Maritime shipping is a key stage of the global freight supply chain, transporting between 80% and 90% of global freight. It is also a critical target for decarbonization, responsible for 3% of global greenhouse gas emissions. This could rise up to 17% of global emissions by 2050, as maritime traffic is projected to increase by 240% — 1,200% by 2050.

One of the reasons that the maritime sector is considered a hard-to-abate industry is the complex ecosystem of players that represent many geographies, levels of governance, and often conflicting interests. Perhaps the most influential of these players are ports.

Ports play key ecosystem roles across policy, regulation, innovation, and technology scaling of sustainable technologies. Green shipping corridors, for example, are port-led initiatives to create specific economic zones to incentivize the uptake of decarbonization technologies, low-carbon fuels, and develop inter-regional and cross-sector partnerships.

Accelerator and incubator programs such as PortXL and Pier71 support early-stage start-ups to develop technologies and establish in-port pilots as well as to connect demand owners—namely shipping companies and fleet operators—with innovators offering decarbonization solutions that meet their specific needs. In an increasingly crowded market, these programs provide early-stage start-ups with market recognition and trust, and support demand owners in the increasingly difficult decision of identifying which solutions and technologies to implement.

Decarbonizing Internal Port Operations

Port operations themselves are the source of both carbon emissions and other pollutants including soot, sulfur oxides, and nitrous oxides. Software-based solutions to digitize, streamline, and optimize port logistics and operations are the low-hanging fruit of decarbonizing ports themselves, and can reduce fuel use and emissions while increasing processing capacity. Deep decarbonization of port operations, however, will come from electrification of equipment, vehicles, and vessels. Achieving full electrification will require both battery-electric and hydrogen-electric solutions in conjunction with energy storage and smart charging solutions.

Innovators providing such optimization solutions include PortXChange, Portcast, and Teqplay. Solutions like flywheel energy storage technology (e.g., QuinteQ), are enabling the electrification of heavy-duty equipment such as cranes by providing charging flexibility and minimizing the demand on local grids. Though battery technology continues to advance, higher energy densities and shorter charging times are required to effectively electrify the commercial vehicles and vessels used in port operations and fit charging times into operations schedules. The short refueling time of hydrogen-electric vehicles are a promising solution, enabling near 24/7 operation. However, the ubiquitous challenges with green hydrogen supply and costly transport and storage remain a barrier to market uptake.

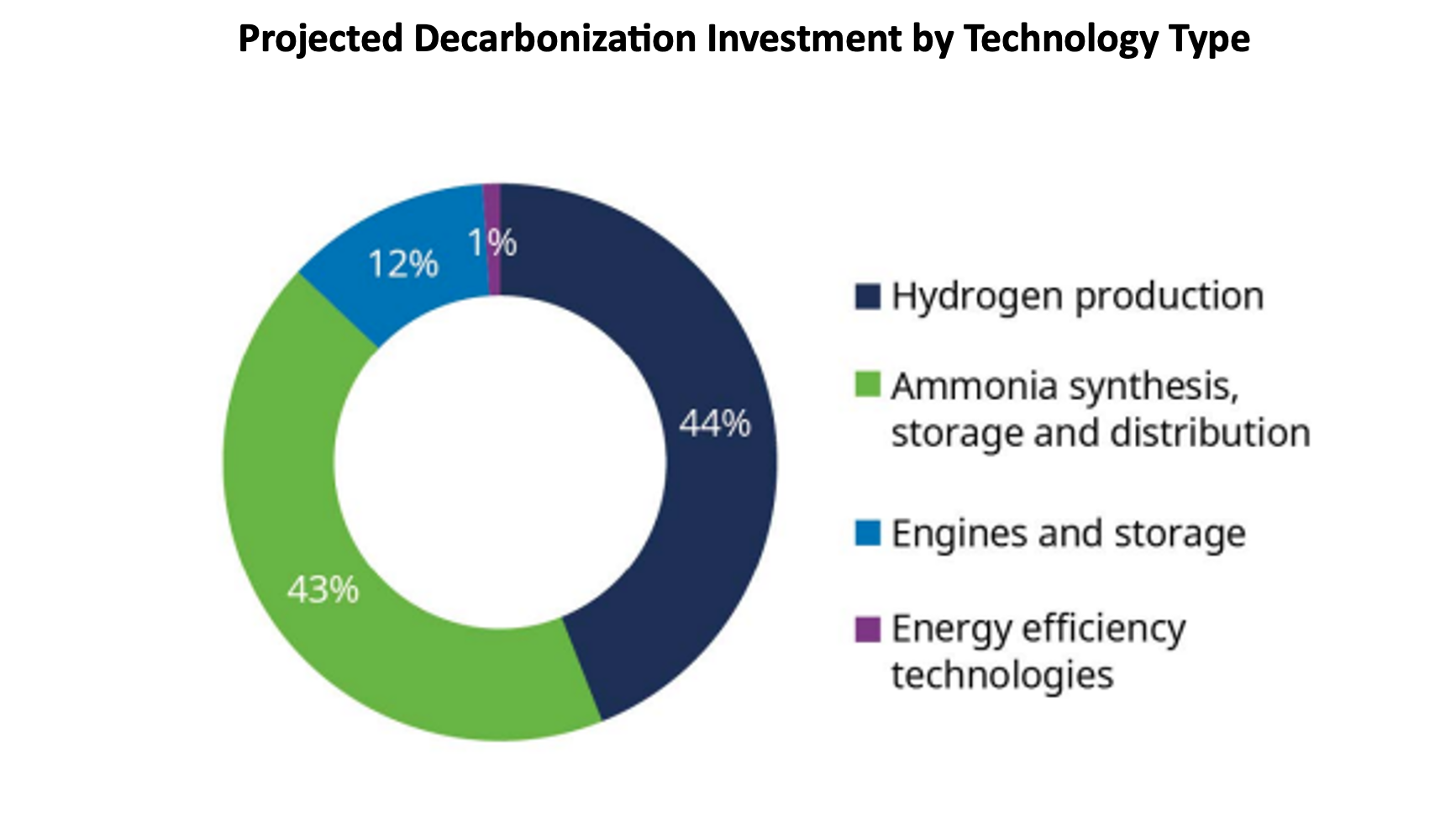

Linchpins of Sector-wide Decarbonization Strategies

Setting our sights on 2050 and the ambitious decarbonization targets set by the IMO, incremental decarbonization technologies improving fuel efficiency or fleet and vessel optimization, will not be sufficient to reach the 2040-2050 targets of 70%-100% emissions reduction. Systemic, industry-wide shifts towards zero-carbon fuels are the only realistic pathway to deep decarbonization of maritime shipping and ports and will play an essential role in this transition as deployers of alternative fuel infrastructure.

Hitting the IMO target of decarbonizing global shipping by 2050 will require at least $1.9T in investment. According to the Global Maritime Forum, only 13% of this investment is required by vessel efficiency technologies while the vast majority (87%) of investment must be directed towards infrastructure for fuel production, storage, and bunkering.

The uncertain future of alternative fuel production, cost, and supply poses a significant risk for shipping companies and fleet operators, stymying investment and uptake. Deployment of bunkering and transport infrastructure lowers the risk of ordering new-build vessels that are compatible with alternative fuels. This dynamic can be seen most clearly in the current trend towards ordering methanol-compatible ships over other alternative fuels.

The availability of methanol bunkering and storage, in comparison to hydrogen and ammonia, for example, makes it a safer choice for fleets that must choose to transition towards a specific alternative fuel. As ammonia and hydrogen storage in general become more cost-efficient, safer, and available in more ports across the world, orders for compatible vessels will follow. Innovators are addressing technology barriers to green hydrogen production with novel electrolyzers (e.g., SungreenH2), transport and storage of alternative fuels (e.g., Voyex), ammonia cracking (e.g., Amogy), alternative fuels conversion (e.g., Prometheus Fuels), and ammonia bunkering (e.g., Azane Fuels).

Looking forward…

- Widespread deployment of bunkering facilities for various alternative fuels will further investment, corporate engagement, and technology development to lower production and transport costs

- Ports will become sites of green hydrogen production and/or key nodes in green hydrogen distribution networks both for refueling of in-port vehicles and vessels and the production of zero-carbon fuels

- Once technological barriers are addressed to enable safer and more cost-effective transport and handling of ammonia, supply constraints of e-methanol will shift market preference from e-methanol to green ammonia

- As shipping corporates engage across the value chain of alternative fuels, collaboration between ports and fuel producers will streamline industry transition and market uptake of new fuels

- Current push to establish onshore power to eliminate at-berth emissions will meet significant challenges, particularly regarding grid capacity and renewables supply

- Leveraging of existing bunkering infrastructure, distribution networks, and value chains will be major differentiator between alternative fuels— minimizes infrastructure build-out costs, eases distribution, and reduces overall cost of transition for demand owners

- Zero-carbon fuel costs will not compete with conventional bunker fuel, despite advances in production and storage technologies—policies established between ports, and at the national and international level must effectively incentivize alternative fuel uptake and penalize continued emissions to drive industry transition