In the overview of our January 2020 Global Cleantech 100, we welcomed readers to the “Roaring 20s,” predicting a decade of cleantech growth, continuing the consistent expansion we had seen since 2016. By January 2021, we had already changed our terminology the “chaos of the 2020s,” written in the midst of the Covid pandemic but just before a historic surge in cleantech investments. At the release of the 2025 Global Cleantech 100, the U.S. stands on the brink of Donald Trump’s re-inauguration, marking another major shift in global energy and climate direction within just five years.

The only certainty in this decade is uncertainty. At this mid-point, we see cleantech innovation approaching three significant tipping points that will define its trajectory. From where we are sitting today, we can see three over-arching tipping points emerging, that provide the backdrop for 2025’s cleantech innovation unfoldings:

- Tipping Point #1: The Supply Economics Survival Game: We’ve observed an unprecedented surge in first-of-a-kind (FOAK) cleantech projects in recent years. Entrepreneurs have shown remarkable resourcefulness in financing these endeavors, but the anticipated reduction in policy support and incentives, especially in the U.S., will require the ability to compete on market economics. Notably, some companies are already demonstrating their ability to navigate this shift, as reflected in this year’s Global Cleantech 100 list.

_ - Tipping Point #2: The Power Shortage Demand Pull: The historic surge in power demand fueled by data centers, EV charging, and the electrification of manufacturing and buildings is exerting a substantial influence on electricity generation sources, energy efficiency, and uptime assurance. This demand pull is creating a favorable environment for cleantech solutions that can address these challenges.

- Tipping Point #3: The Resilience Renaissance: Climate adaptation and resilience, once a niche area, are poised to enter the mainstream. This shift is driven by escalating temperatures, increasingly frequent extreme weather events, and the expanding “uninsurable frontier.” Consequently, new technologies are being integrated into public safety, health, and finance discussions. The resurgence of water as a prominent theme in this year’s Global Cleantech 100 list underscores this trend.

A Lean Financing Environment Demands Early Indicators of Commercial Engagement

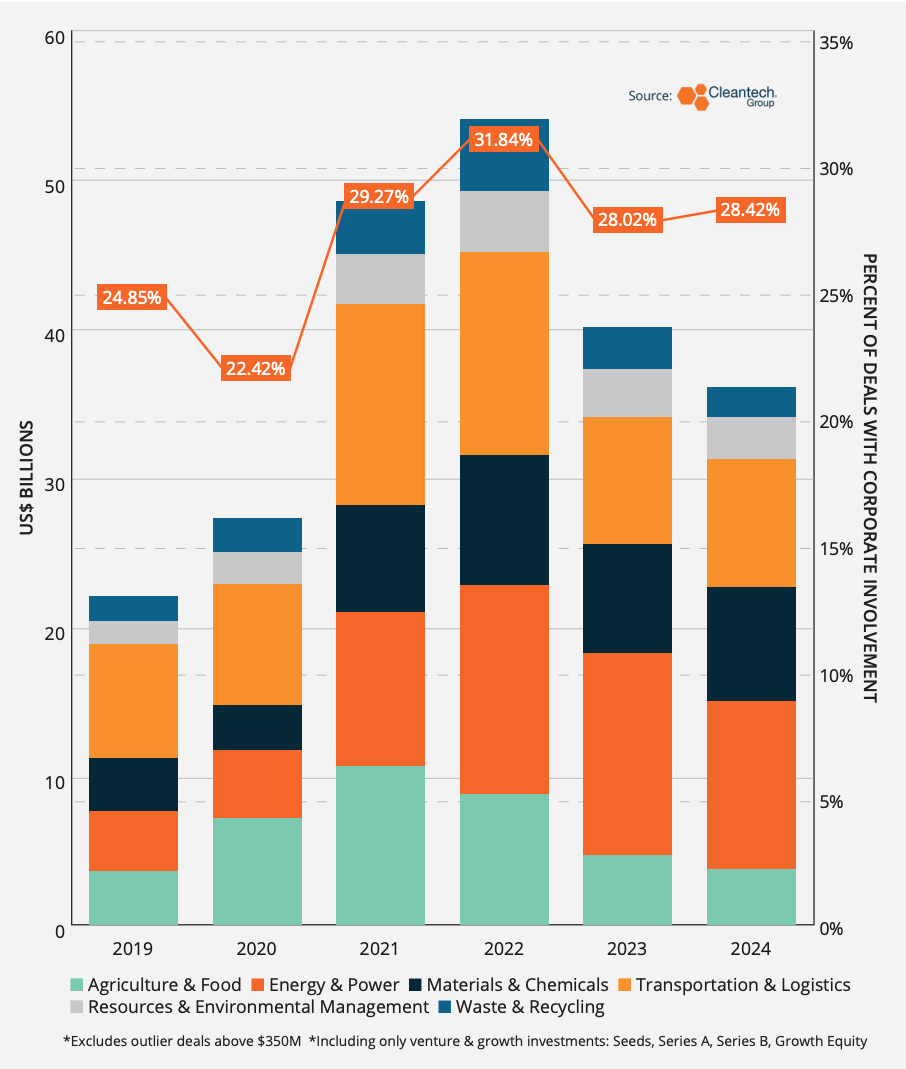

We noted in our report that 2024 witnessed investors prioritizing initial commercial results as a basis for capital allocation. Corporate involvement played a pivotal role in venture investments, with nearly 30% of all deals involving a corporation.

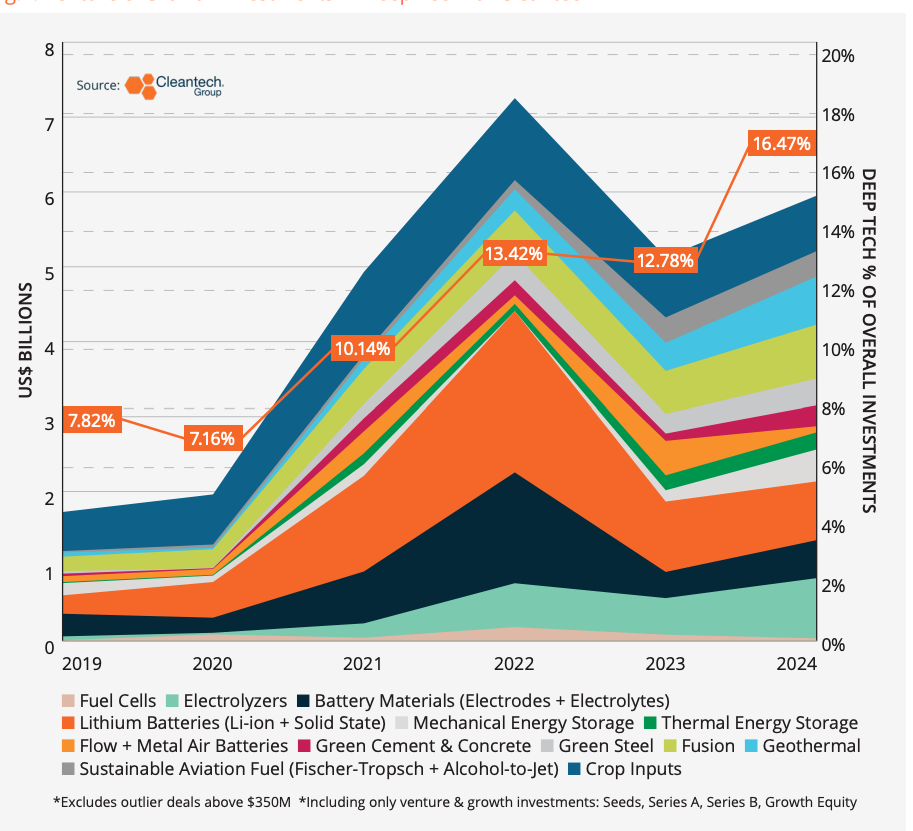

The Deep Tech Drive Hits a New Gear

In 2024’s Global Cleantech 100, we covered the major shift in innovation focus from incremental improvements to deep scientific innovation targeting big picture shifts in sustainability. That trend only strengthened through 2024, and deep tech for cleantech now comprises the largest percentage of investments as it ever has. Remarkably, even in a year with lower aggregate cleantech investments, 2024 funding in deep tech for cleantech outpaced their 2023 totals.

Tipping Point #1: Supply Economics

Cleantech innovators are making strides in decarbonizing heavy industries like steel, cement, and chemicals, traditionally “hard-to-abate” sectors. Notable examples in this year’s Global Cleantech 100 include:

- Boston Metal (six-time Global Cleantech 100) launched its first commercial molten oxide electrolysis facility in Brazil.

_ - Sublime Systems (three-time Global Cleantech 100) announced plans for a commercial cement facility in Massachusetts by 2026.

_ - Infinium Holdings (Global Cleantech 100 2023, 2025) began operations at a sustainable aviation fuel facility in Texas, with another planned for 2026.

_ - OXCCU (Global Cleantech 100 2024-2025) opened a demonstration plant at Oxford Airport in 2024.

_ - Antora Energy (Global Cleantech 100 2023, Cleantech 50 to Watch 2021) deployed a thermal battery in California and raised $150M to scale manufacturing.

Tipping Point #2: Power Demand

Data centers are emerging as significant demand drivers for clean energy technologies. For example:

- Fervo Energy (four-time Global Cleantech 100) launched a geothermal project for Google’s data centers in Nevada, followed by a $244M equity round to develop a Utah plant by 2026.

_ - Goldman Sachs estimates that AI advancements will increase data center power demand by 160% through 2030, accelerating adoption of clean power and cooling technologies.

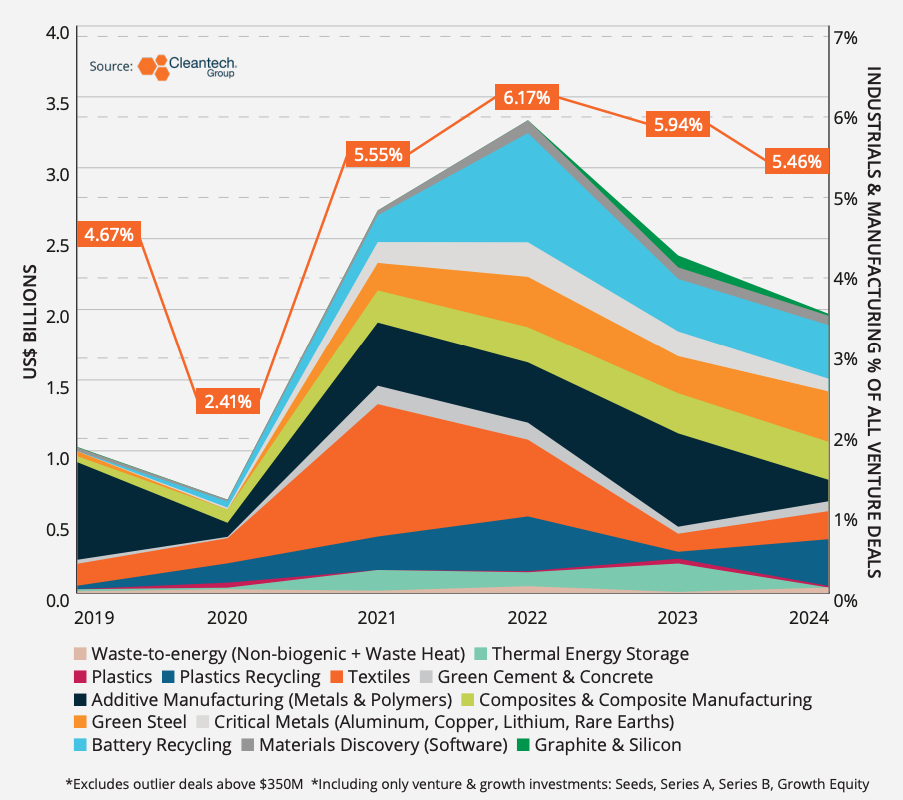

The Fight for the Factory Floor – Are Winners Emerging Already?

We wrote last year about the convergence of two trends—resource reduction in industry and manufacturing of new energy products—to form an undeniable theme in cleantech innovation that an industrial transformation was coming to fruition. In 2024, investments into innovators within these trends outpaced those of 2023, despite the overall dip in 2024 venture and growth investments.

Companies pioneering battery recycling and materials recovery are addressing tipping point #1 with FOAK facilities:

- Nth Cycle (back-to-back Global Cleantech 100) launched the U.S.’s first nickel and cobalt production facility using electro-extraction.

_ - Li Industries (2024 Global Cleantech 100) secured $55M from the DOE to establish a lithium iron phosphate recycling plant in partnership with General Motors.

_ - Cylib (2025 Global Cleantech 100) received $2M for water-based lithium recovery technology, with a pilot facility in Germany planned for 2027.

_ - Cyclic Materials advanced rare earth magnet recovery, launching a pilot plant in 2023 and a demonstration facility in 2024, with off-take agreements from Solvay and SYNETIQ.

The upstream critical materials value chain is well-reflected in this year’s Global Cleantech 100 as well:

- Mangrove Lithium (three-time Global Cleantech 100) and Summit Nanotech (Global Cleantech 100 2021, 2024-2025) are forging ahead in direct lithium extraction.

_ - PH7 (Global Cleantech 100 2024-2025) is innovating in heap leaching for copper and e-waste solvometallurgy.

_ - Copprint (Global Cleantech 100 2023-2025) refining conductive copper printing for power electronics.

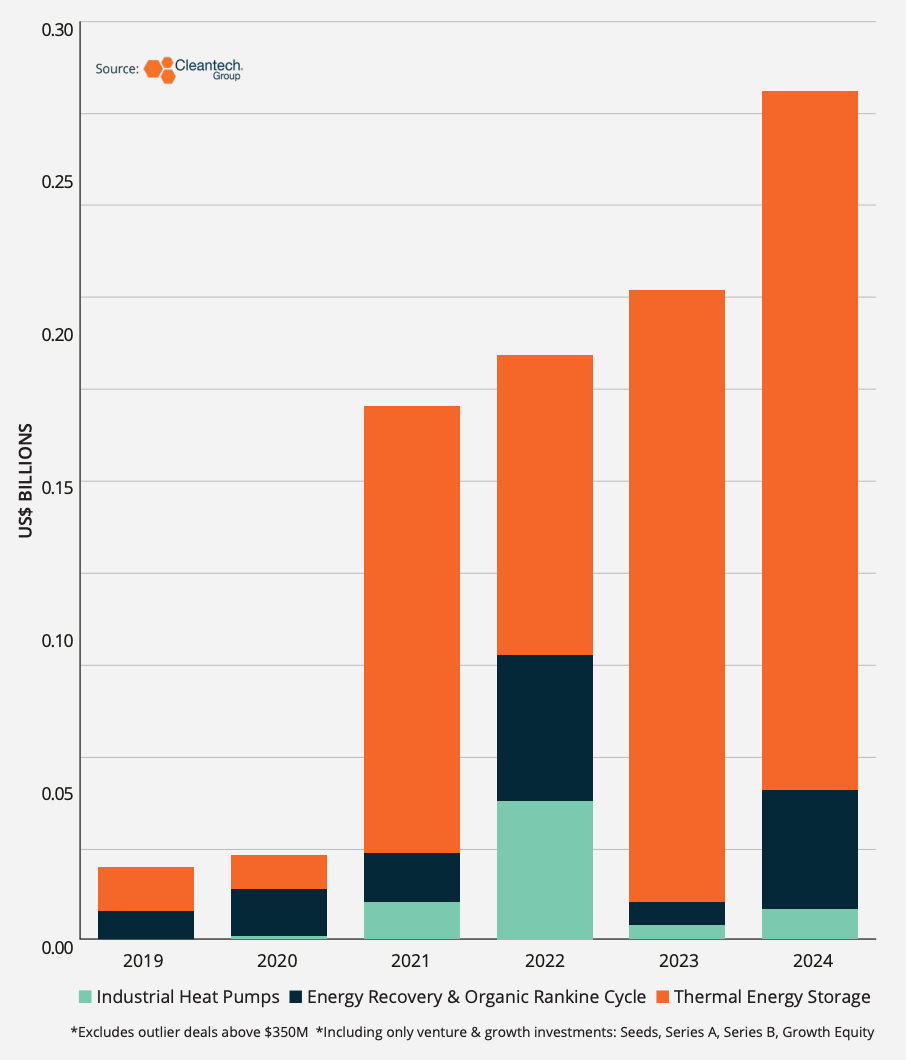

We also wrote in 2024 about the emerging importance of sustainable approaches to manufacturing today’s commodities and products. Within the theme of industrial electrification, especially electrification of heat processes, the investment momentum in 2024 outstripped even the most active investing years of 2021 and 2022.

This year’s Global Cleantech 100 offers some instructive examples of which technologies are starting to be perceived as high-potential industrial electrification vectors:

- Delivering high-temperature process heat to heavy industry processes including steel and cement generally requires temperatures of 1000° C – 1250° C. Thermal energy storage systems operating at these temperatures can also spin a turbine to generate electricity from the stored heat – that’s where companies like Antora Energy (Global Cleantech 100 2023, Cleantech 50 to Watch 2021), Kraftblock (Global Cleantech 100 2024-2025), and first-time Global Cleantech 100 company RedoxBlox come in, storing at temperatures of up to 1300° C – 1500°C.

_ - Low-temperature heat (<200° C) is the “bottom of the iceberg” in industrial emissions, found in many large industries such as food and beverage processing, recycling, and in parts of complex chemicals production. This year’s Global Cleantech 100 features three first-time award winners in low-temperature heat electrification: Skyven (steam-generating heat pumps), Atmoszero (electric boilers), Qpinch (chemical heat pumps).

Passing Paris – Can Adaptation Accelerate in 2025?

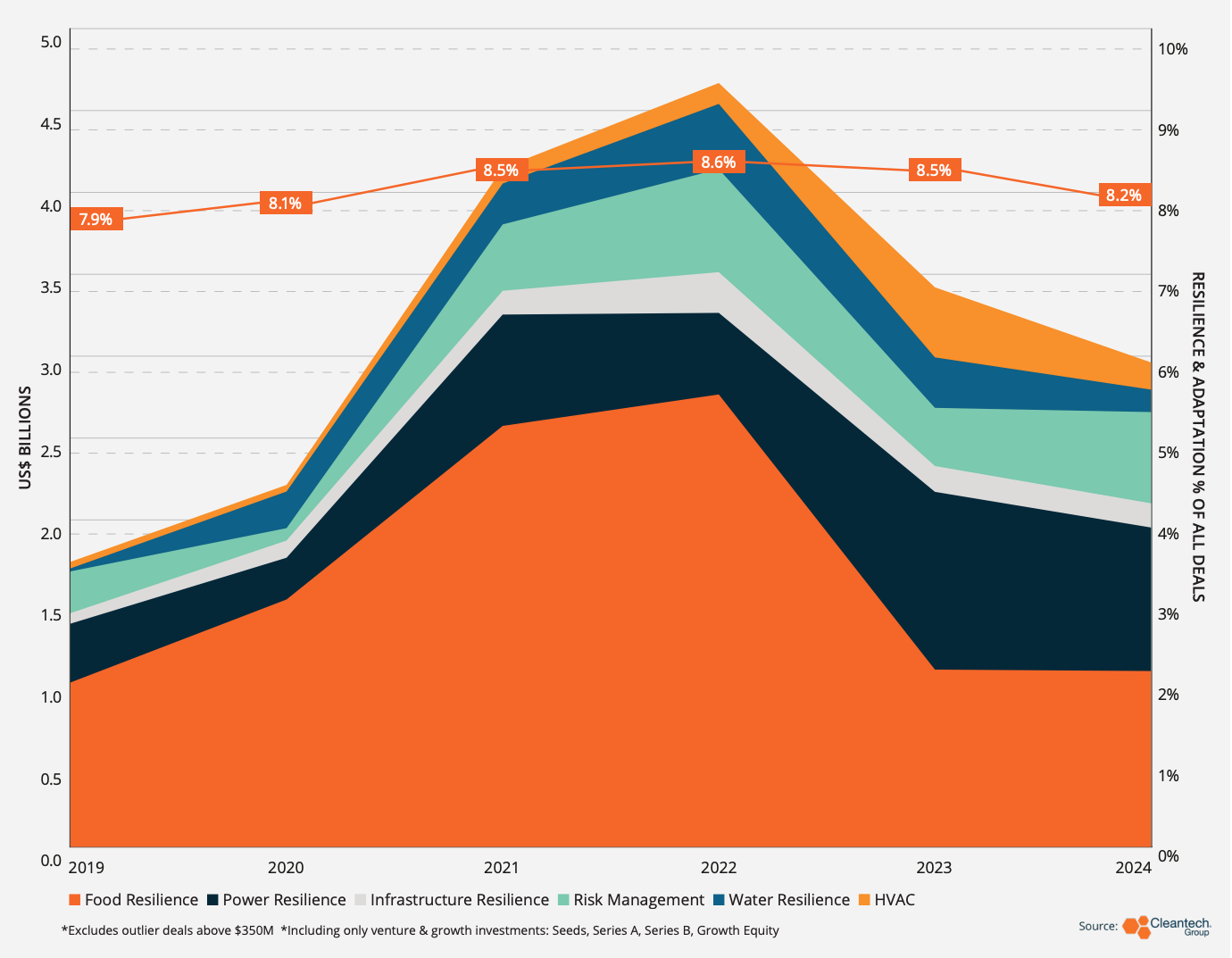

2024 exceeded 2023 as the hottest year on record (World Meteorological Organization), and as the reality begins to set in that the world is likely to surpass the 1.5° C warming limit that the Paris Agreement set out, we continue to wait for the urgency to be reflected in innovation and investment. Venture investments in adaptation and resilience continue to top out between 8-9% of all cleantech investments.

The 2025 Global Cleantech 100 featured promising innovations addressing tipping point #3 (resilience urgency):

The recent, tragic wildfires in Los Angeles underscore the pressing need to adopt wildfire resilience technologies. New wildfire tech is prepared to close off risk gaps in real time; take 2025 Global Cleantech 100 debutante Burnbot, who has developed remote-operated robots to carry out prescribed burns and prevent wildfire outbreaks before they happen. Indeed, the wildfire tech community, while small, is combining forces across parties and is positioning itself to unlock latent demand in 2025. We wrote in last year’s Global Cleantech 100 about the launch of Convective Capital, the first dedicated wildfire tech venture capital fund. In 2024, Convective and a group of partners began formal lobbying efforts and have already engaged with members of the U.S. Congress.

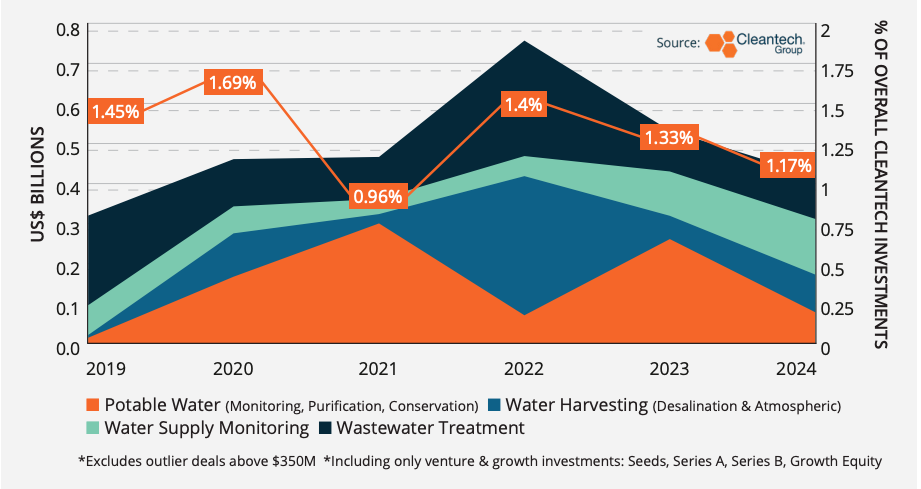

Will Water Finally Have its Moment in 2025?

In the 2024 Global Cleantech 100, our 15th iteration of the report, Cleantech Group CEO Richard Youngman noted in his foreword that in the first edition of the report, there were nine water-related companies on the list, and that number was never reached again. In 2024, there were two, but the theme shows a glimmer of a return in 2025 with six companies on the list.

Water continues to play a side role in overall cleantech investments, but we see tipping points #1 (supply economics) and #3 (resilience urgency) emerging in a noticeable way in this year’s Global Cleantech 100 companies:

Two new takes on the reverse osmosis process through unique membrane formulations have landed on this year’s Global Cleantech 100 list:Aqua Membranes and ZwitterCo. Note the corporate urgency here: Micron was an investor in Aqua Membranes and BHP and Munich Re Ventures were investors in ZwitterCo.

Centralized wastewater treatment is viewed as a venue of demand opportunity, as well. This year’s Global Cleantech 100 list boasts a mini value chain of wastewater treatment technologies:

- Molear uses nanobubble aeration techniques to flatten energy demand in aeration processes and reduce the need for chemicals to reduce residue.

_ - Aclarity has developed a novel electrochemical approach to PFAS destruction.

_ - Indra Water is decentralizing the electrochemical treatment approach and bringing modular treatment units to site-of-use, while also leveraging internally developed automation and analytics for OPEX reduction.

_ - Pani Energy is bringing AI to wastewater treatment and desalination plants through granular sensing and diagnostics to prescribe surgical chemical inputs and membrane maintenance.

2025 Will Be the Year We Remember the Guardrails Coming Off

Policy uncertainty, the success of deep tech innovators clearing FOAK hurdles, and growing demand for climate adaptation technologies signal an intensified focus on product and project economics in 2025. Companies leveraging organic demand in areas like data centers and proving their technologies in real-world environments without relying on favorable policies are well-positioned to succeed. Key milestones to watch include:

- Data center hardware exits: Expect growth in cooling solutions, power conversion technologies, and grid hardening as demand for energy efficiency surges. Data centers, with their price-insensitive buyers, are likely to drive innovation and acquisition activity.

_ - FOAK project ripple effects: The success of first-of-a-kind facilities in 2024 marks a significant step toward scaling nth-of-a-kind operations. Companies that can deliver scalable solutions will lead the market, while fast followers benefit from lessons learned by early adopters.

_ - Expect a few China blindsides: This year’s Global Cleantech 100 list includes only two companies from China, raising questions about whether its innovation has slowed or if the global ecosystem is losing visibility. The latter seems more likely. As China’s renewables and EV rollout accelerates, innovations in energy storage, grid resilience, and materials are likely. Ambitious plans for nuclear fission and fusion could also yield advances. While trade decoupling dims export prospects, it also reduces global insight into emerging Chinese technologies.

_ - Adaptation and resilience tech: Technologies such as wildfire prevention tools are moving beyond government applications, gaining traction among utilities and private consumers. Markets are beginning to adopt new metrics for evaluating adaptation technologies, creating opportunities for innovative solutions in resilience.

We extend our congratulations again to all of this year’s Global Cleantech 100 companies and look forward to continuing to accompany you on the next leg of the journey.