Earlier this month the 2025 Global Cleantech 100 was launched, identifying 100 cleantech companies most likely to make a significant impact in the coming years and providing key trends and forward-looking analysis for the year to come. Overall investment in the Transportation & Logistics (T&L) industry group remained steady from 2023 despite the slight overall decline in venture investment in cleantech as a whole.

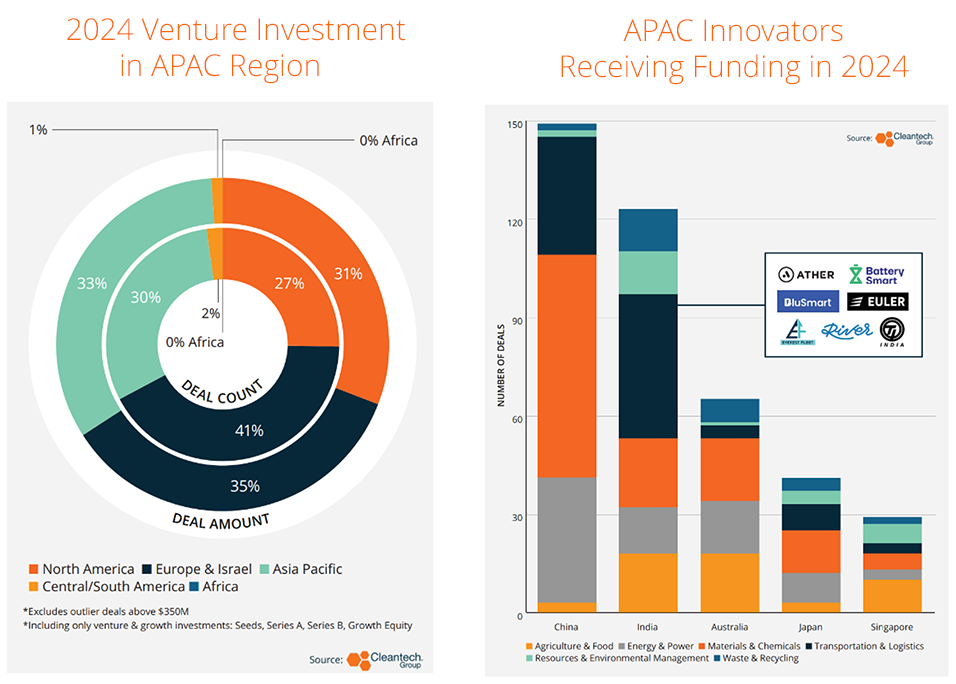

APAC innovators have consistently had a strong presence in T&L compared to other cleantech industry groups and cleantech as a whole. For several years, APAC innovators have been the source of nearly a third of T&L venture investments as well as overall investment amount, compared to 17% of investment across all cleantech sectors.

Despite the lower number of deals, the average investment size has substantially increased from 2023, particularly for late-stage deals. While late-stage deal count dropped to an all-time low in Q4, T&L late-stage deals averaged $59M, soundly outperforming the cleantech-wide average of $36M.

Unsurprisingly, of APAC innovators that raised funds this past year, Chinese innovators took the lead with nearly 150 distinct China-based innovators announcing venture investments. Chinese cleantech innovation has been highly focused on Materials & Chemicals and Energy & Power, with over two-thirds of these innovators specializing in these, specifically in the energy and battery value chains sectors.

Exploring India’s Thriving Cleantech Ecosystem

One of the key highlights that emerged when reviewing the past year for the T&L industry group was the strong performance of the Indian cleantech ecosystem.

The Indian cleantech innovation ecosystem placed a close second behind China, with over 120 innovators closing funding rounds in 2024.These India-based innovators are spread more evenly across cleantech sectors, but over a third work in the T&L space (44 distinct Indian T&L innovators closed funding rounds in 2024 – more than any other APAC country). In fact, Indian T&L innovators were one of the most active categories across the entire cleantech taxonomy.

Key Subsectors of the Emerging Indian Cleantech Ecosystem

The micromobility sector in India is no longer emerging, but is now a well-established cleantech powerhouse, as was well reflected in the 2024 investment data. Innovators like TI Clean Mobility ($69M Growth Equity) and Ather Energy ($71M Growth Equity) raised large, late-stage funding rounds to expand operations and reach new markets. However, the Indian cleantech ecosystem is deepening and diversifying, quickly expanding to provide a range of products and services to enable deep electrification of transport systems.

Fleet electrification has emerged as a key sub-sector, with innovators such as ALT Mobility, Everest Fleet, BluSmart, Vecmocon, and Magenta Mobility providing electrification and logistics services to integrate and optimize electric fleets. BluSmart, a 2025 Global Cleantech 100 company, provides ride-hailing services in electric vehicles and runs a charging infrastructure network.

While micromobility is dominant, innovators are also providing solutions for electric commercial vehicles. Electrification of public transport, particularly city buses, is on the rise with approximately 12% of new bus sales in 2025 expected to be electric. Innovators such as GreenCell Mobility are targeting this market.

Aviation is another emerging area of electrification for Indian innovators. Not immune to the eVTOL boom, Indian innovators are developing electric urban aircrafts. The ePlane Company, Sarla Aviation, and BonV Aero all raised venture funding rounds this past year to support the continued development of eVTOLs with the goal of reducing urban congestion and emissions and providing cargo solutions for challenging terrains.

To support this sector-wide shift towards electric transport, an extensive network of electrification and charging infrastructure innovators are deploying solutions across India. Critically, charging and battery swapping innovators aim to deploy networks to enable the expansion of public and private electric vehicles. Where the local grid is unreliable or inaccessible, battery swapping networks provide a reliable alternative to charging networks. Additionally, sale of E2&3-wheelers without the battery reduces up-front costs for consumers, a significant barrier to adoption. Battery swap stations offer significant, though as-of-yet unrealized potential for energy storage and grid stabilization services as well.

As India´s transportation network becomes increasingly electrified, battery and charging solutions are in high demand. Battery Smart raised $65M in a Series B round to deploy battery swapping networks across India and Urja Mobility closed a $12M Seed round for their EV battery leasing platform. Meanwhile, innovators such as Charge Zone, Kazam, Neuron Energy, and Ultraviolette also raised funding to develop a range of battery and charging solutions.

Keep an Eye On EV Powertrains and Components

A small but growing corner of the Indian T&L cleantech ecosystem, innovators like Electra EV and Chara Technologies are developing EV components—namely powertrains and electric motors. High electrification and stiff import tariffs on EVs and components create a strong demand market for locally manufactured, high-efficiency EV motors and components for both E2&3-wheelers and larger electric vehicles.