APAC: What We Learned from 2024 and What It Means for 2025

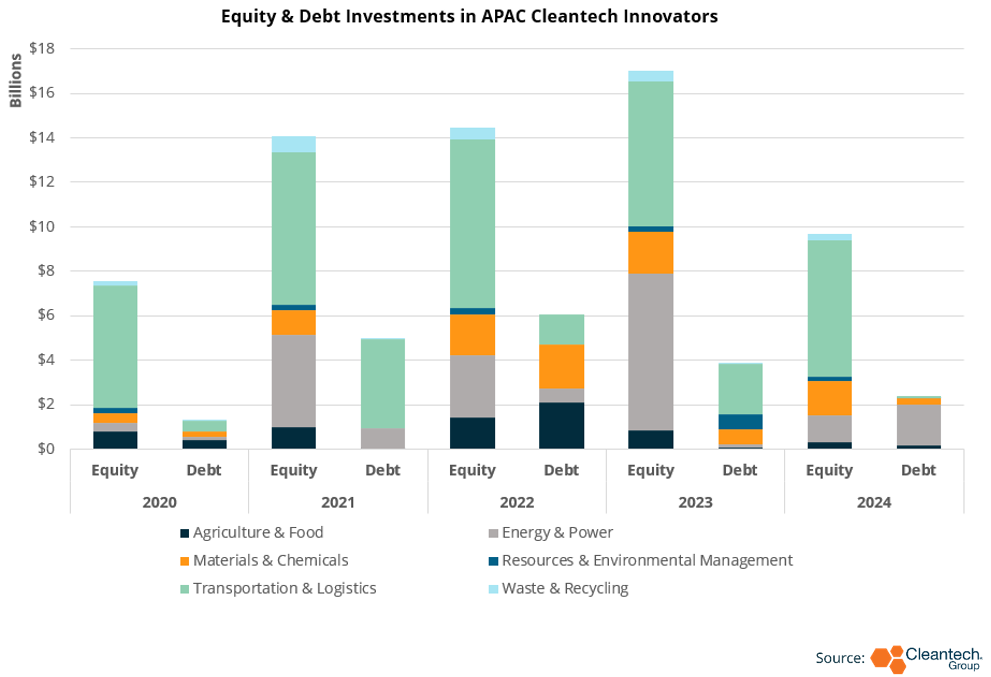

In 2024, the Asia-Pacific region (APAC) saw a relative cooling off period after the meteoric growth experienced in 2023. The Energy & Power industry group’s stunning 2023, underpinned by Chinese innovation in solar and battery technology, came back down to Earth in 2024. However, focusing on this apparent drop-off risks missing two bigger takeaways:

- Many of these companies are more bankable now and less reliant on equity (see the 2024 debt statistics for Energy & Power.

- Other spaces such as Transportation & Logistics and Materials are continuing at pace.

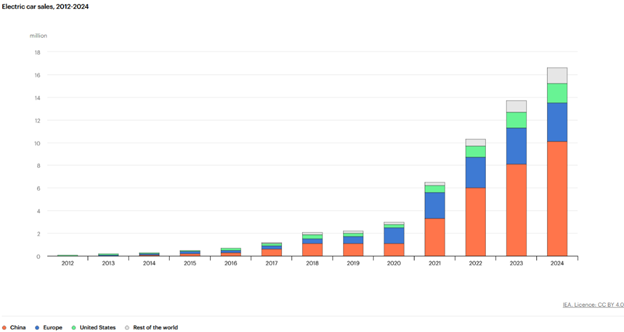

While 2023 reinforced much of what we already knew around Chinese advantages in electrification of power supply (e.g., the success in rolling out and innovating in new solar and energy storage), 2024 drove home the advantages that have crystallized in the electric mobility economy. If looking at the top 15 areas of investment in APAC versus those in North America and Europe, there is a clear central focus on electric mobility in APAC. This trend goes well beyond what one typically associates with electric mobility – e.g., electric passenger vehicles, batteries, and chargers – now to full-scale electrification infrastructure that accommodates multiple types of vehicles and charging styles.

China is both APAC and the world’s center of gravity in electric vehicle (EV) sales – the statistics from the IEA below show where China accounted for an estimated 60% of the world’s EV sales in 2024, and EVs comprised an estimated 45% of all vehicle sales in China. Nevertheless, more export markets are mulling tariffs on Chinese EVs, and concerns over production over-capacity are increasing. Expect innovation for better and more efficient infrastructure to be in higher demand as vehicle OEMs seek to diversify revenue streams.

Source: International Energy Agency

Source: International Energy Agency

Case in point, Nio Power, the charging and infrastructure subsidiary of Nio, raised a $200M Growth Equity round – the entity’s first external financing round – to expand R&D and manufacturing of its battery charging and swapping infrastructure. Nio Power is aiming to deploy over 3,000 battery swapping stations in China (up from around 2,000 in mid-2024). Nio Power estimates that their swapping process takes approximately 3 minutes, an ideal approach for drivers in Chinese cities who are unlikely to charge at home and want to avoid public charging. This financing is also expected to support development of vehicle-to-grid capabilities.

Photo: Nio Power

Battery swapping has obvious benefits for drivers of passenger vehicles in dense urban areas, but innovation is now cropping up to make it a reality for fleets and heavy-duty vehicles. Especially relevant for fleets with fixed routes and where time-to-route completion is a priority issue, expect to see more battery swapping models pick up.

Singapore-based Open Energy is bringing its Hyperswap battery-as-a-service offering to fleet owners who value speed-of-route completion and want to control total cost of ownership of fleets. Open Energy is also integrating its swapping stations into grid flexibility through an AI orchestration engine that optimizes time of charge and engages grid balancing programs.

Keep an eye out for battery swapping in heavy-duty vehicles. A long-stated pain point of industries like mining, steel, and cement, is that to use electrified heavy-duty vehicles requires significant power capacity for charging, and that the distributed nature of these industries makes infrastructure build out challenging. Add to that the 24/7 nature of these operations and charging time becomes a material opportunity cost. China’s QiYuan Core Power has developed modular, scalable mobile charging and battery swapping stations for heavy industry. The company raised a $211M Series B in 2024, following a $223 Series A in 2022.

Photo: QiYuan Core Power

Deploying new technology in real-world environments is critical to generating learning effects fast and developing cost advantages. If China’s electric truck trend continues its path upward since the pandemic, expect to see more novel technologies supporting expansion of vehicle electrification into the hard-to-abate sectors. If, as we noted in our last quarterly APAC analysis, the trend of innovation in electric aviation continues to grow in China, expect to see this converge with innovation around remote charging.

Source: International Energy Agency

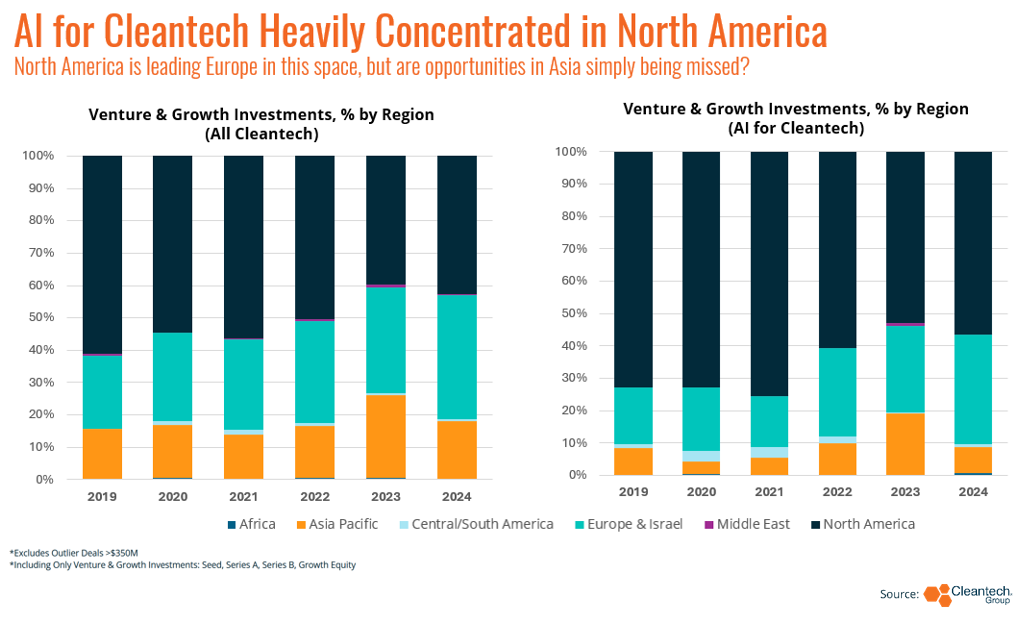

Cleantech Group has, over the past year, made it a goal of ours to estimate the potential impact – both drawbacks and benefits – of the latest AI revolution on our theme. We have noted that, while APAC always plays heavily in overall cleantech investments — around 15% of the global total — that presence has generally been lower in cleantech applications of AI.

This begs the question of whether there is a true lag in APAC, or whether the market has demonstrated demand pull yet, while it still absorbs a significant amount of hardware innovation that has commercialized in recent years. It is also possible, given the surprise that the world experienced with DeepSeek a few weeks ago, that we have not yet fully imagined all of the areas where APAC, principally China, will play.

Nevertheless, in 2024, we did see both an application-rich and geographically diverse AI for cleantech ecosystem begin to crystallize in early-stage APAC rounds.

- Aprisium (Singapore) raised a $7M Series A to further develop their on-site testing and analytics suite for water quality testing and contaminant monitoring (e.g., PFAS).

- Fyllo (India) provides sensors and analytics to farmers, including for irrigation, weather monitoring, and precision application of crop treatments. The company raised a $4M Seed round in 2024.

- Fitsol (India) raised a $1M Seed to further develop their AI-enabled emissions management tool for heavy industry.

- AI Palette (Singapore) raised just under $5.5M in two parts of their Series A round, to continue developing an AI discovery engine for food ingredients and packaging. The company intends to use the funds to further expand in the Americas.

A Fyllo weather station

Photo: Fyllo

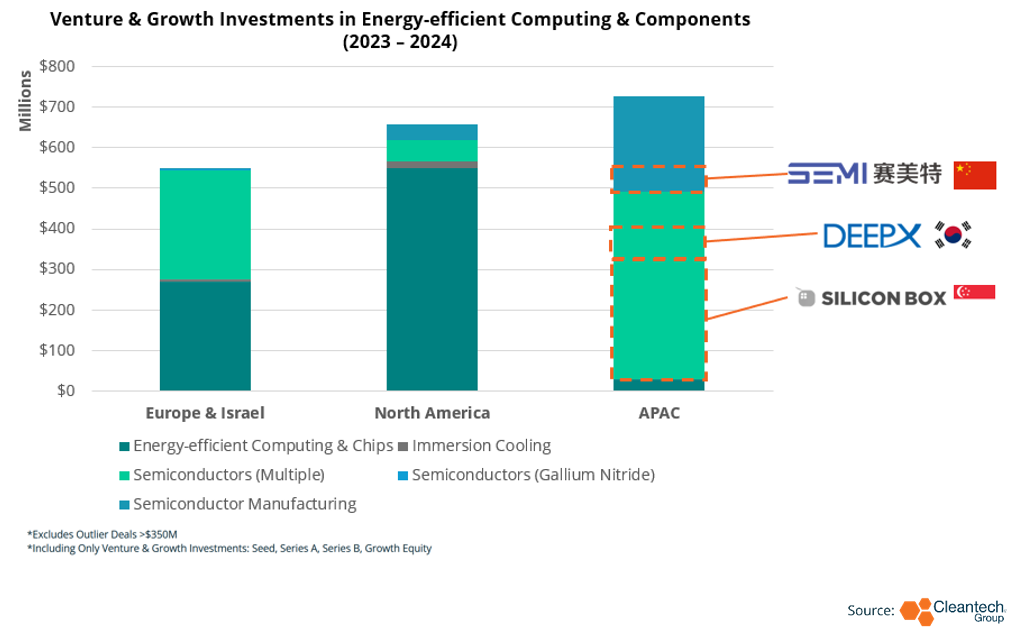

The other side to the sustainability equation of the AI revolution is ensuring that new gains in benefits are not outweighed by emissions costs. Reducing emissions requires a full spectrum of technologies, from baseload power to power management and cooling in data centers, to new types of AI chips and semiconductors that reduce energy consumption. APAC is demonstrating early innovation strengths across this spectrum already.

- Sustainable Metal Cloud (Singapore) is developing immersion-cooled data centers that provide a low-carbon cloud to users of advanced AI services.

- Silicon Box (Singapore) designs and manufactures low power-consuming chiplets. In 2024, the company raised $60.6M, just a year after a $139M round.

- DeepX (Korea) received a 2024 CES Innovation Award for its cost- and power-efficient AI chips, aimed at data centers, mobility, and robotics. The company raised $80.5M to scale manufacturing for global distribution of its LLM on-device solutions.

- Further upstream, Semi-Tech (China) raised a $72.3M Growth Equity round in 2023 to support further growth of their manufacturing efficiency software, which counts semiconductor manufacturing as one of its key markets.

Photo: Sustainable Metal Cloud

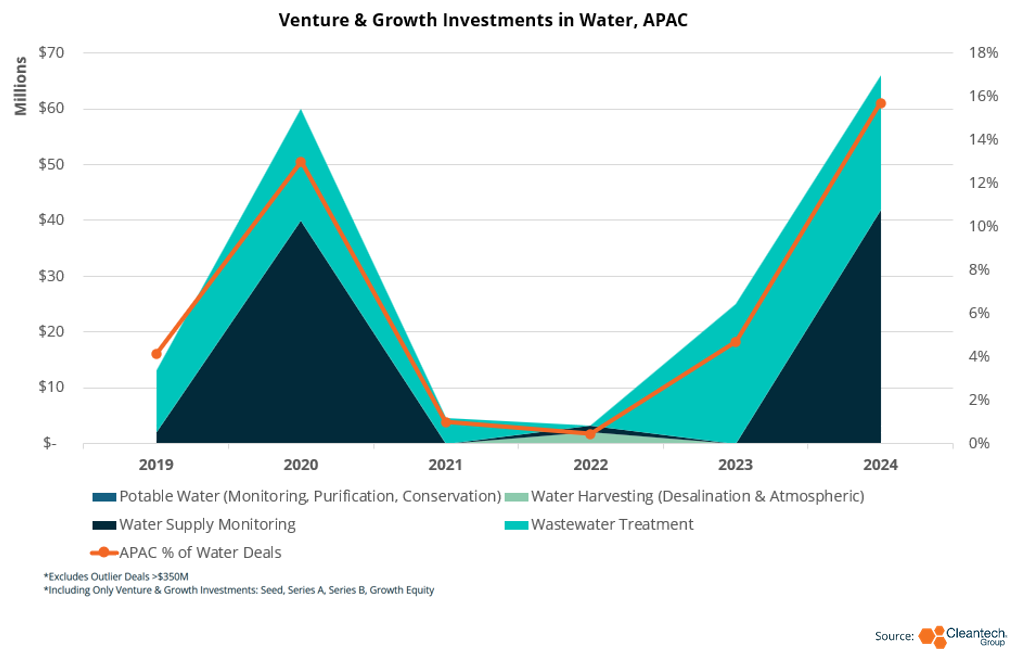

We noted in this year’s Global Cleantech 100 that, while the investment numbers do not indicate investor embrace of water technology yet, the presence of six water companies on the list of 100 does indicate that novel technologies are preparing to hit market. Encouragingly, APAC is playing an outsized role in launch and growth of water innovation.

India is tackling resource efficiency in wastewater treatment head-on. Take Global Cleantech 100 company Indra Water, whose modular wastewater treatment plants can bring water treatment to remote industrial sites and rural populations. The technology is capable of removing a number of pollutants and pathogens and slices size and cost of wastewater treatment by nearly a third. Haber Water’s robotic sampling unit and AI analysis flattens time to results in testing and cuts out costly manual processes. Haber raised a $38M Growth Equity round in 2024.

Photo: Haber Water

A Look Ahead

In a year where global appetite for risk is likely to give way to more emphasis on resource efficiency, take close note of solutions like the ones listed above – offering critical capabilities at lower cost and high efficiency, and leveraging modularity to cut out costly infrastructure buildouts. We predict that 2025 will be a year of “doing more with less” in industry, and we may see some APAC innovators with outsized opportunities.