Battery Recycling and Materials Innovation in APAC

The APAC region has for years shown strength in production of finished electric vehicles (EVs) and in multiple form factors (passenger vehicles, trucks, two- and three-wheelers). And while many are aware of China’s long-standing domination of battery materials supply chains, fewer are aware of the deeper innovation occurring in the region around higher-performing battery materials and resource-efficient access to raw materials.

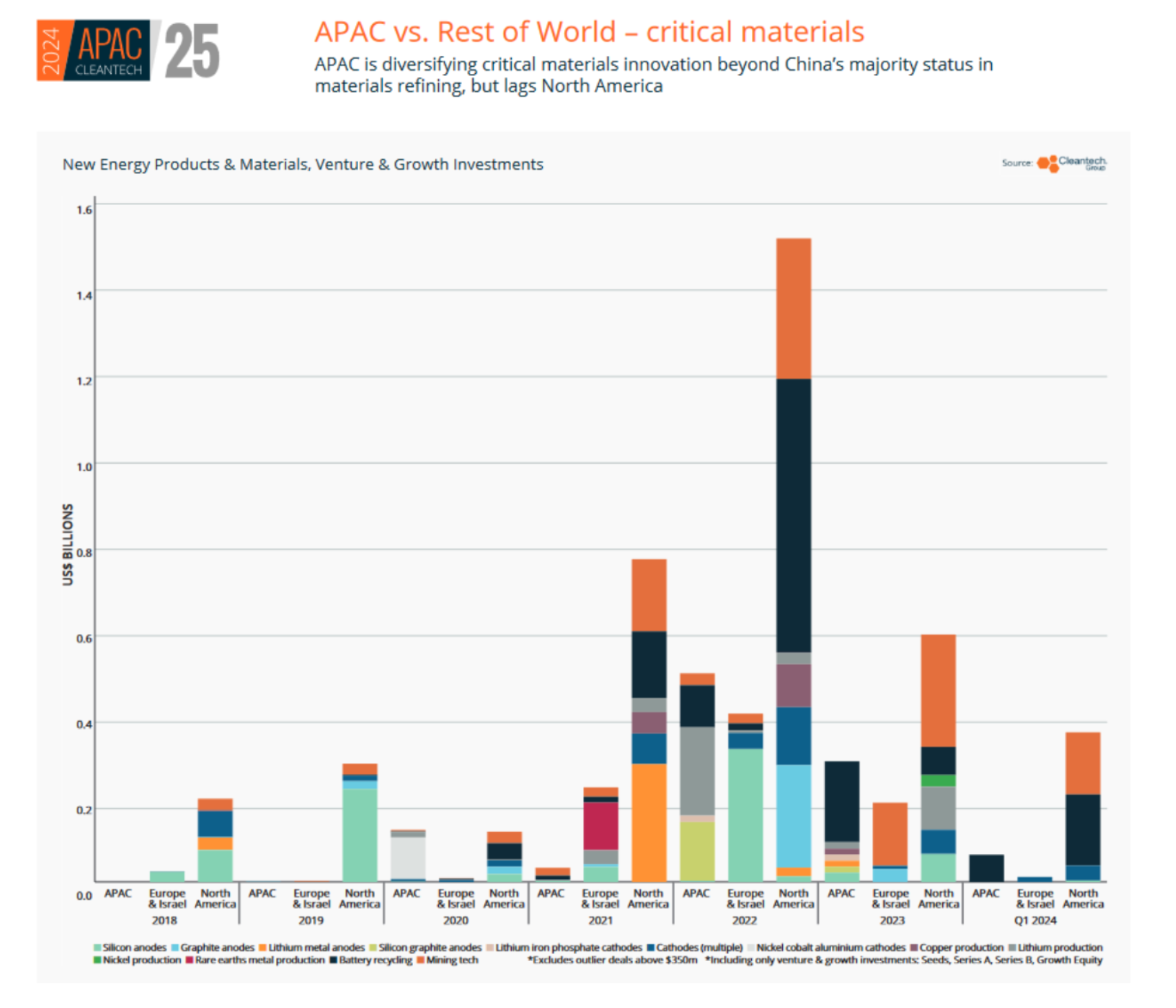

In terms of venture and growth investments in critical materials innovation, APAC has led Europe since 2022 – what is different now is that innovation is developing across the value chain but with notable progress on the furthest upstream of materials extraction and furthest downstream of battery recycling. These trends in innovation are often mirrored with protectionist policy or trade dynamics, contributing to a rapidly changing EV industry.

Innovation Sources

This year’s APAC Cleantech 25 list shows a pan-APAC effort to succeed in critical materials onshoring, but also to develop the exportable technologies that any country with an onshoring priority will want to engage:

- Novalith (Australia) uses CO2 from industrial processes to replace sulphuric acid in the lithium extraction process to produce smaller footprint lithium and flatten the carbon emissions profile of extraction.

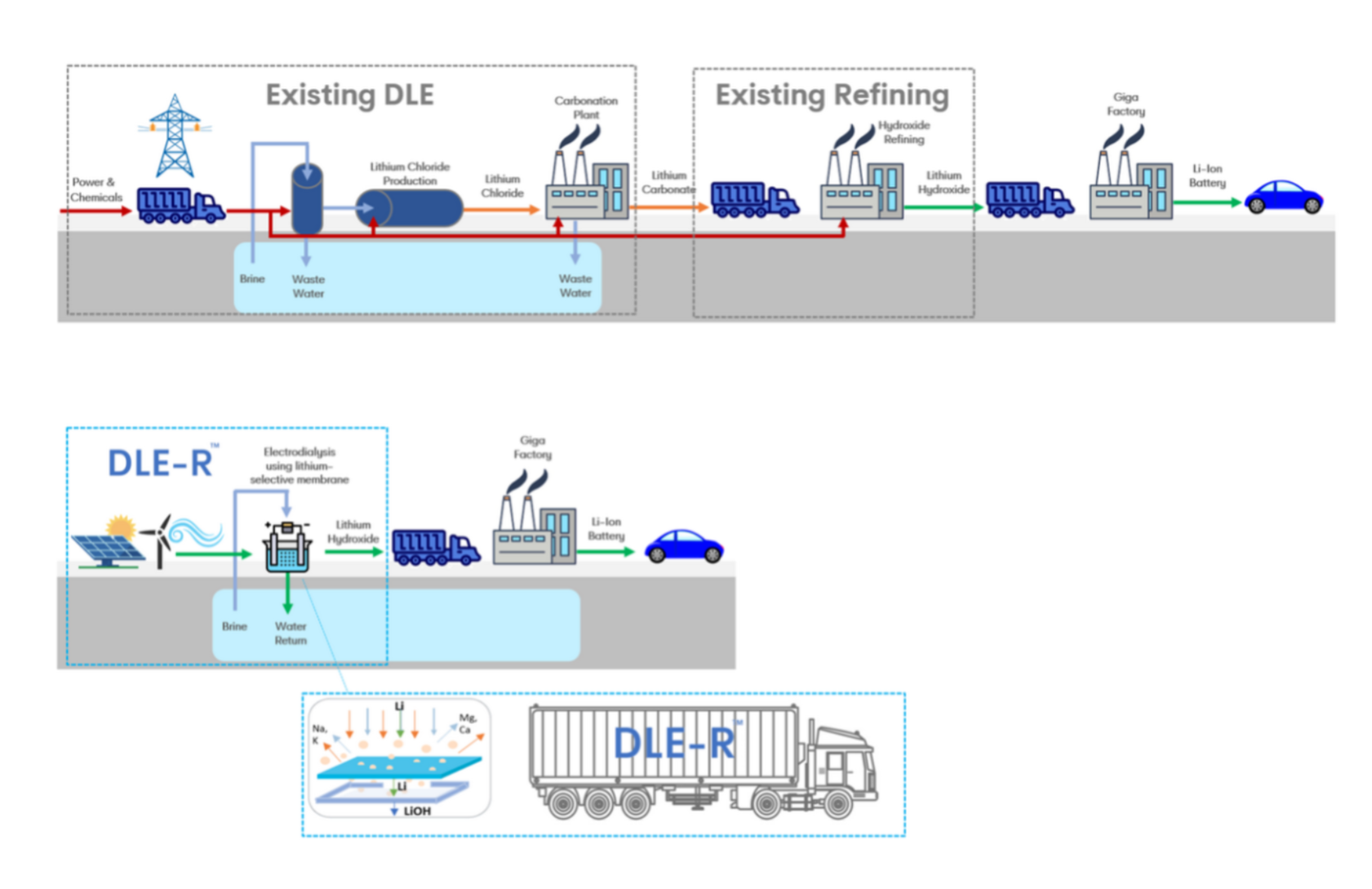

- Electralith (Australia) has further compressed the direct lithium extraction process by leveraging a proprietary membrane separation technology to extract lithium from brines and convert to lithium hydroxide in one step (versus incumbent processes that have an extra conversion step from lithium carbonate to lithium hydroxide).

- Geo40 (New Zealand) recovers silica and lithium from geothermal reservoirs, allowing for co-location with geothermal power operations.

- Sicona (Australia) has developed a silicon carbide material for batteries that has the potential to be a drop-in replacement for graphite anodes but with up to 4.5x capacity.

- Ruilong Tech (China) is recycling lithium-ion batteries at scale through 4 facilities that carry out crushing, dismantling, and hydrometallurgical processing of batteries to recover lithium, cobalt, and nickel.

Electralith’s Novel Direct Lithium Extraction and Refining Approach

Challenges to the EV Supply Chain Status Quo

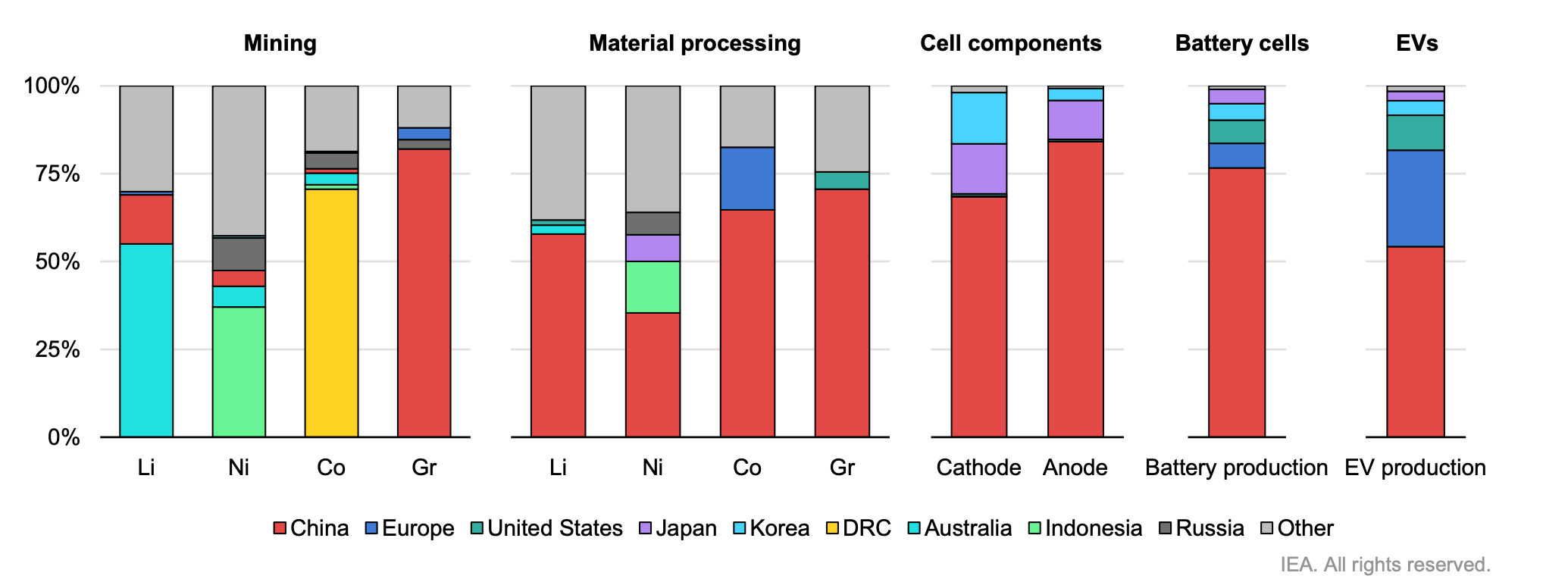

China’s dominance over the EV supply chain begins with refining the core materials for cathodes and anodes: lithium, cobalt, nickel, and graphite. Controlling over 60% of lithium refining but less than 20% of mining, China’s hold on lithium refining is precarious considering the emerging innovation coming out of Australia.

Australia is pairing lithium extraction innovation with increasing refining capacity (slated to increase from 0% to 6% of global capacity) by the end of 2024 and Envirostream’s mixed battery recycling. These cross-supply chain consolidations target a common theme in APAC and globally: leveraging existing critical mineral resources in the hopes of onshoring battery manufacturing including up to 92% domestic minerals in Energy Renaissance’s batteries.

Geographical Distribution of the Global EV Battery Supply Chain

Indonesia is also looking to onshore battery manufacturing through lucrative corporate partnerships as well as policy. While Indonesia’s battery manufacturing capacity is still low, corporate investments from CATL, Hyundai, and LG were incentivized by the country’s rich nickel deposits and EV targets for 2.1 million e-motorcycles and 2,200 e-cars by 2025.

Unlike Australia, Indonesia is not looking to reduce trade with China as Indonesian nickel production and refining infrastructure is largely owned by China. Instead, Indonesia has banned raw mineral exports to expedite domestic refining capability, slowly increasing their influence in the global EV supply chain. This policy opened the door for refining partnerships with China’s Tsingshan Holding Group in Indonesia. Without a national nickel trade deal with the U.S., China has become the dominant trade partner in the region. That said, Filipino and Indonesian politicians have expressed increasing concern over China owning domestic nickel refineries.

Both case studies hit on the larger theme of expediting domestic APAC mineral refining and LIB (Li Ion battery) manufacturing ahead of increased competition for resources and demand for EV batteries.

On the policy front, Europe and China have been the two leaders but remain interconnected. After banning black mass imports in 2018, China set mineral recovery targets (98% of nickel, cobalt, manganese and 85% of lithium from spent batteries) to accelerate its already leading recycling industry.

As the second largest EV market, the European Union enacted similar policies targeting extended producer responsibility (EPR), mineral recovery targets, and minimum recycled content peaking in 2036. It is important to note the policy pushing battery recycling forward may not necessarily advance the goal of onshoring an integrated circular battery supply chain unless “black mass” exports are also banned. Europe currently continues their reliance on Chinese mineral refining as black mass or spent batteries routinely flow out of Europe to Asian hydrometallurgy recyclers selling their outputs back to China.

Industry Outlook and APAC’s Significance

Battery recycling offers a buffer against volatile global supply chains whose price fluctuations disrupt emerging EV battery manufacturing. By creating a domestic cache of battery minerals through recycling, states in APAC and beyond reduce dependence on the traditional industry bottleneck, China. With new tariffs from the EU and U.S., China itself is diversifying its mineral control through legislation such as limiting graphite exports.