How the Insurance Sector Can Further Enable Cleantech Scaling

The insurance sector is the leading authority on risk, while scaling cleantech requires a deep understanding of risk and risk mitigation. As such, we have observed increasing synergy between cleantech and the Insurance sector. Cleantech Group recently researched the innovations and partnerships which are aligning the insurance industry with new climate realities.

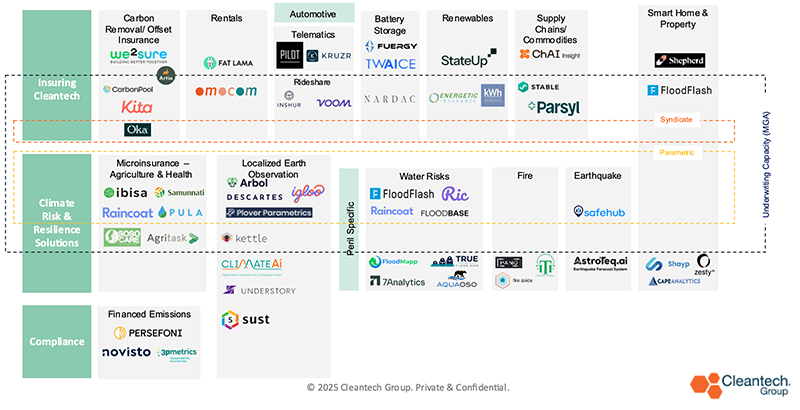

Insurance Cleantech Innovator Landscape

The insurance industry has significant, yet unrealized power in scaling cleantech markets. This blog highlights some industry leading, innovative partnerships and suggests bold actions the insurance industry should be taking next to futureproof its growth and enable global climate mitigation and resilience.

Insured losses from extreme weather events have increased astronomically in the last 30 years, by as much as 250%. But insurers continue to insure oil and gas infrastructure – the very industries which cause climate change and exasperate extreme weather events. This contradiction and seeming lack of long-term planning isn’t industrywide; many have made moves to divest and/or restrict the underwriting of oil and gas.

In 2022, Munich Re announced that as of April 2023 it will no longer invest in or insure contacts/ projects exclusively covering new oil and gas fields, midstream infrastructure, and new oil fired power plants. Other major insurance firms including Allianz, Swiss Re and Hannover Re have made similar divestment commitments, which can increase the OPEX of oil and gas projects and ultimately increase the cost of oil and gas.

Others have taken a more collaborative role. For example, in March 2023 Chubb announced it will cease underwriting oil and gas extraction projects which don’t have evidence-based methane reduction plans.

At a time where oil and gas majors are rolling back plans to cut oil production, e.g., BP changed its target to reduce its Scope 3 emissions to 20-30% by 2030 (from 35-40%), divestment is pertinent and powerful in shifting the economics away from fossil fuel industries.

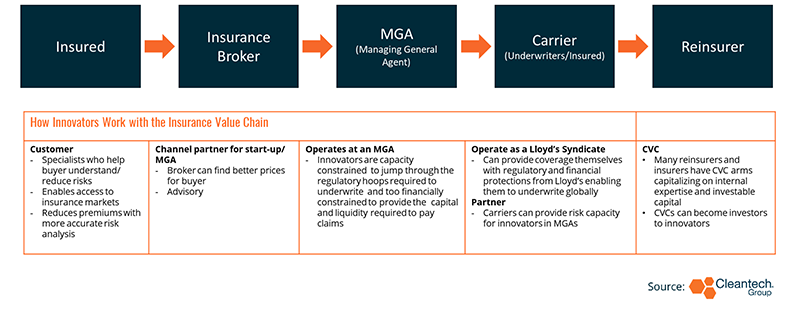

The insurance sector also has the power to improve the economics of cleantech across the whole insurance value chain (figure 1). The sector can engage with cleantech in 3 main ways:

- Create insurance products to insure a sustainable transition (e.g. Technology performance insurance)

_ - Create new risk transfer solutions, addressing risking physical climate risks (e.g. parametric insurance)

_ - Provide capital and support to innovators (e.g. CVCs, Accelerator programs)

- Create insurance products to insure a sustainable transition (e.g. Technology performance insurance)

The Insurance & Cleantech Value Chain

Insuring Cleantech: Creating Insurance Products to Insure a Sustainable Transition

Insuring Cleantech: Creating Insurance Products to Insure a Sustainable Transition

Insurers are shifting operating practices from underwriting policies based on historic data of technology performance and risks to proactively understanding their risk profile, enabling new insurance products to be created for emerging technologies. Insurance has the power to fast-track the scaling of cleantech, reducing sales cycles and unlocking new forms of finance for first-of-a-kind (FOAK) projects and to cater to high demand.

There is a growing trend for start-ups to engage the insurance industry for product warranties. Munich Re, for example, led the way with their Emerging Green Tech division, offering guarantees on things from batteries (E-Mobility Warranty), to hydrogen power, bioenergy plants, and innovative agricultural practices. These are model examples of the insurance market and cleantech working harmoniously. The insurer examines early-stage data of the technology, then guarantees the outcomes.

For a start-up, they can now shorten sales cycles often convincing more customers/investors to shorten or remove the need for lengthy or multiple proof-of-concepts. Those early-stage adopters can have greater confidence in the technology, both directly, due to the financial guarantee from the insurer, and indirectly, due to the global brand name the insurer brings.

Investment in cleantech requires investor confidence, which can be supported by insurance which reduces business and technology risks for scaling cleantech companies. Early-stage cleantech investors are high-risk, high-reward. But as cleantech companies scale, their business risk and technology risk ‘generally’ are reduced – which can enable greater access to different forms of finance, which is less or non-dilutive, e.g., debt financing.

This finance enables the start-up to finance FOAK projects and then meet demand faster, especially in hardtech. Insurance can fast-track this risk reduction via proactively understanding the technology, market, and performance risks and creating appropriate risk models and then policies specific to that technology. Therefore, the insurance industry has significant enabling power to scale cleantech innovation.

With the cleantech markets on significant growth trajectories, including hydrogen, nuclear, battery storage and carbon dioxide removal (CDR) markets, and on-going corporate and government commitments to decarbonize, there are growing opportunities for new insurance products and strategic investments. The technology transition is inevitable, and insurance can accelerate it.

The Catalyst for Change: Industry Leadership and Collaboration

Many industries struggle with collaboration in the face of the sustainability transition. In highly competitive environments, information-sharing and joint investments often take a backseat to maintaining a competitive edge. However, the insurance sector operates differently. While competition remains a driving force, insurers frequently collaborate by sharing large risks or spreading exposure through reinsurance. Brokers, too, play a critical role in balancing competition and collaboration to secure the best outcomes for clients.

At the heart of this industry sits Lloyd’s of London, a self-regulating marketplace that has facilitated insurance innovation for centuries. Lloyd’s provides a unique ecosystem where insurers and brokers operate under a common regulatory framework, ensuring smooth collaboration and competition. The central fund guarantees payouts on valid Lloyd’s policies, even if an insurer becomes insolvent, offering confidence to policyholders. Additionally, Lloyd’s global licenses enable insurers to operate across hundreds of markets worldwide.

An Innovation Legacy

Lloyd’s dominance began with its unparalleled access to shipping intelligence, making it the go-to marketplace for maritime risk exchange. Over time, it has pioneered insurance for emerging technologies, launching the first policies for motor vehicles, aviation, and space satellites. While not every innovation succeeded (e.g., airship insurance), Lloyd’s has cemented its reputation as the premier marketplace for insuring complex and unique risks—from Bruce Springsteen’s voice to Betty Grable’s legs.

Beyond underwriting, Lloyd’s has played a proactive role in industry research and crisis response. The Lloyd’s Tercentenary Research Foundation funds studies into risk management, and the marketplace has historically acted decisively in turbulent times. For instance, after the 1906 San Francisco earthquake, Lloyd’s facilitated immediate full-limit payouts. Following the 1980’s asbestos crisis, it led structural reforms to stabilize the market.

Now, as the world faces climate change—arguably the largest evolving risk—Lloyd’s has an opportunity to drive industrywide collaboration in support of cleantech solutions.

Lloyd’s has already taken steps in this direction. In 2021, it launched the Sustainable Products and Services Showcase, highlighting innovative insurance solutions from industry leaders. Its Lloyd’s Lab accelerator program has nurtured insurtech start-ups such as Kita (carbon offset insurance) and AstroTeq.ai (earthquake forecasting technology). These initiatives demonstrate Lloyd’s ability to foster innovation, yet focused engagement with the cleantech industry remains limited.

A Call for More Focused Action on Cleantech

While Lloyd’s remains neutral regarding divestment from fossil fuels, it can do more to leverage its market position in favor of cleantech. Currently, non-profit initiatives like InnSure in the U.S. are leading the way. InnSure’s climate initiative platform recognizes insurance as a critical enabler of clean energy deployment. In January, InnSure partnered with Energetic Capital, kWh Analytics, and the Coalition for Green Capital (CGC) to launch GreenieRe, an impact-focused reinsurance company designed to remove financial barriers for clean energy projects. With an initial $200M investment from CGC, the initiative aims to unlock over $30B in private-sector financing for renewable energy.

Lloyd’s is uniquely positioned to take similar bold action with the contacts, authority, and deep pockets to bridge information gaps in cleantech and facilitate innovative partnerships to unlock scaring cleantech. At a time when its relevance to a modernizing insurance market is under scrutiny, it has a rare chance to lead, organize, and innovate at an industrywide scale. By championing cleantech investment and insurance solutions, Lloyd’s can not only help mitigate climate-related risks but also secure its own long-term role in the evolving insurance landscape

Parametric Insurance: New Risk Transfer Solutions to Address Risking Physical Climate Risks

According to AON, In Q1 – Q3 last year (2024), the insurance protection gap was estimated to be 60% ($258B of economic losses vs. $102B of insured losses) and is growing, leaving communities, businesses, and individuals without a financial backstop for climate risks. The LA wildfires this year are estimated to cause as much as $250B in economic damage and account for 4% of California’s GDP.

These increasing extreme weather events are reducing the financial resilience of communities – after each loss, insurance premiums increase for communities in Cat-loss-prone areas, leading to more people being priced out of buying insurance. A negative feedback loop is created where the insurance gap then widens after each event, pushing the cost of damage onto taxpayers, downgrading the whole communities’ credit, devaluing properties and communities. One such solution to bridge the protection gap is tech-enabled parametric insurance.

Parametric Insurance: Rather than estimates via retrospective data and payouts based on loss, parametric insurance makes projective estimates of risk via advanced climate data models. These are being used to hyper-localize risk profiles for specific insurance lines (property) and perils (flood) and payout based on triggers.

Triggers can be verified by direct sensing (e.g., water sensor for flooding severity) and can enable fast feedback of event severity to replace sending loss adjusters and can enable fast payouts – however, as the sensor is in the client’s possession, reinsurers have raised fraud concerns. Instant payouts should reduce the overall cost of claims for insurers, saving on costly administrative loss-adjusting, and enable greater resilience for the insured.

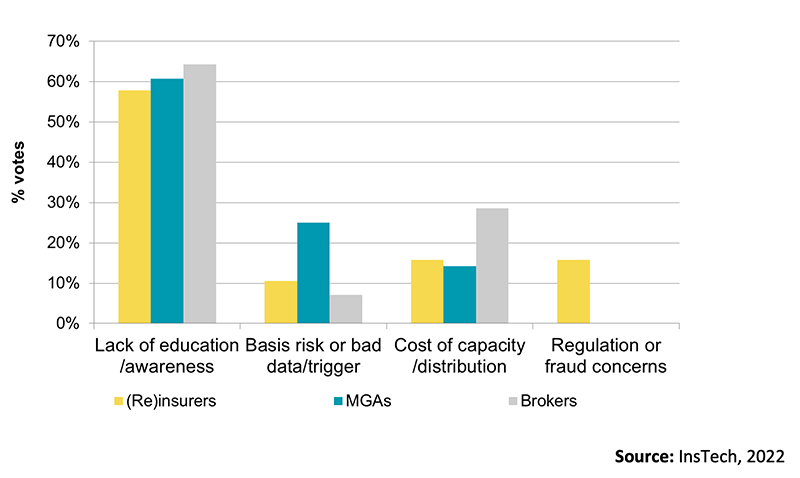

InsTech Poll: Poll of Insurance Professionals on What’s Holding Parametric Insurance Back

Amongst other innovators, Cleantech Group spoke to Tanguy Touffut, CEO and co-founder Descartes, a leader in parametric insurance solutions. When speaking on the future of parametric insurance, Touffat said, “With the support of our partners, we will continue to develop and deploy a new generation of insurance products that are entirely tech-driven, simpler, more transparent and quicker to pay in the event of a loss – adapted for the new risks corporations and governments increasingly face.”

In speaking on the disruptive future of parametric insurance Touffat said, “Parametric insurance can both replace or complement traditional insurance; that being said, we expect to see more covers combining parametric insurance for speed and transparency for Cat perils with traditional insurance for non-Cat perils.”

What’s Holding Parametric Solutions Back?

Lack of Knowledge. In the case of parametric insurance, the insurance insider polled dozens of insurance experts in 2022 finding lack of education and awareness as the greatest barrier (52%) as to why more insurers hadn’t taken up parametric insurance. This is especially the case for retail brokers who are on-the-ground selling these products. Cleantech Group spoke to parametric insurance innovators, with most identifying brokers as key sales channels they needed to establish. Conversely, brokers should be more proactive in exploring these opportunities in cleantech.

Tech Gap. A more recent poll of insurance professionals on the obstacles to parametric insurance in August 2024 by Reinsurance News found that lack of data and models was the greatest obstacle to global adoption. This presents challenges where there may be misalignment between the pre-agreed parameters for the payout and the actual losses, necessitating the use of loss adjusters and delaying payouts after all.

However, many advanced and projective models do exist, accounting for complex, compounding risks of climate change, e.g., Descartes, Sust Global or Jupiter Intelligence. These solutions are also getting smarter, with proprietary and regionally-focused models, AI, and greater access to more accurate satellite data. Insurers need to explore partnerships with these innovators to advance and customize their models or outsource underwriting capabilities.

A Note of Caution

Capitalizing on emerging markets in cleantech, insurers are working with innovators in earlier stages and in more varied sectors which can fast-track scaling. However, insurers can wield significant power in shaping these markets – so they must invest in internal and external expertise to appropriately support, mitigate risks, avoid red-tape, and ultimately scale cleantech.