Innovation Without Borders: APAC Cleantech 25 and the Global Energy Shift

We would like to extend our congratulations to this year’s APAC Cleantech 25 awardees. In recent years, we have covered in detail the meteoric rise of the APAC region within the global cleantech innovation landscape.

This year’s APAC Cleantech 25 offers a glimpse into the next generation of innovation to emerge from the region, while the major sources of growth – primarily Chinese solar and energy storage – have recently reached industrial maturity.

The headline investment numbers tell two stories: One around the speed with which Chinese solar and storage companies were able to accelerate through, and out of, the equity financing continuum to scale, and another about the speed with which the region (China and beyond) is laying the groundwork for an electrified economy at scale.

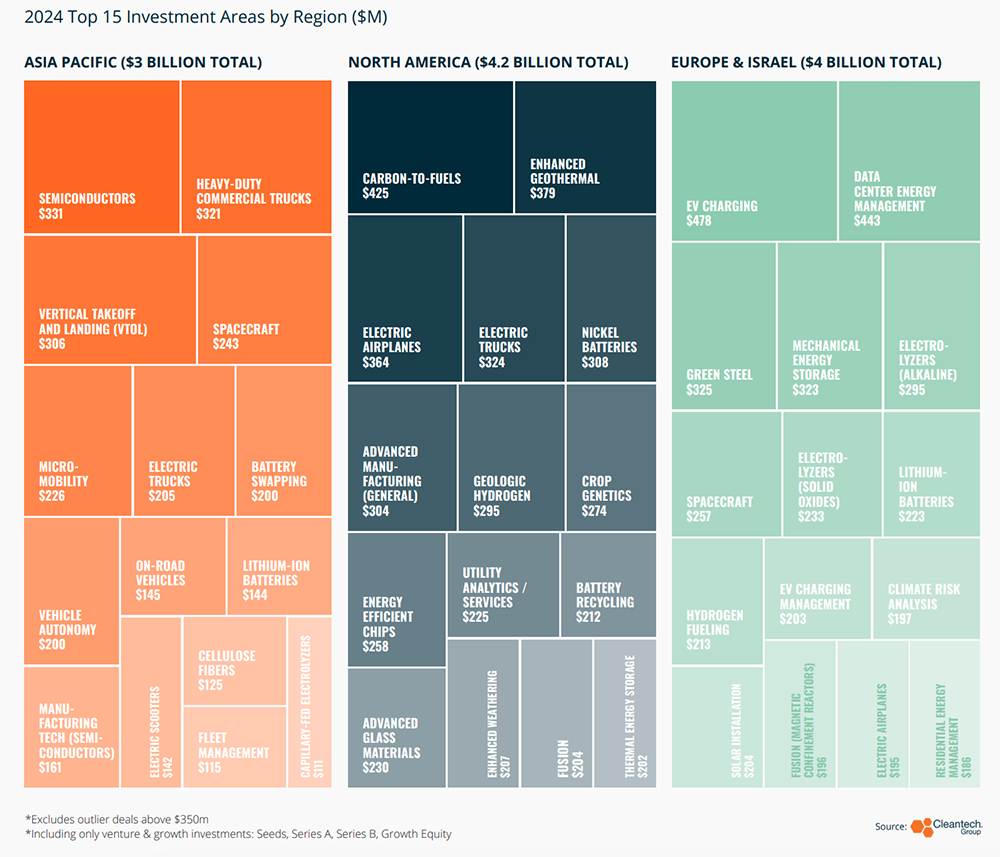

Look to the examples of innovation in electric mobility infrastructure in this year’s APAC Cleantech 25 as an indication of the region’s ability to quickly adopt innovative technology in the mainstream.

APAC’s EV innovation has consistently been centered in China, but we’re now observing expansion beyond just on-road vehicles.

The electrification wave is sweeping through heavy-duty commercial trucks and off-road industrial vehicles. Additionally, charging infrastructure and battery swapping solutions are reaching mass scale, facilitating easier EV adoption and minimizing development risks for electric heavy-duty and industrial vehicles.

For the APAC region, 2024 marked the strongest year yet in electric vertical take-off and landing (EVTol) and unmanned aerial vehicle (UAV) investments – with China’s “low-altitude economy” initiatives highlighting this emphasis.

Electric mobility infrastructure innovation extends beyond China as well, as demonstrated by these examples from this year’s APAC 25:

- Battery Smart (India): Since its 2019 launch, has evolved into India’s largest battery swapping network for two- and three-wheel vehicles

- Kwetta (New Zealand): Offers modular EV, fleet, and bus charging depots without requiring grid upgrades

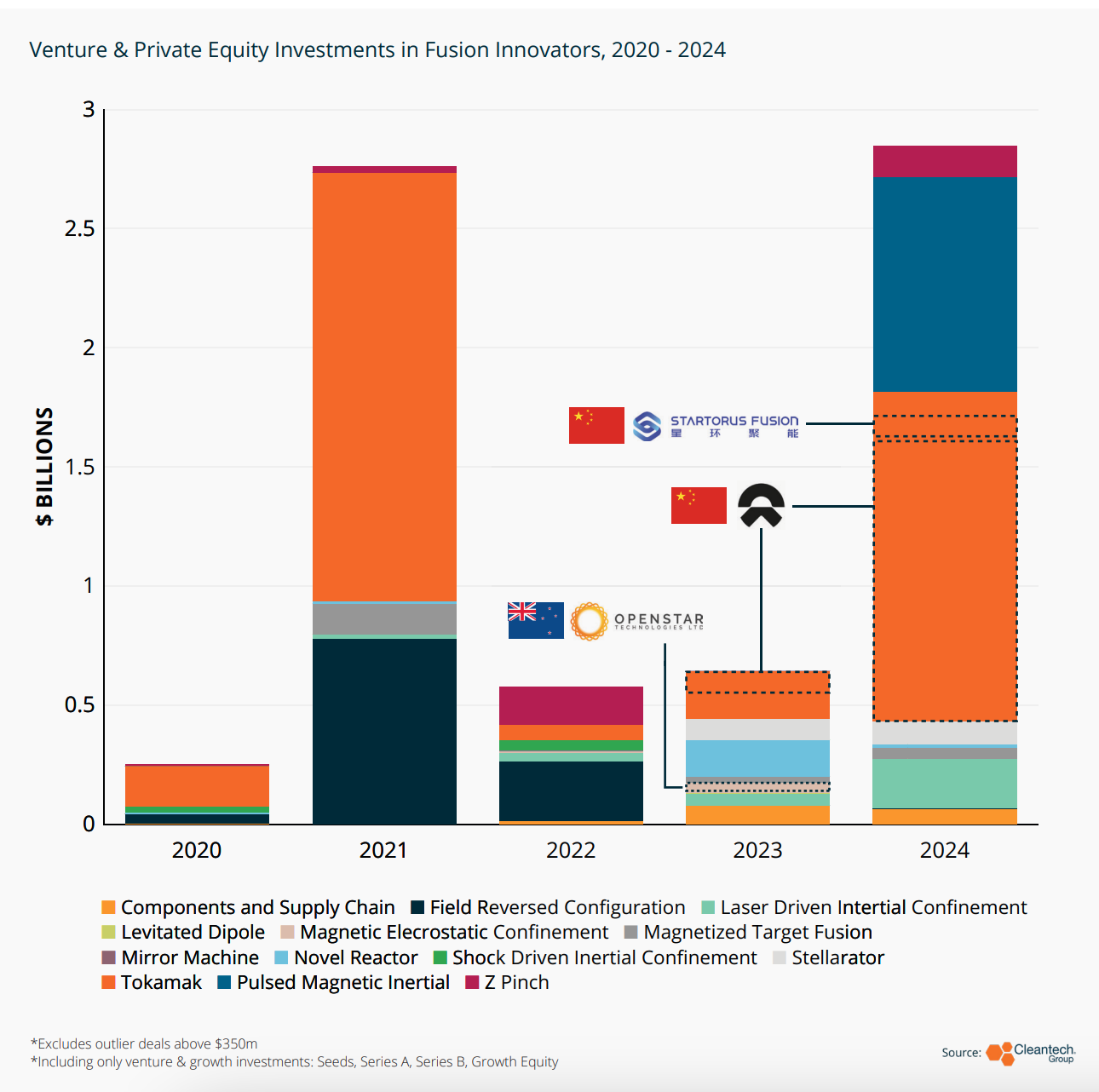

While most Energy & Power innovation sectors experienced fundraising declines over the past two years, fusion stands as a notable exception. At Cleantech Group, we’ve observed that this technology, often viewed as the future’s beacon, had a breakthrough year in 2024, featuring more geographic diversity in fundraising and more variety in reactor types.

Undoubtedly, part of this shift stems from investors becoming more familiar with fusion milestones and growing comfortable with the financing requirements needed to fund companies through their next milestones. This differs from previous years when companies received funding for smaller milestones, resulting in down rounds and higher capital costs.

Perhaps more significant, however, is the milestone progress being observed across different reactor types. Several examples from the APAC 25 include:

- Startorus Fusion (China): This spherical tokomak company, launched from Tsinghua University, reported being first worldwide to achieve an optimized spherical tokamak plasma configuration in 2024

- Openstar Technologies (New Zealand): Their levitated dipole reactor achieved first plasma in November 2024

- Kyoto Fusioneering (Japan) (2024 APAC Cleantech 25 company): Though not a reactor company, they develop components and provide fusion plant design and engineering for various reactor types (magnetized target, magnetic confinement, inertial confinement), with multiple testing facilities planned

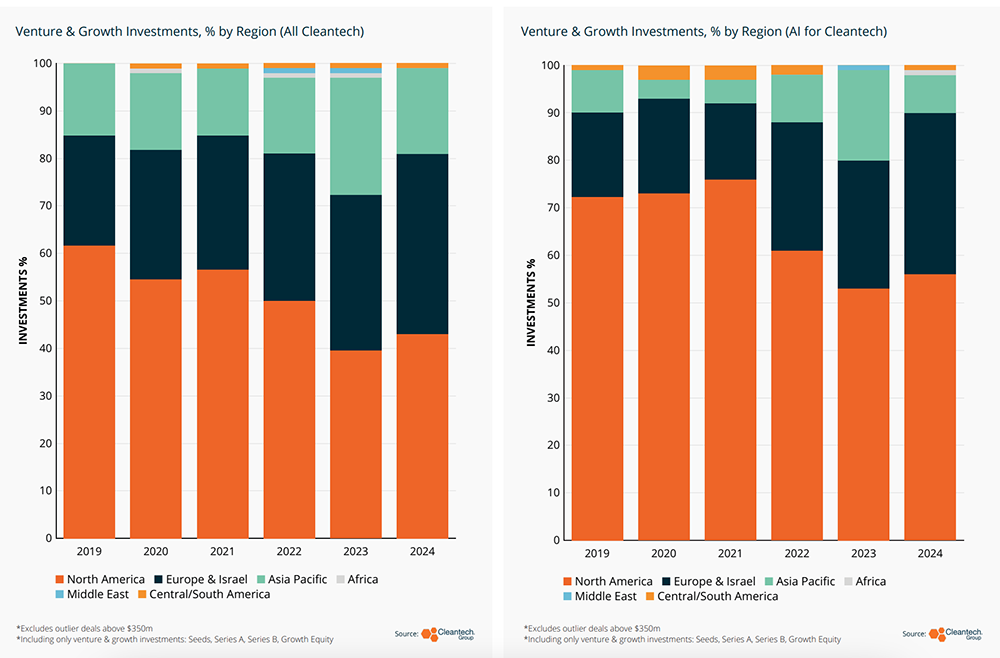

When we initially mapped AI-for-cleantech companies, we noticed a surprising lack of APAC innovators. Our hypothesis was that many simply weren’t yet in a stage of market-facing publicity. This was partially confirmed by Deepseek’s announcements in late January 2025.

While industrial efficiency has improved significantly across much of APAC, even countries making the greatest strides (China, Vietnam, India) remain far from maximizing output per hour worked. Combined with a tightening global economy and emerging overcapacity challenges in China, we expect process and resource efficiency to become top priorities for APAC companies. AI provides momentum for firms already on this improvement trajectory.

The emerging APAC AI-for-cleantech ecosystem is addressing highly localized problems while extending beyond traditional cleantech strength areas. This year’s APAC Cleantech 25 includes instructive cases of localized models with global market potential:

- Cosmos Innovation (Hong Kong SAR): Leverages their internal AI (Mobius) for materials discovery and process optimization in perovkskite/tandem solar cells production, enhancing solar cell performance while controlling R&D costs

- Ecolibrium (India): Provides an industrial efficiency AI platform aimed at reducing process waste and operational costs in high-volume, low-margin industries like commodity manufacturing and mining, while also working to optimize high-load sites such as data centers

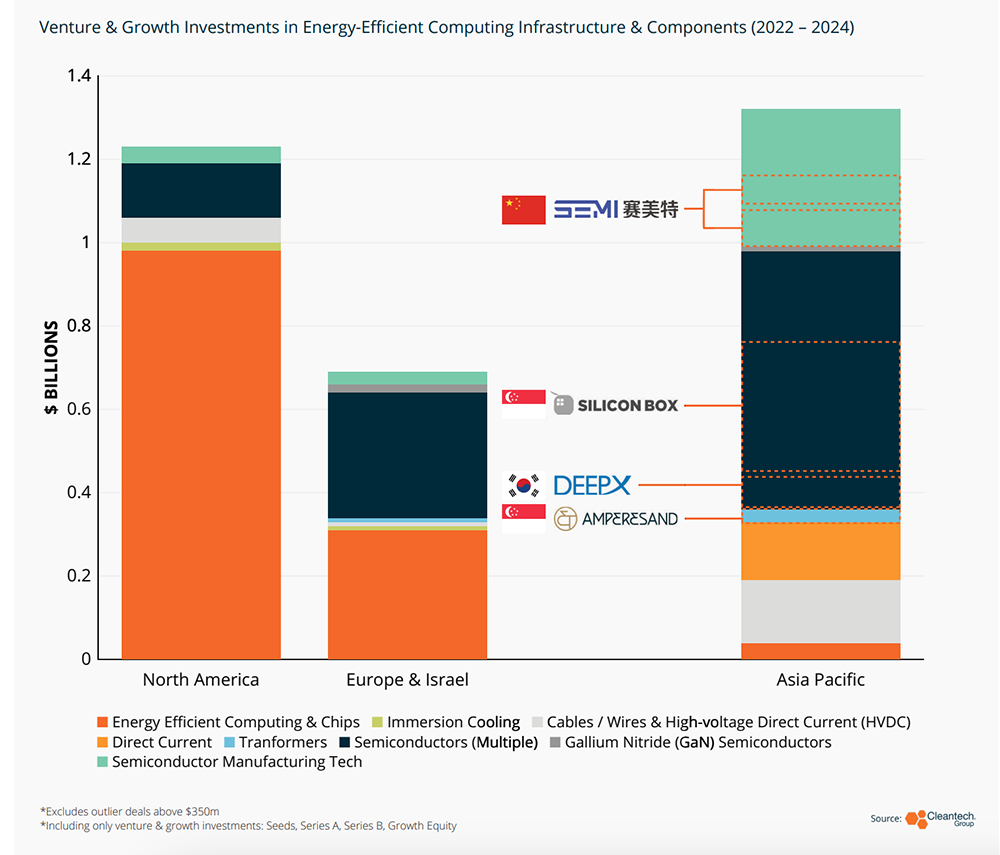

Outside China, most APAC regions cannot deploy renewables at the same pace as AI development (and its supporting infrastructure). Consequently, Asia-Pacific is rapidly becoming competitive ground for technologies reducing data center energy consumption.

APAC innovators have opportunities across the spectrum—from energy-efficient AI-supporting chips and semiconductors, to deep cooling of compute operations and more efficient IT equipment (as seen in Singapore’s Green Data Center Roadmap). Recent investment trends clearly indicate this opportunity is being recognized.

This year’s APAC 25 features companies addressing these urgent needs:

- Firmus Technologies (Singapore): Offers liquid-cooled data centers (both retrofits and new builds) and low-carbon hosting solutions with their Sustainable Metal Cloud service

- Amperesand (Singapore): Develops solid-state transformers that provide more granular power flow control across high electricity load sites, with modular and scalable designs offering additional resilience through fault isolation capabilities

For years, critical materials innovation has centered on two hypotheses:

1) Demand for battery, electric motor, and power electronics materials will exceed supply in coming decades, and

2) China’s supply concentration will require other countries to increase onshore supply

The second hypothesis is accelerating as global trade tensions rise and previously reliable supply relationships face fracture risks. The next five years will certainly see increased demand-side insecurity around these challenges.

Addressing both challenges requires improved mining efficiency and precision, new refining techniques, and materials recovery from waste. This year’s APAC 25 showcases the full value chain with diverse geographic representation:

- Fleet Space (Australia): Provides satellite-based critical mineral detection

- Element Zero (Australia): Offers non-aqueous electrochemical processing of ores (iron, nickel, silica) into high value materials

- 3DC (Japan): Produces three-dimensional graphene material sponge applicable in current lithium-ion batteries and future chemistries (e.g., solid state)

- Poen (Korea): Specializes in spent and damaged battery assessment, remanufacturing, and re-purposing

- Lohum (India): Focuses on battery recycling and recovery of lithium, cobalt, nickel, and graphite through a hydrometallurgical process

As of time of writing, the fast acceleration of global trade fractures is making the possibility of “regional technology spheres” even more likely. Especially given that so many of this year’s APAC Cleantech 25 are innovating in technologies crucial to the next decades of sustainable industry, we expect to see the trends named above intensify even further.

We once again congratulate all of this year’s APAC Cleantech 25 award recipients!