Maritime eFuels: Bridging the Market Gap

The maritime sector, though in many ways a conservative and slow-moving industry when it comes to innovation, has quietly set itself up to be one of the most progressive industries in terms of sustainability and decarbonization. The International Maritime Organization has set ambitious decarbonization targets and emerging international and industrywide regulations and standards are spurring global shipping actors to reduce emissions and adopt more sustainable solutions.

One of the major hurdles standing in the way of deep decarbonization of the maritime sector is the challenge of the development, deployment, and uptake of more sustainable fuels. While some emissions reductions can be gained by a range of low-emission vessel innovation solutions, such as route optimization software, wind-powered propulsion, or existing bio-based fuels on the water today, limited scalability and an inability to achieve near 100% emissions reduction impacts the long-term viability of these solutions. It is becoming increasingly clear that long-term decarbonization of the maritime space will require the widespread uptake of e-fuels.

Biofuels and LNG (liquified natural gas) have been two of the initial solutions but have had feedstock bottlenecks and relatively low emissions reductions. A recent report by the Maersk-McKinney Moller Center for Zero Carbon Shipping found that the EU fleet is on track to meet 90% of required emissions reduction through 2029 with biodiesel and LNG alone. However, as emissions reduction requirements become increasingly stringent, projected use of biofuels and LNG will only meet about 30% of requirements for 2030-2034.

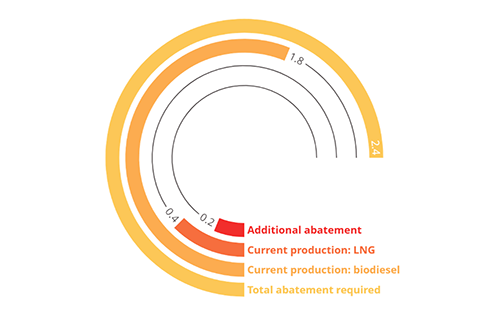

Fuel Use to Meet 2025-2029 2% Emissions Reduction Target (in Mil tonnes CO2eq)

Source: Data from Maersk-McKinney Moller Center for Zero Carbon Shipping

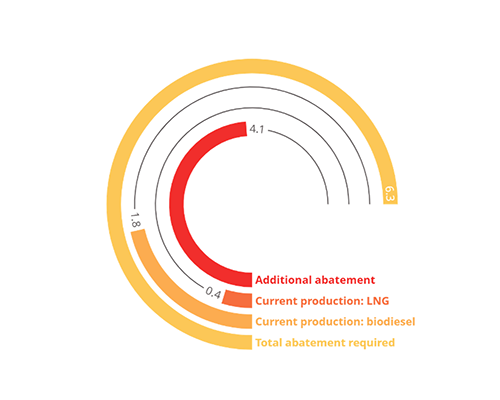

Fuel Use to Meet 2030-2034 6% Emissions Reduction Target (in Mil tonnes CO2eq)

Source: Data from Maersk-McKinney Moller Center for Zero Carbon Shipping

E-Fuels Needed to Meet Future Abatement Gap

E-fuels, or synthetic hydrogen fuels (90%+ emissions reductions compared to conventional bunker fuel), are seen by many as the only viable pathway for deep maritime decarbonization. Significant challenges remain that hinder the widespread market uptake of e-fuels, including barriers from high production costs, limited renewable energy capacity, technical roadblocks, and storage and handling challenges.

Additionally, uncertainty around which e-fuels will be most competitive and market-ready slow decision-making from fleet owners and operators, diminishing market demand and investment in the near term. A number of industry actors, however, are taking up the challenge of addressing these key barriers to the development and deployment of e-fuels in the maritime sector, whether that be providing infrastructure funding to scale up e-fuel production projects (e.g., Breakthrough Energy) or piloting e-fuel bunkering solutions and standards (e.g., MPA Singapore).

Market Mover Spotlight: Zero Emission Maritime Buyers Alliance (ZEMBA)

Discussions on “bridging the gap” in terms of scaling cleantech innovation tend to focus on the investment gap. However, the market demand gap for sustainable innovation is an equally daunting challenge. ZEMBA is working to bridge this classic “valley of death” that many new markets face between research and development and the significant scaling then required to facilitate robust commercial deployment.

ZEMBA describes the challenges facing the maritime sector as a fundamental chicken-and-egg problem in developing and scaling a market for new clean energy-derived fuels and technologies. Demand is stymied by high initial predicted costs of shipping services powered by these solutions. A resulting lack of sufficient committed demand from corporate freight buyers (cargo owners) erodes investor confidence, as well as appetite for risk among maritime stakeholders who will need to order new types of vessels, build new fuel production facilities, and create supportive policy at global, regional, and national levels.

What are the basics of ZEMBA’s operations? How does the tender process work?

ZEMBA members represent the end customer in the maritime value chain, and within this sector, they have historically relied on the carriers they use to provide them with greener solutions. However, no freight buyer is big enough on their own to incentivize the market to transition to new scalable solutions like e-fuels.

This is why ZEMBA works to pool freight buyer demand, bringing together the buying power of over 40 companies around the world. Through ZEMBA’s tenders, willing buyers (i.e., aggregated demand) are brought together to signal their demand early, giving the market time and confidence to address these market development challenges, prepare the required infrastructure, and deliver over longer contracts.

ZEMBA´s first tender was launched in 2023, for 3.5 billion TEU-nautical miles of zero emission shipping services over a three-year period. This inaugural tender marked the first-ever collective multi-year offtake commitment for near-zero greenhouse gas (GHG) shipping. When completed, 17 members signed bilateral agreements with winner Hapag-Lloyd and will receive the emissions reduction associated with the ZEMBA tender in 2025 and 2026.

NOTE: ZEMBA organizers comment that they were somewhat surprised that they received no bids for e-fuel powered shipping— despite numerous announcements at the time about new e-fuel production projects, e-fuel-capable vessels on order, and ZEMBA setting a 90% lifecycle emissions reduction target for bids.

In response to the lack of market for the e-fuels that will be critical to meeting future emissions abatement, ZEMBA has recently launched its second tender, seeking bids from the containership segment specifically for e-fuel-powered shipping. At the end of the tender process, ZEMBA members will contract with the winning carrier for just the premium associated with deploying the e-fuel service compared to a fossil fuel service. In return, ZEMBA members receive in-sector, in-value chain emissions reduction credits. ZEMBA aims to announce the successful conclusion of this e-fuel-focused tender by the end of 2025.

The uncertainty of which e-fuels will be most competitive and market-ready is a divisive topic at the moment, particularly surrounding methanol and ammonia. What has ZEMBA observed regarding the demand and market-readiness for these two fuels?

ZEMBA remains open to any qualifying e-fuel-powered bid; you can see our RFP 2 ZEMBA Eligible Fuel Requirement document to learn more about how we define that in technical terms. To answer your question, our RFI results demonstrated that for containership services launching in 2027, e-methanol-powered container shipping services represent the most likely bid pathways because of strong alignment between e-methanol production and methanol-capable ships. E-ammonia fuel production was projected to have a similarly strong growth trajectory as e-methanol in the years ahead, however the first potential e-ammonia-capable containerships are rolling out more slowly than many had hoped. Until there are containerships ready to use that fuel, we may see the initial progress on ammonia in other segments of shipping like bulkers and tankers that transport commodities rather than consumer products.

How would you respond to VC/CVC investors that think there is little to no opportunity for venture investment in the maritime decarbonization space? Do you agree? Are the key opportunities mainly infrastructure-level investments?

There are absolutely opportunities to invest in new companies designing new innovations. Maritime shipping is a huge industry that is the backbone of global trade. A lot of the investment needed is in big infrastructure projects, but this maritime clean energy transition will also require new software, new equipment for vessels and port operations of various sizes, new data management systems, etc.

A combination of public policy and voluntary corporate action through efforts like ZEMBA will support creation of entirely new markets for low-emission solutions. Like many sectors, is it a challenge to know what customers will want in the future, of course, but we suggest VC investors take a look at the criteria ZEMBA puts out for our tenders. We are building this future market right now, offering clear specifications for the kind of solutions that we know shipping’s corporate customers are looking for in the years ahead. They are more than welcome to look to us as they seek to read the tea leaves.

For a tangible way to get involved in the innovative aspects of the maritime sector, ZEMBA and Lloyd’s Register Maritime Decarbonisation Hub will be hosting a Maritime Innovation Trade Fair this spring, a webinar highlighting innovators working to create a scalable, sustainable, and reliable maritime sector of the future that are outside ZEMBA’s current tender.

Quotes attributed to CEO Ingrid Irigoyen and ZEMBA.