Q1’24 Trend Watch: Steel, Cement, Energy, China & Europe

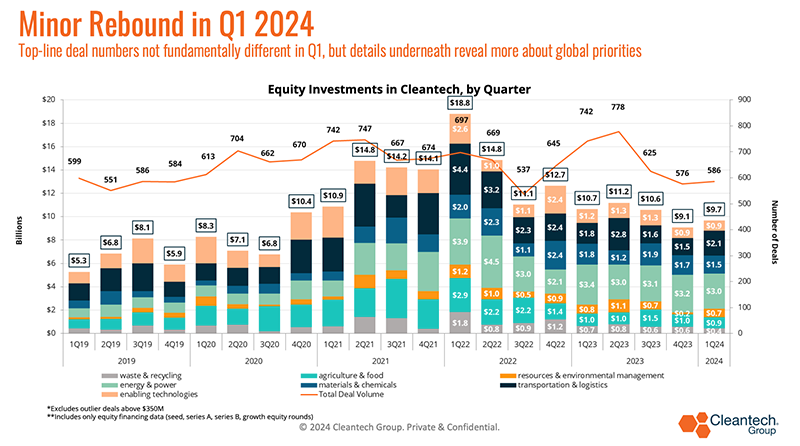

In Q1 of 2024, we saw more of the “new normal” in venture & growth investing – following the explosive years of financing during the pandemic, equity financing levels have essentially leveled out but have settled at average levels higher than the averages pre-pandemic.

Some things that were unique to Q1:

- Significant activity in the hard-to-abate sectors, e.g., steel and cement (more on these later) – these were the industries traditionally considered most difficult to decarbonize and the technologies most risky to back financially, but they have seen consistently strong investment quarters.

- Despite some of the lingering doubts around transitions to hydrogen, hydrogen production technologies saw a very strong venture quarter – underpinned largely by enthusiasm over new geologic hydrogen exploration technologies.

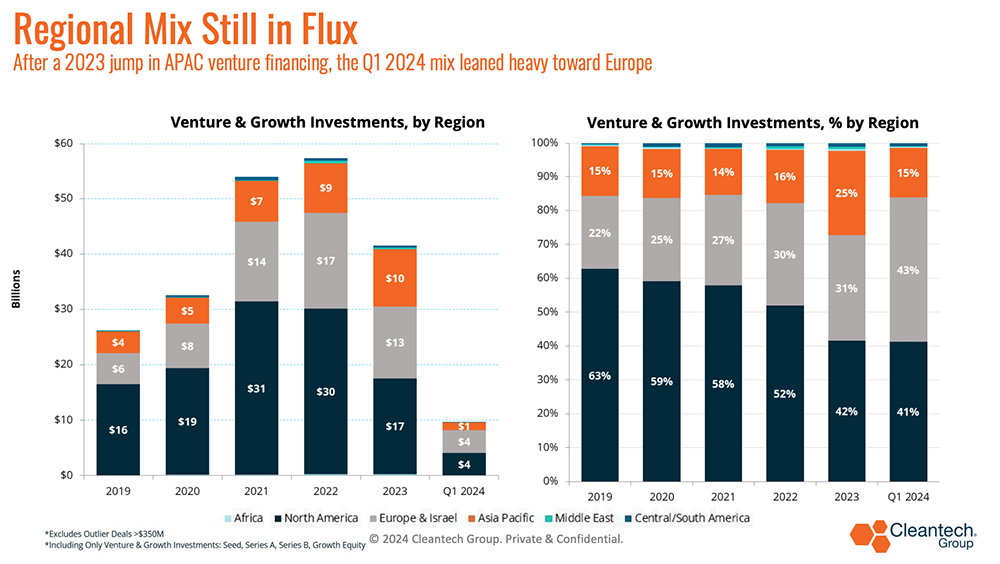

- Another quarter of a “cooling” in Asia-Pacific (continued from Q1 2023) versus the very significant jump, especially in Energy & Power financing in most of 2023 – the mix shifted heavily European in Q1 with the Europe growth case mostly coming from Transportation & Logistics tech (see below).

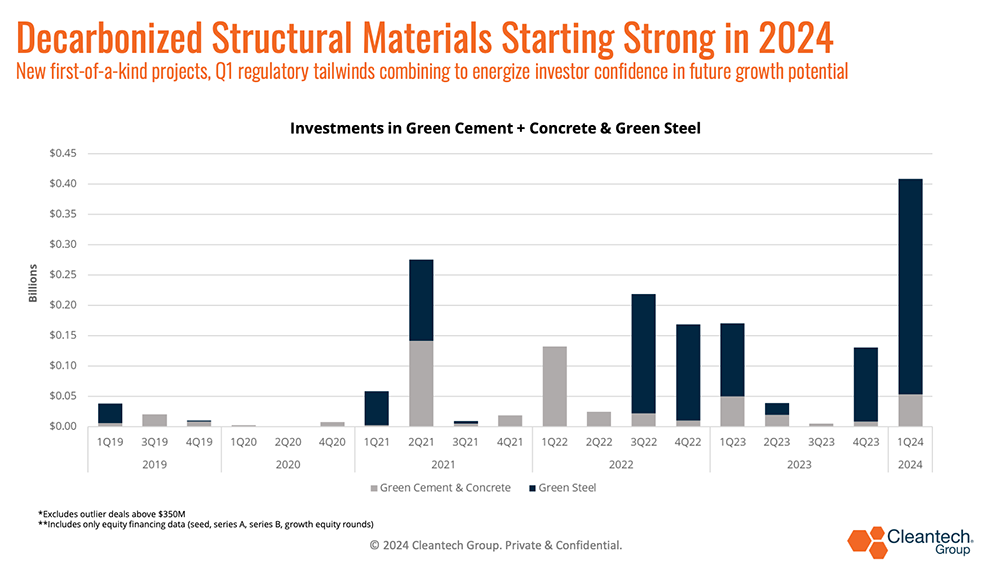

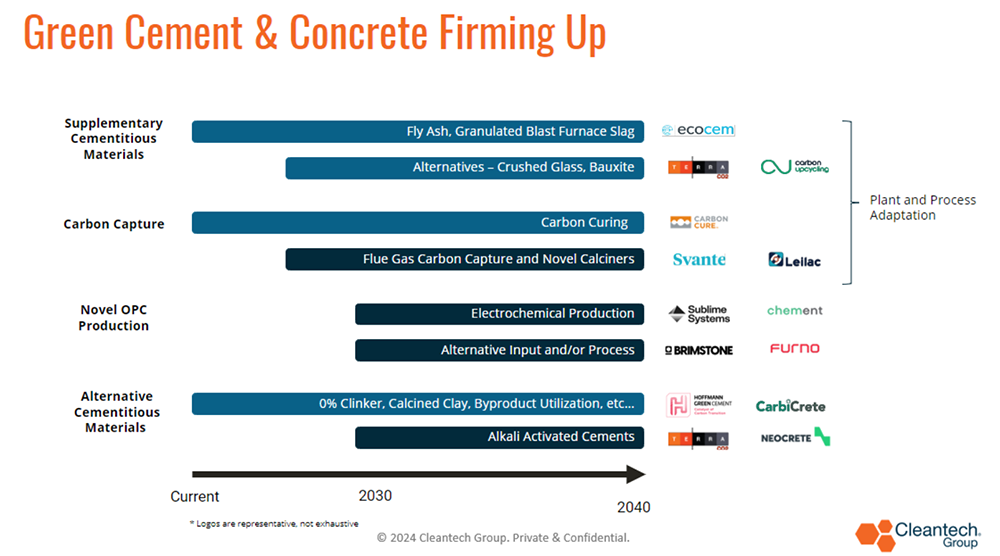

Cement and Concrete Headline Q1

The early activity in green steel and green cement and concrete is one of the headline stories of this first quarter. These traditionally hard-to-abate sectors now have enough of a slate of innovative solutions to start charting a path forward to decarbonization.

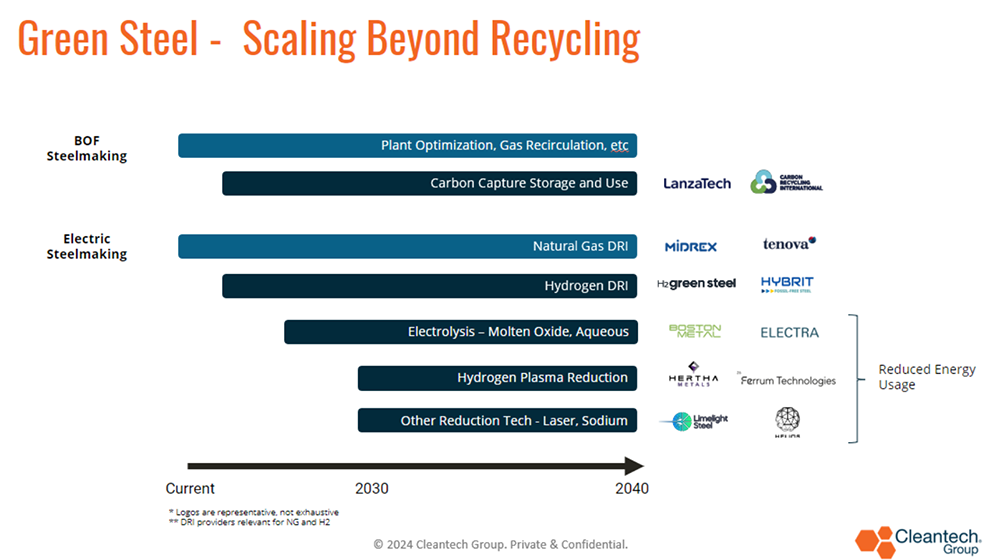

We are now at an interesting stage in which there are new green steel and cement production technologies that are entering the market (mostly through demonstration plants, but some at commercial scale) – a first “tranche” of technologies is emerging while the more nascent technologies are seeing more venture support (see diagrams below for our take on the “tranches” of green steel and green cement development):

Some key deals in these spaces from Q1 2024:

- H2 Green Steel raised $325M Growth Equity from Microsoft Climate Innovation Fund, Mubea, and Siemens Financial Services in parallel with a $4.55B debt round. The funding will be in support of continued expansion of the company’s large-scale production facility

- Boston Metal raised a $20M Growth Equity round now totaling $282M to demonstrate its technology commercially

- NeoCem raised a $25M Series A for a pilot facility from a consortium of players including BPI France

- Furno Materials raised $6.5M Seed from Breakthrough Energy and others

The Biden Administration recently announced $6B for 33 projects in hard-to-abate sectors, some innovative solutions benefitting directly include:

- Low-carbon Cement

- Deeply Decarbonized Cement (up to $189M) by Brimstone

- First Commercial Electrochemical Cement Manufacturing (up to $86.9M) by Sublime Systems

- Decarbonized Process Heat

- Steam-Generating Heat Pumps for Cross-Sector Deep Decarbonization ($up to $145M) by Skyven

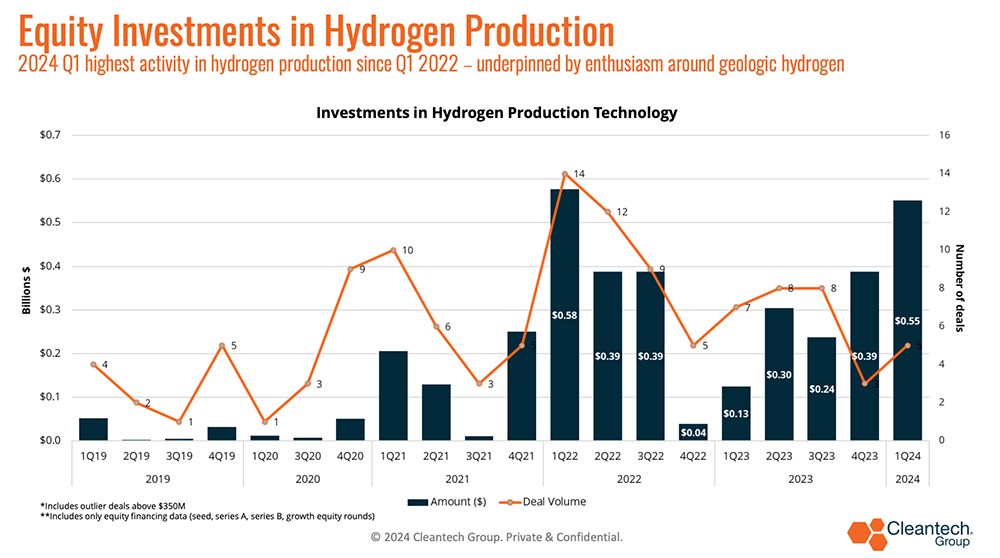

Hydrogen Also Shows Investment

Perhaps not unexpected, per se, but certainly the hopes around potential for geologic hydrogen became more palpable this past quarter. See the chart below, where Q1 was the most significant in terms of equity financing toward hydrogen production technology – the over half a billion dollars spent consisted of investment in multiple hydrogen production pathways, but was significantly underpinned by a $245M Series B round invested in white hydrogen company Koloma days after Koloma also received a $900K grant from the U.S. Department of Energy, and less than a year off a $91M Series A round.

The enthusiasm around geologic hydrogen (hydrogen that occurs naturally in underground reservoirs) is two-fold:

1) It is hydrogen that is extracted and not produced through a thermal or electric process

2) As a result, it avoids carbon emissions from production processes.

Accessing geologic hydrogen in a low-cost way would reduce the need to build out new renewables to produce green hydrogen and, in theory, trade electricity cost for cost of compression, transport, and storage of hydrogen.

Looking Towards Q2

- Commercial traction and offtake agreements will be the KPI for companies hoping to exit the equity financing continuum out to bankability. This may be an obvious statement, but companies that are able to find creative ways to access pockets of willingness-to-pay are going to begin a journey to lower cost of capital sooner than their competitors.

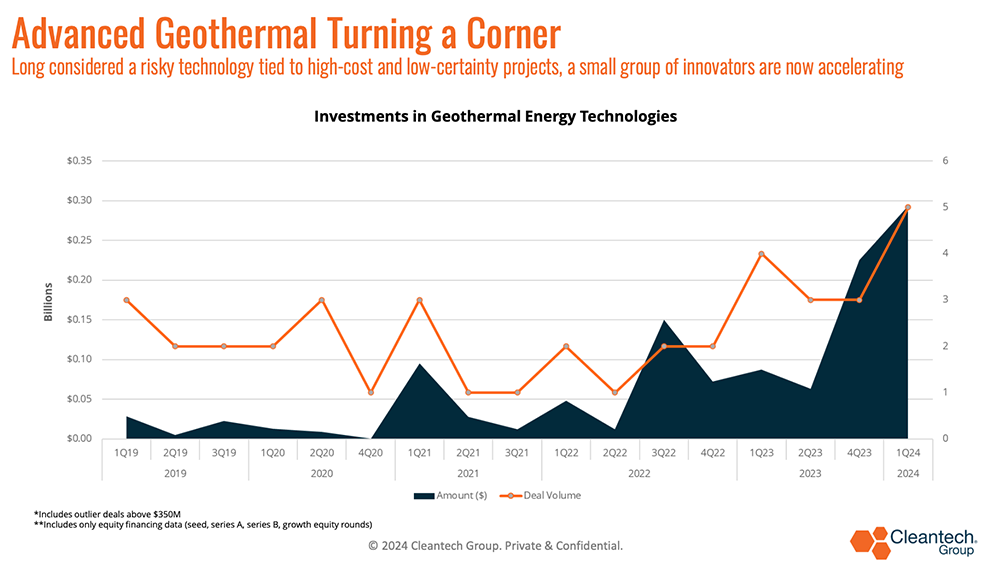

- A space to watch is enhanced geothermal – despite having significant potential to provide 24/7 firm clean power, challenging project economics have remained a barrier. New technologies in drilling and closed-loop systems have shown promise to better access the latent power potential in hot, dry rock geothermal deposits.

- This past quarter was the most significant in geothermal venture financing since we began tracking the space, some key deals included:

- Quaise: $21M Series A for supply chain development, field operations to advance deep geothermal drilling

- Fervo: $244M to further operations at Cape Station to support clean electricity to the grid by 2026. Fervo has multiple power purchase agreements, including with Google and East Bay Community Energy

- Sage Geosystems: $17M Series A to support 3MW site in Texas after successfully completing full-scale commercial pilot that produced 200kw for more than 18 hours and 1 MW for 30 minutes

How Can Climate Innovation Continue to Evolve?

How Can Climate Innovation Continue to Evolve?

- It’s all about attacking the cost curve: so many of the innovative technologies that we’ve followed for years are now entering real projects and manufacturing. Once market forces kick in and demand pull is observed, you’ll have more entrants and begin the economic journey to commoditization – getting past green premiums and toward affordability will be critical for batteries, hydrogen production, and low-carbon industrial products (steel, cement, chemicals).

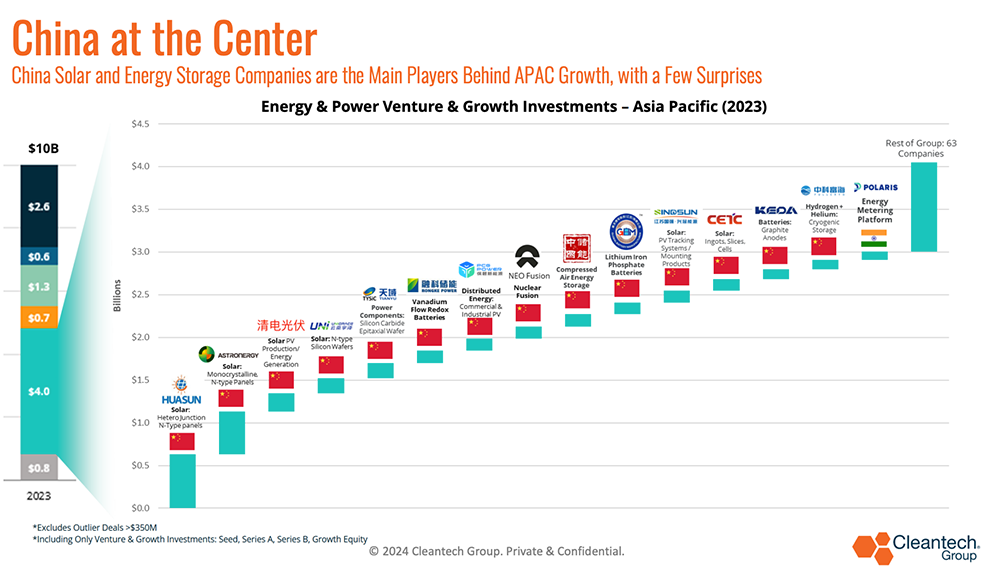

- There’s a habit of referring to China in this regard as a siloed case for specific technologies – but ultimately China is a proxy for the cost pressures that innovators need to keep up with once scale manufacturing is online (a change from the R&D phase when tech performance metrics tend to be more central concerns).

- See the graphic below, where China was the central innovation & venture financing for energy in APAC in 2025 – if this is any indication, one can expect to see similar levels of competition outside of just solar and batteries, but in all aspects of energy technologies.

Some deals this past quarter that support energy technologies entering commercial phases include:

- Antora Energy raises $150M for thermal energy storage to support commercialization and a manufacturing facility in San Jose, California

- NineDot Energy raises $225M from Carlyle Group and Manulife Investment

- Ascend Elements raised a fresh $162M Growth Equity round to finalize North America’s first recycled cathode from black mass production facility

- Lohum raised a $54M Series B to expand their operations in EV battery-to-energy storage systems conversion while entering the recycled cathode materials market

Chinese Influence on the Future of the EV Market

The subsidies to Chinese EV manufacturers, as well-documented in recent reports, is very significant and has allowed for a rapid scaling of EV production and sales (both within China and Chinese-produced vehicles for export).

There is already a high 27.5% import tariff on Chinese-built vehicles in the U.S., so the onus will now be on U.S. manufacturers to slash costs through learning effects and use of technology.

- A critical challenge will be that Chinese manufacturers are already producing at significant scale (near 10M EVs sold by Chinese manufacturers last year vs. 1.2M in the U.S.). Subsidies or not, the learning effects from mass production are not to be understated – this is where manufacturers resolve production inefficiencies (e.g., reduce scrap), optimize factory layouts and operations management systems, gain negotiating power with suppliers, and generally achieve economies of scale (i.e., spreading CAPEX of facilities across more revenue).

- Passenger EVs tend to be the focus of this conversation, but buses and fleet vehicles are a frontier market that will also be critical – the learning effects gained by Chinese scale manufacturing may already be paying dividends in these markets (Automotive World, Proterra May Not be a Bellwether for e-bus Failure in the U.S.).

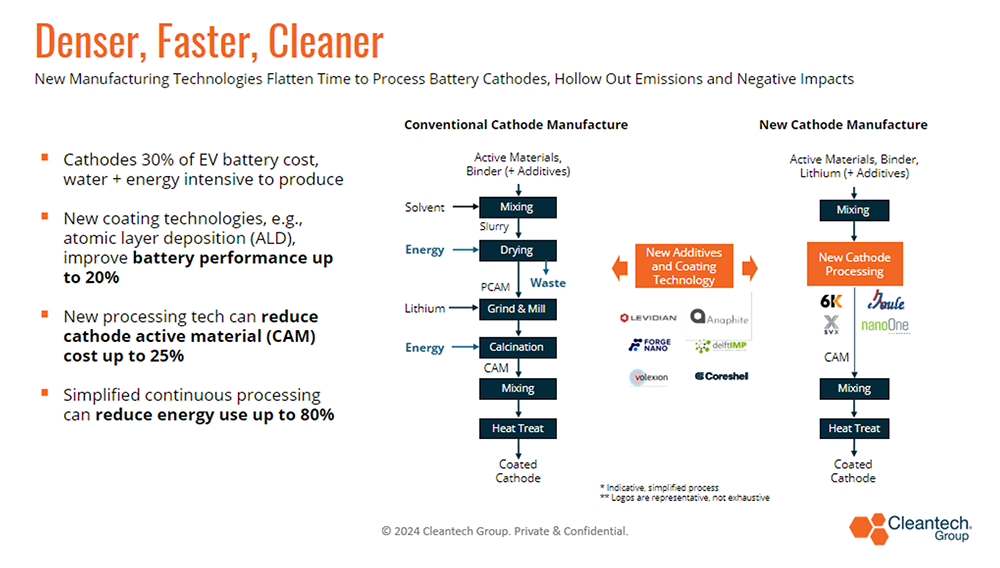

- Leveraging new technology is one of the best ways U.S. and Western EV producers can start reducing costs to compete better globally. There are many variables to consider in cost reduction, but our hypothesis at Cleantech Group is that innovation will reduce costs of cathodes in batteries – batteries can comprise up to 40% of vehicle cost and cathodes 30% of that battery cost. Some innovations that we’re keeping an eye on below:

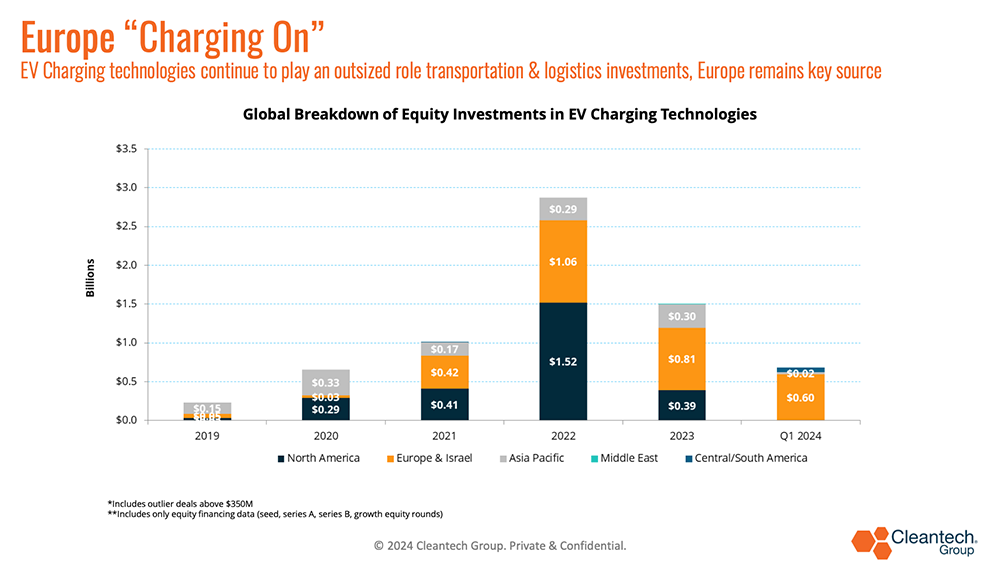

Europe Remains Key Source

An interesting pull-through effect of global EV rollout has been the opportunities it is creating for innovation and growth of new technologies in EV charging – Europe has seen consistent venture activity in this regard over the past few years (see chart below).

Some dynamics making the situation in Europe unique:

- Policy signals at the EU level:

2035 ICE ban for new cars approved in 2023

Deal on decarbonization of heavy-duty vehicles agreed in February, with ambitious targets o Deal on charging infrastructure in 2023 (AFIR)

Deals on the Batteries Regulation and Critical Raw Materials Act – the EU’s legislative framework around EVs was essentially completed over the last 18 months and covers the whole value chain

- The EU has much lower tariffs on Chinese EVs than the U.S. does, at a time when China has major overcapacity. Hence, competitively priced Chinese EVs are flooding into Europe and putting downward pressure on the prices of non-Chinese EVs

- Europe has had one single charging standard for a while, unlike the U.S. where there were multiple until Tesla’s recently won out