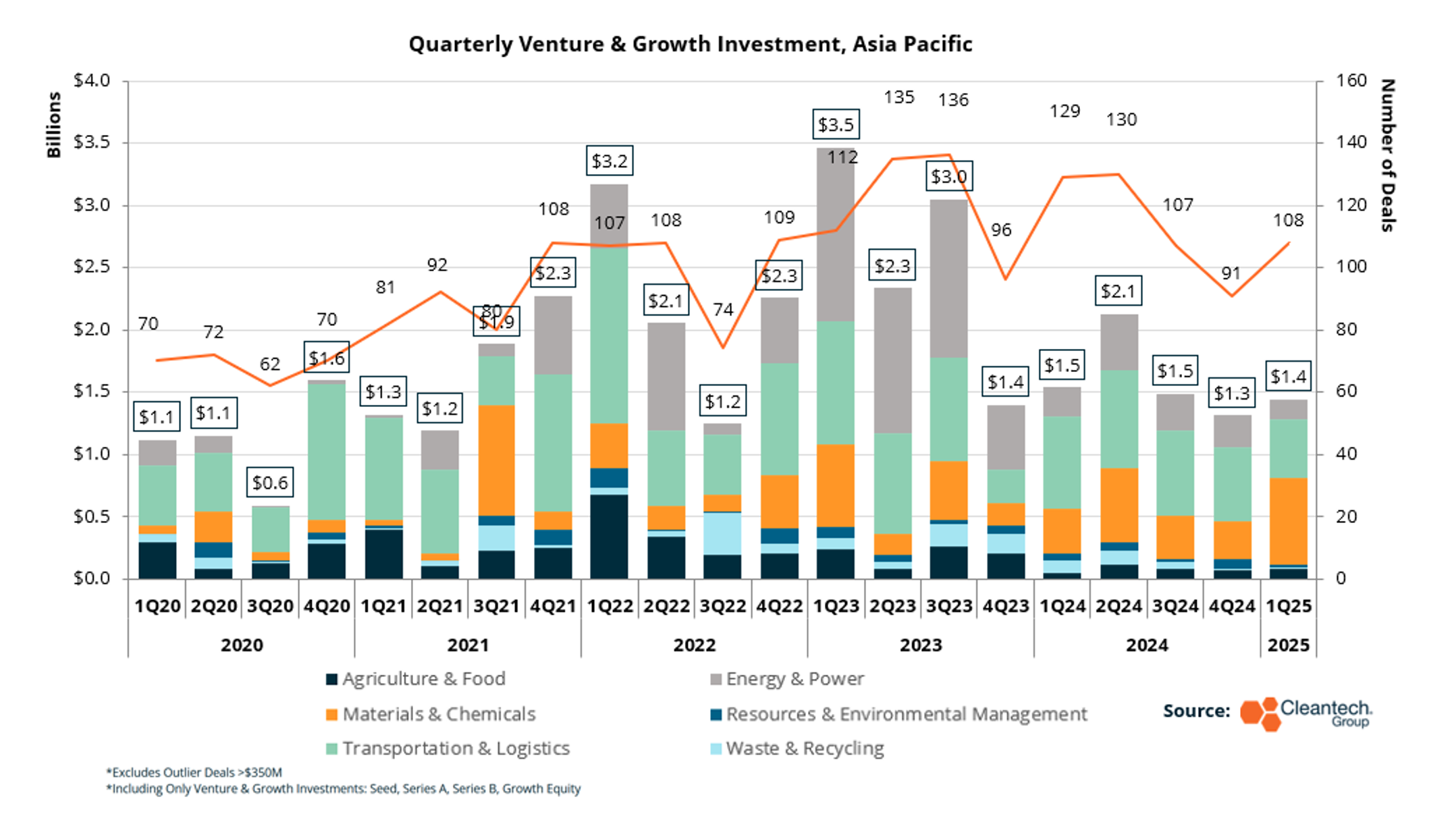

Under the Surface: APAC’s Strategic Shift in Cleantech Investment

Just a few months ago, we wrote in our year-end wrap-up newsletter on APAC activity that, while investment numbers had come down to earth following a highly active 2023, what was happening beneath the surface was a growth of the infrastructure necessary to facilitate the next waves of cleantech deployment (high-scale electric mobility, data centers), and also a competition to own innovation of the constituent components in the new cleantech economy (chips, semiconductors).

These trends have generally persisted through this first quarter of 2025, and indeed some have accelerated. Take note especially of the Materials & Chemicals industry group, which experienced its most significant APAC quarter since 2021.

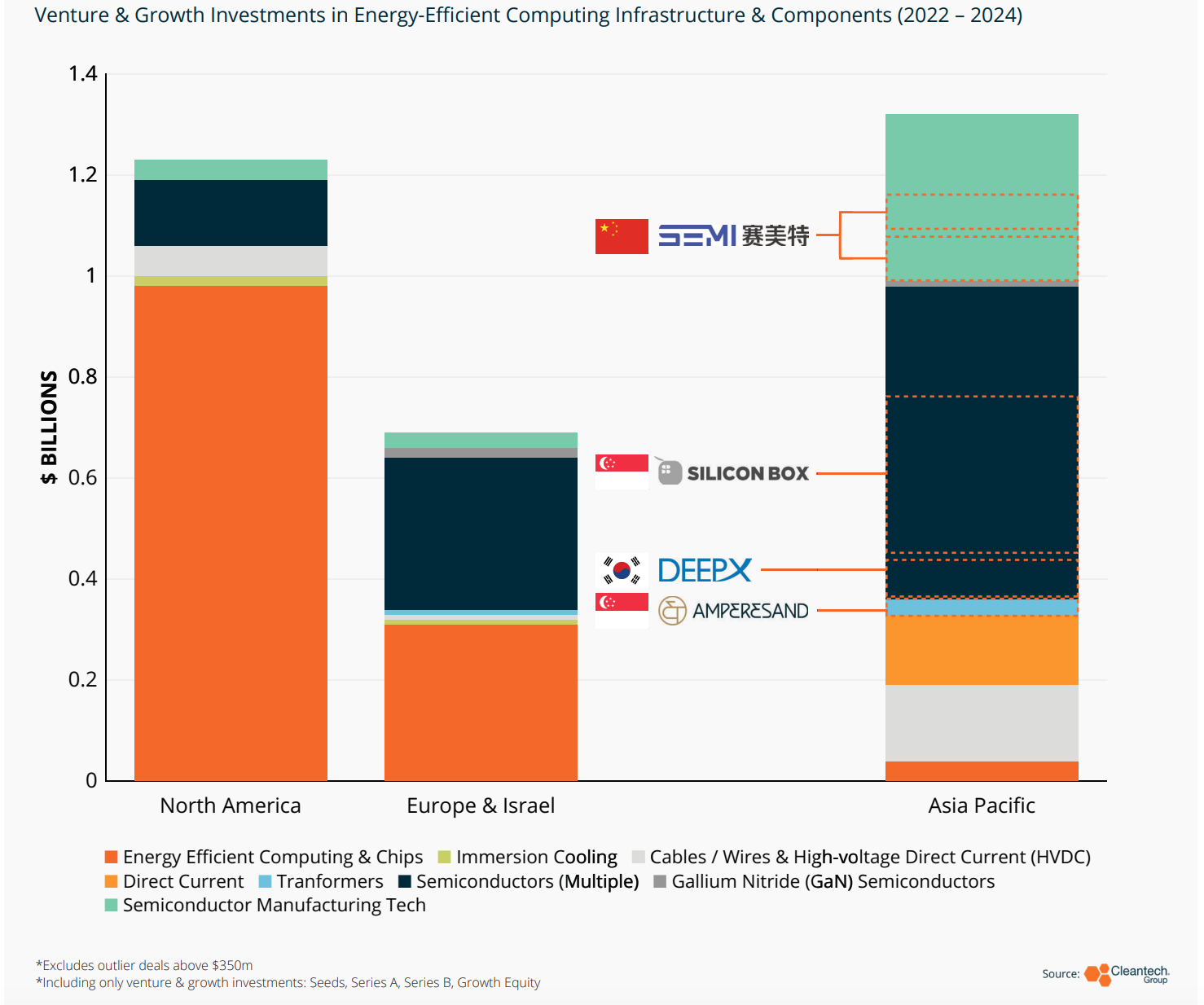

We observed in our 2025 APAC Cleantech 25 report (free download here) that Asia-Pacific was still catching up in delivering AI products for cleantech-specific applications, but indeed was competing on a global scale to innovate in the technologies that underpin AI infrastructure. Not only was innovation in APAC garnering more investment than global competitors, on aggregate, we also noted the presence of companies like Firmus Technologies and Amperesand on our APAC Cleantech 25 as an indication that the ecosystem was also perceiving these companies as high-quality and positioned for growth.

Much of the APAC innovation activity in the area has been at the furthest upstream level of semiconductor materials. Companies in the region, especially China, are seeking to reduce single points of failure in their supply chain that can be affected by trade restrictions – even before the most recent round of U.S. tariffs, we witnessed Chinese semiconductor innovators raising the right funds to tackle the upcoming opportunity.

This has an observable effect on the global context – not only were semiconductors the key underpinning technology segment in the Materials and Chemicals category in Q1, this space was once again primarily comprised of APAC-based innovators.

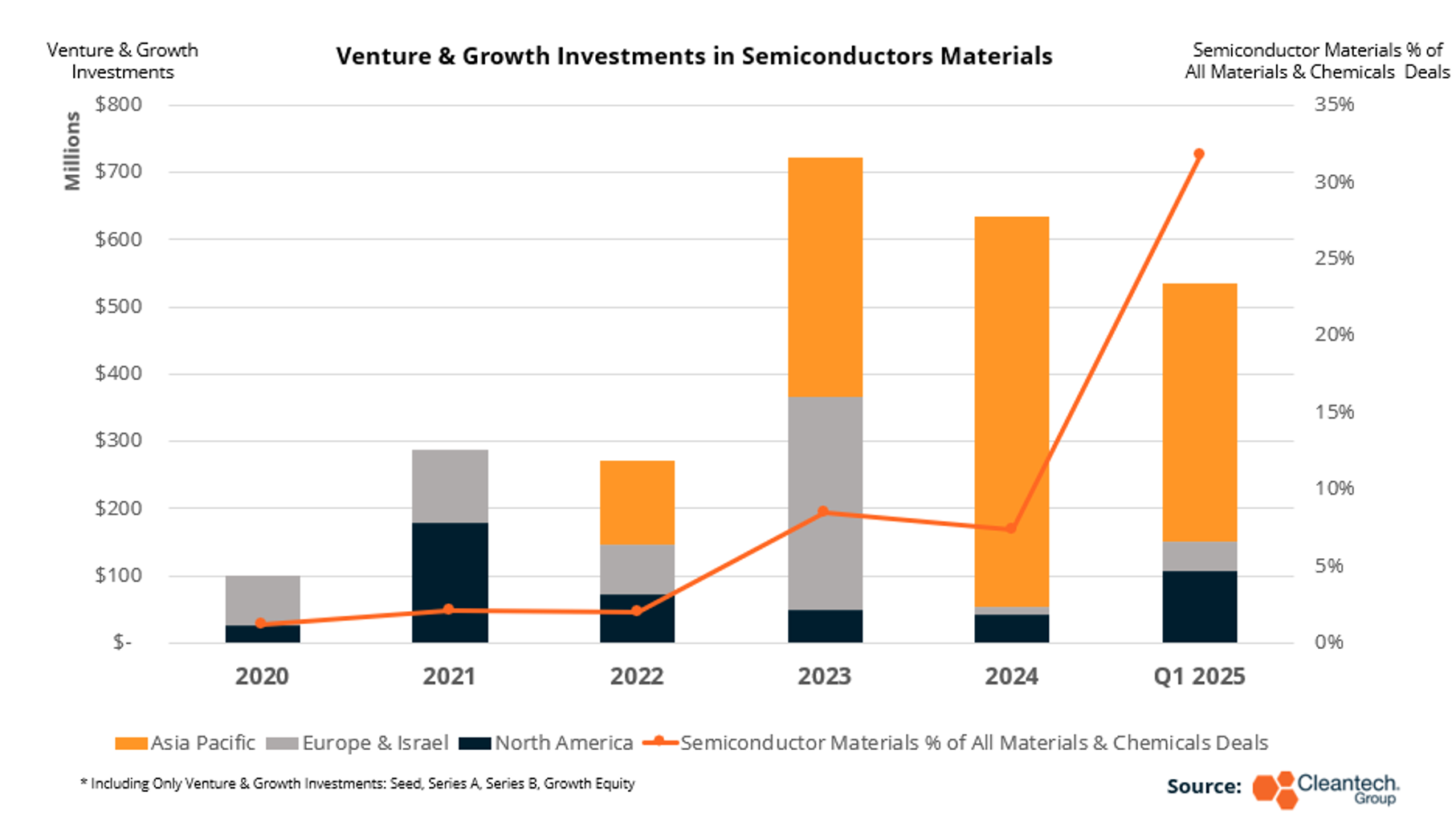

This past quarter was one of significant activity for Chinese innovators focused on both materials and manufacturing technology for semiconductors. A few notable examples:

- InventChip, a silicon carbide device manufacturer raised a $137.5M Growth Equity round in January. InventChip’s silicon carbide products are used in inverters for solar and wind and in electric vehicles (DC-DC conversion, charging). Previous funding rounds have taken in investment from major Chinese automotive OEMs and suppliers, including XPeng, Xiaomi, and CATL.

_ - Omnisun, a supplier of substrate materials for photomasks, raised a $101.7M Series B round, just less than a year off a $77M Series A last January. Omnisun, a 20-year-old company, claims to be the only Chinese company developing and selling these materials, which are a critical input to integrated circuits and printed circuit boards, as well as display technologies.

_ - A smaller round, but one potentially indicative of the direction of priority in Chinese semiconductors, is the $6.9M Growth Equity round in Teyan Semiconductor. Teyan produces equipment for semiconductor packaging (system-in-packaging, chiplets), printing, and laser processing services. Keep an eye out for a motivated drive to improve semiconductor packaging technology in China. As global players move beyond transistor scaling to packaging innovation in chips to pursue efficiency and power use reduction, this will be one of the key opportunities for Chinese semiconductor manufacturers to develop a performance and cost advantage at the same time that demand is growing, and trade is complicating.

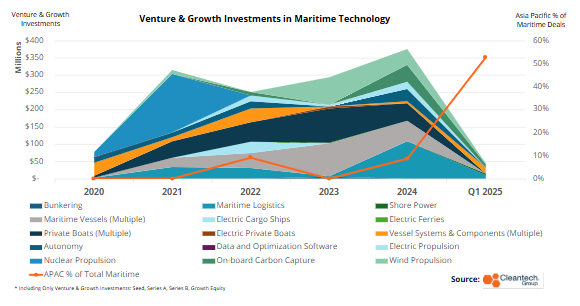

Q1 of 2025 brought an unexpected surprise in the form of high APAC investment activity in maritime cleantech. This, at a time when the maritime sectors in cleantech saw a landmark 2024 that involved only marginal APAC activity, raises a question of whether the trend is catching in Asia or whether the global trend is receding.

Part of the answer to that question is that Q1 was a slow quarter for global investment in maritime innovation (just 12% of what it was all of 2024). Even so, the $23M in investments in APAC-based maritime innovators in Q1 is compared to only $32M in the region in all of last year – and that $23M figure is for companies squarely categorized as maritime innovation (see the example of Power-X below who has multiple applications).

- Lyen Marine (China) offers pitch-controllable propellors for ships as well as a suite of analytics tools for fleet optimization, stating fuel savings potential from use of their propellor and analytics tools. The company raised a $13.6M Series A in February.

_ - The accelerating importance of the digital layer in maritime cleantech is coming through clearly in both the Lyen deal and also with Korean Seadronix. Seadronix describes itself as a “port-to-port” AI platform. Its software is able to bring a diverse feed of data from multiple sensor types into analytics and optimization tools for ships, for ports, and one that can be combined for both. Seadronix raised a $10.4M Series B round in March.

_ - Not reflected in the maritime numbers are a $38M round to Power-X. Power-X manufactures liquid-cooled lithium iron phosphate (LFP) batteries for stationary grid and commercial building storage, but also offers marine batteries. Power-X is now pioneering an innovative “Ocean Grid” offering comprised of battery-carrying ships that can charge with off-peak renewables and discharge at points of high demand. The rendering below is of the 240MWh “Power Ark” ship, set to sail in 2027 – one of the stated use cases will be “connecting” an offshore wind installation with the city of Yokohama.

Rendering of a Power-X “Power Ark”

In recent years, Asia-Pacific has been the central venue for both scale deployment and innovation EV charging methods. In the first quarter of 2025, investments in EV charging dipped globally, but also saw the APAC percentage of those deals dip as well. The open question will now be whether the leaders in EV charging (think Nio or BYD) are too well-established for new players to continue finding supply gaps (note that last quarter we identified a few niche gaps that innovators in APAC were experimenting with).

Nevertheless, the trend of innovation localized models for EV charging to accommodate nuances in usage patterns continued to develop. It is also clear from this past quarter’s deal activity that managing strain on grids is a growing priority for each geography that continues to grow EV ownership. In this past quarter’s deals, we can see three distinct technologies in three different countries as examples:

- Jolt (Australia) offers EV charging payment and membership solutions for both individual EV drivers but also fleets and ride sharing. Jolt secured $135M in structured debt from the Canada Infrastructure Bank in February to finance expansion into Canada.

_ - On the earlier-stage side of deals, India-based DeCharge raised a $2.5M Seed round to fund the growth of its 7kw charging unit and decentralized charging software. The DeCharge helps owners of buildings and parking spaces offer charging solutions at an affordable price.

_ - Kwetta (New Zealand) is a 2025 APAC Cleantech 25 awardee. The company’s “Grid Unlock” solution deploys DC fast-charging depots with sophisticated power electronics to avoid costly grid upgrades. Kwetta raised a $10.5M Series A in January.

A Kwetta Charging Depot