A Rapidly Evolving Landscape

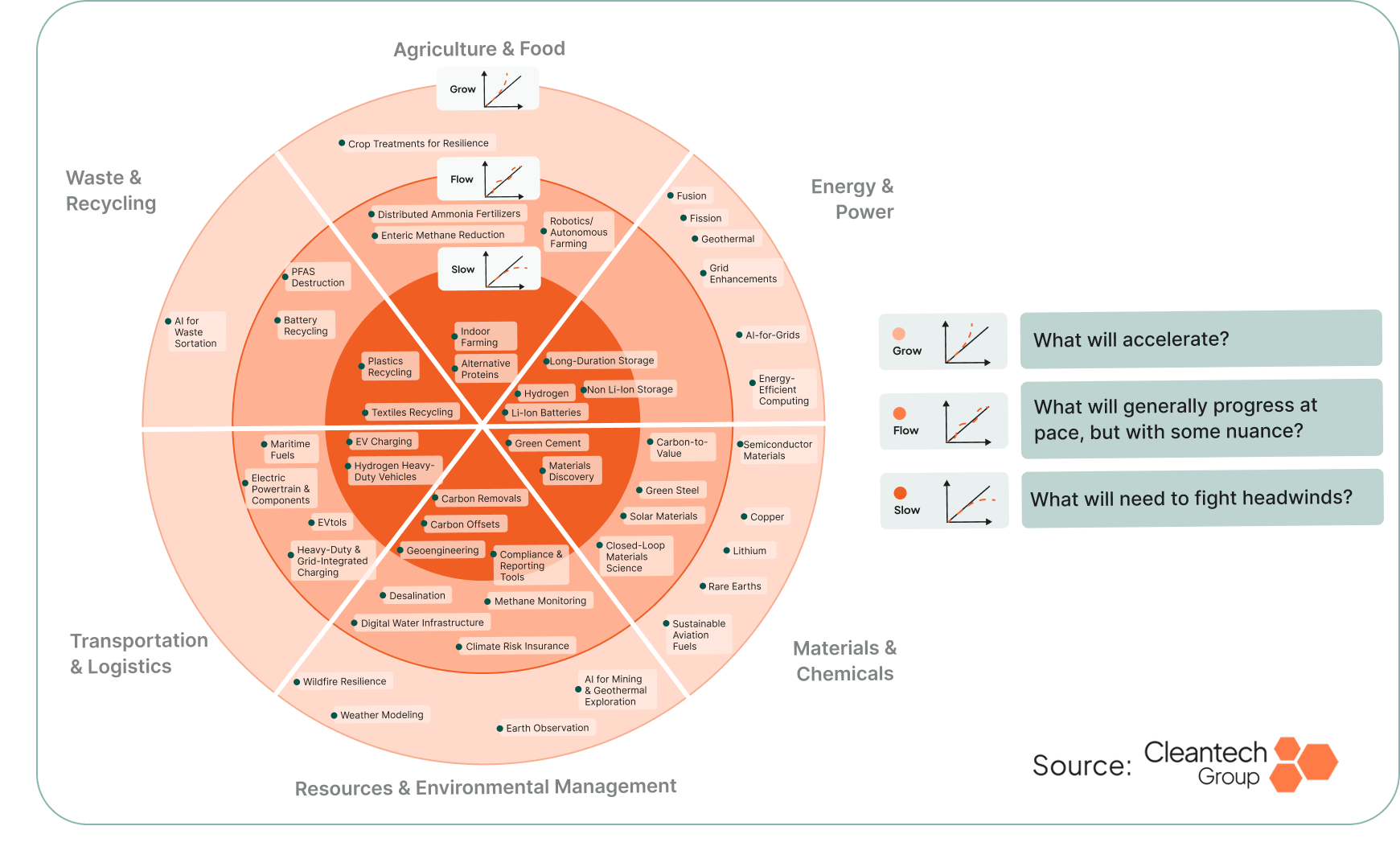

Coming off a 2025 replete with both “known unknowns” and “unknown unknowns” in the policy and global macroeconomic environment, we expect 2026 to proceed with slightly more certainty, but also more pressure on the global cleantech ecosystem. Given that the majority of technologies in the “Grow” ring are associated with AI infrastructure or critical minerals, there is a clear narrowing of growth areas into these two themes, while most else will stay in “Flow” or recede into “Slow”. What we expect for 2026 is a “pressure cooking” effect, in which the spaces experiencing continued growth today will become extra competitive, while the “Flow” and “Slow” rings will become especially challenging to break out of.

What Do We Predict to Grow, Flow, and Slow in 2026?

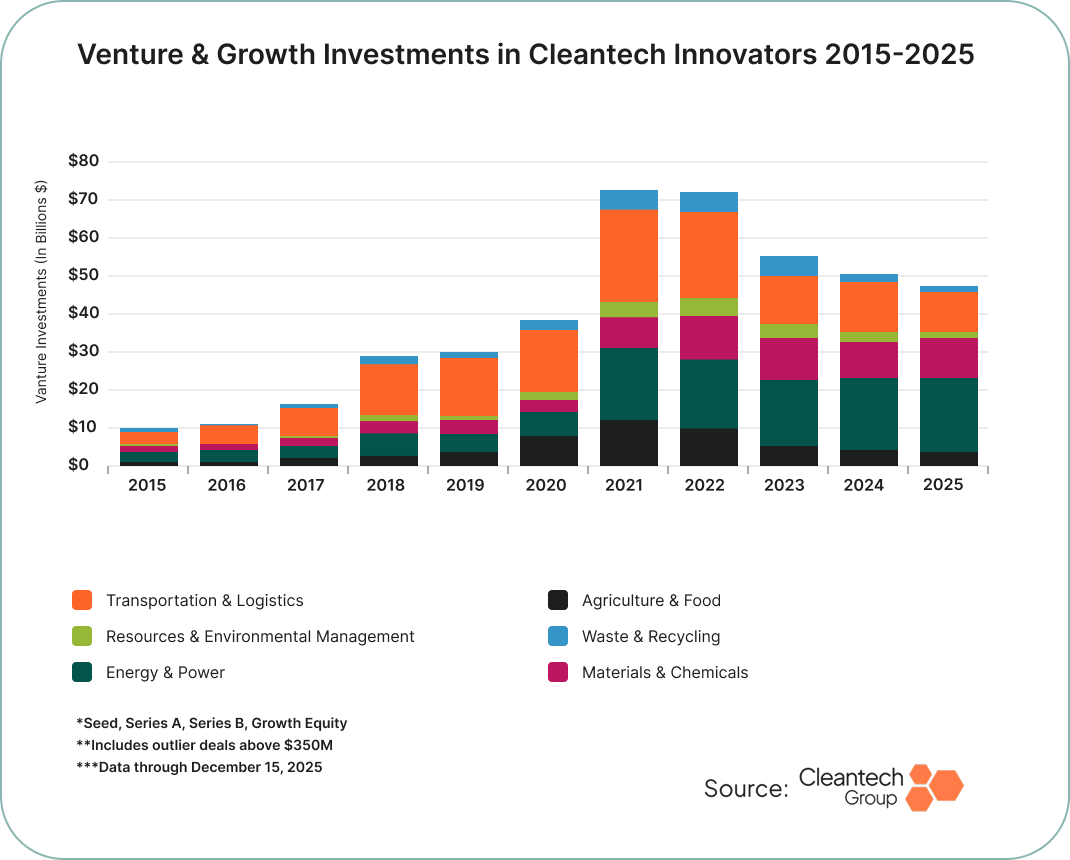

With today’s headwinds in mind, it is still worth taking a step back to understand exactly where we are in cleantech history. When using venture investments as a proxy for confidence in growth, there is a tendency to index against the low-interest rate environment of 2021 and 2022, which points to an apparent drop-off in the years that follow. However, if zooming out over the past decade, it can be seen that the space is far more robust than 10 years ago, and investments today still outpace those of the years just before the pandemic.

The Pursuit of Economic Durability

The next era of cleantech innovation will build “durability” into the global economy. We have seen for years that cleantech innovators have multiple arguments—decarbonization, supply chain stability, and health & safety improvement—for the adoption of their technologies. For this reason, we expect the primary drivers for cleantech adoption to shift toward those that demand economic durability. We see this developing through two overlapping lenses: continuity and predictability.

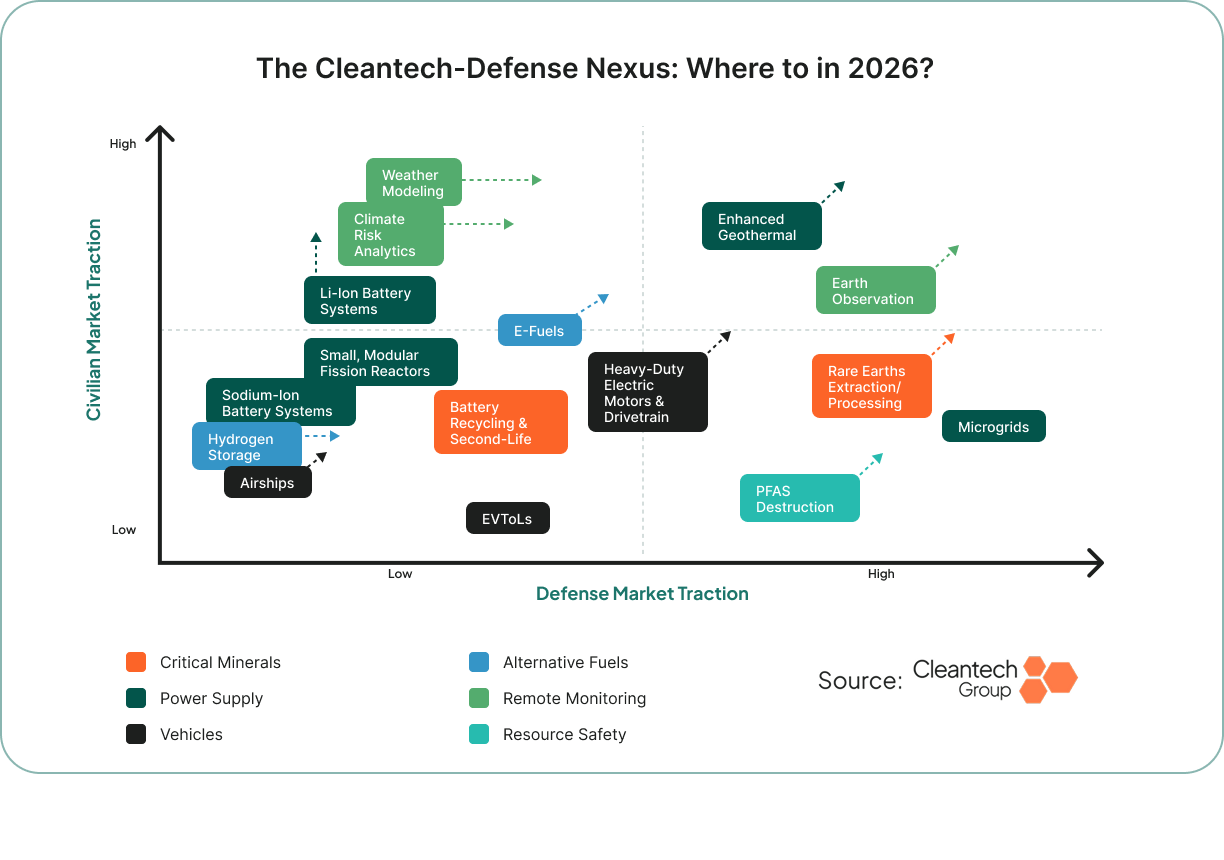

- Continuity: A vital nexus has emerged between cleantech and defense, where technologies offer operational and supply continuity for both national security actors and civilian applications.

- Predictability: The urgent race to secure power for AI growth is motivating the adoption of novel baseload power, grid efficiency, and resilience technologies to mitigate supply uncertainty.

The latter part of this Trend Watch outlines the slow-growing but emerging urgency around predictability of water supply that is starting to show up in more parts of the economy. The still under-engaged spectrum of adaptation & resilience technologies is expected to grow as the predictability of public safety and economic activities face compound threats from climate change each year.

The Cleantech–National Security Nexus is Crystallizing

We have seen a clear change in the vernacular of cleantech companies over the past year, with the word “security” as the leading line in more companies’ headline selling points than ever. There are multiple flavors to the security argument in cleantech, namely, resource security (think critical minerals, energy, water) but also several areas where there is a direct overlap with national security and defense.

With continued concerns over supply chain domination by China, technologies that offer superior material performance while eliminating supply chain risk will continue to be of paramount strategic value in 2026.

- Niron Magnetics: Manufactures high-performance, rare earth-free permanent magnets using proprietary iron nitride technology, which provides efficiency and thermal stability while bypassing critical supply chain constraints.

- Phoenix Tailings: A zero-waste, closed-loop system for extraction and pure metal refining of rare earth elements (REEs) from mine tailings.

- Boston Metal: Uses a molten salt electrolysis process to recover rare metals such as niobium and tantalum from waste streams.

These companies represent complementary strategic hedges: Niron removes the need for scarce materials, while Phoenix Tailings and Boston Metal ensure that existing waste streams can be utilized to rebuild a vertically integrated, domestically controlled critical minerals supply chain. In July 2025, the U.S. Department of War made a landmark agreement with MP Materials that included $400M of stock purchases and a 10-year agreement to purchase neodymium-praseodymium (NdPr). The Department of War subsequently provided a $620M loan to Vulcan Elements as part of a larger partnership to produce magnets within the U.S..

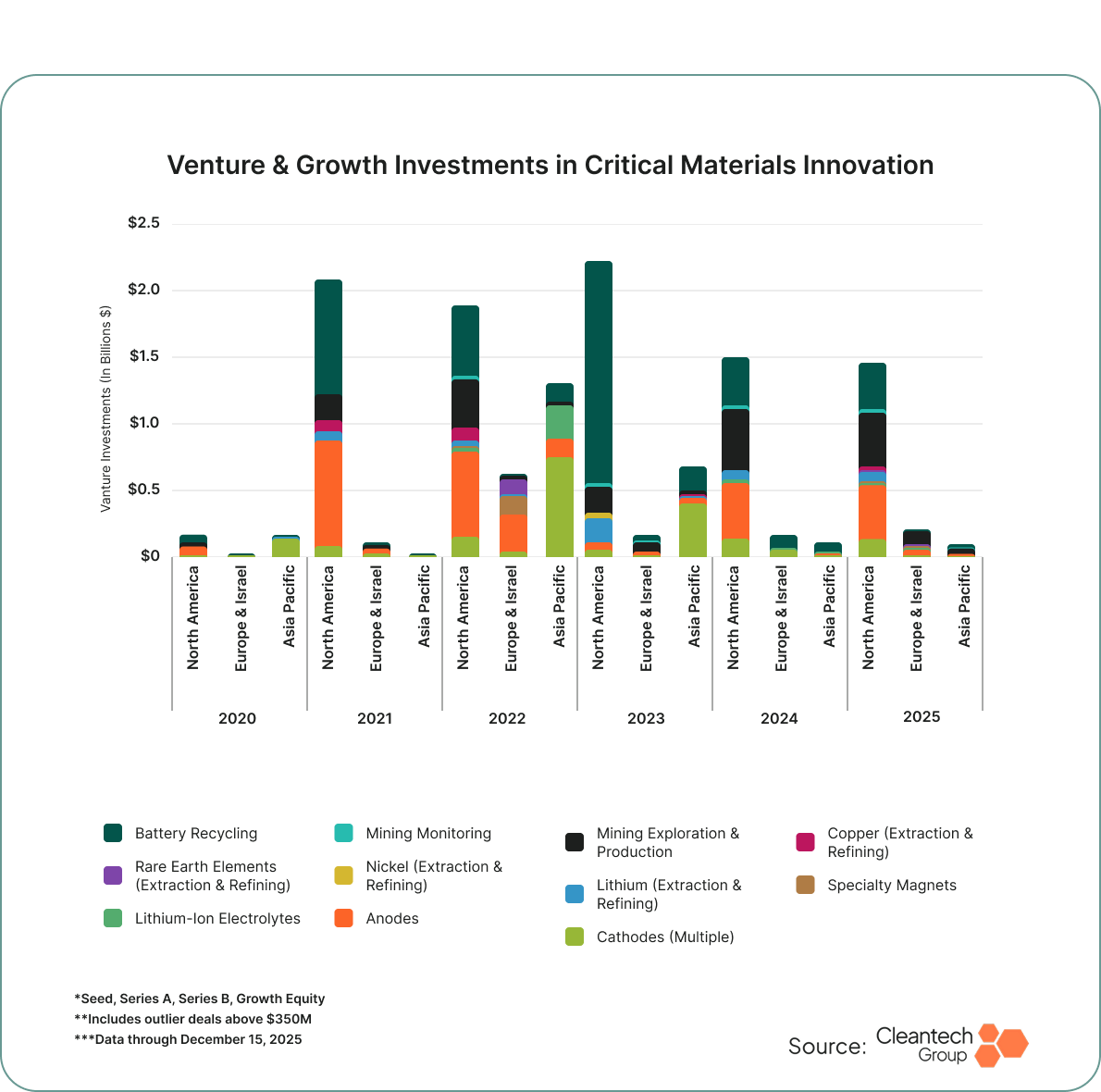

Breaking the Critical Minerals Bottleneck

The current geopolitical environment has made reliance on single sources of refined materials untenable. We expect that technologies offering decentralized processing and recovery of materials in circulation will continue to see enthusiasm. However, price premiums are still the norm in on-shored and friend-shored minerals. Achieving enough iterations to drive down cost and supply critical minerals at industrial scale is the challenge that many of this year’s Global Cleantech 100 are taking aim at.

The high capital expenditures and long timelines of traditional centralized refineries are a liability in a market demanding speed to deployment. Demands for lithium supply require refining solutions to be modular, electrified, and highly resource-efficient.

- ElectraLith: Refines lithium chloride (LiCL) to battery-ready lithium hydroxide (LiOH) in one processing stream.

- Mangrove Lithium: Uses oxygen cathodes to produce LiOH without harsh chemicals at a cost competitive with Chinese refiners.

The renewed urgency to claim critical minerals is providing a tailwind to recycling approaches, which represent the nearest-term path to on-shored materials. This year’s Global Cleantech 100 demonstrates a maturing landscape:

- Nth Cycle: Employs electro-extraction technology to refine critical metals directly on-site from end-of-life batteries or mined ore.

- Cyclic Materials: Building a hub-and-spoke model to recover REEs from e-scrap with 98% less water use than virgin mining.

- cylib: A Europe-focused recovery of lithium, graphite, nickel, cobalt, and manganese from spent EV batteries.

- SiTration: Uses a high-durability silicon membrane to separate materials with electrical processes.

While not a materials recycling approach, Moment Energy has capitalized on the data center boom to accelerate deployment of repurposed electric vehicle batteries into stationary energy storage units. Further proof that there is demand for on-shore batteries and materials, and multiple ways for recyclers to turn recovered batteries into value.

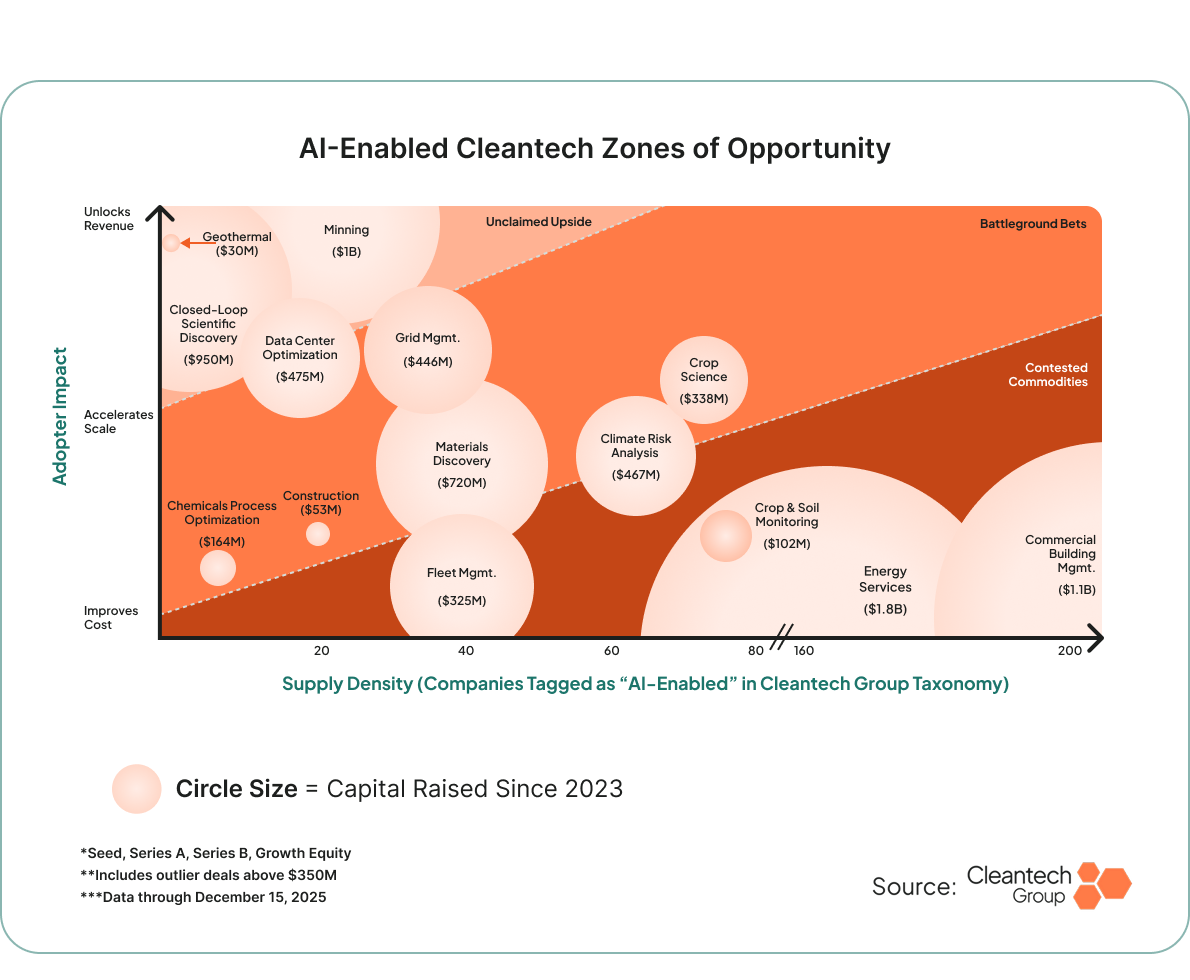

AI in Cleantech: More a Crashing Wave Than a Bubble

While much of the tech community is wrestling with the prospect of an AI bubble, adoption in industry-specific applications is still largely for basic purposes. Our position is that many AI companies in cleantech currently offer simple process optimization or LLM wrappers that are unlikely to fare well as adopters become more adept at leveraging their own proprietary data.

What will continue to grow are AI tools that bring unique data sets and data acquisition approaches into the mix.

- VerAI: Unlocks revenue by identifying concealed mineral deposits in under-explored terrain using custom data sets. While funding for AI in mining has increased, it remains an under-saturated space with only about 20 companies making defensible technology claims.

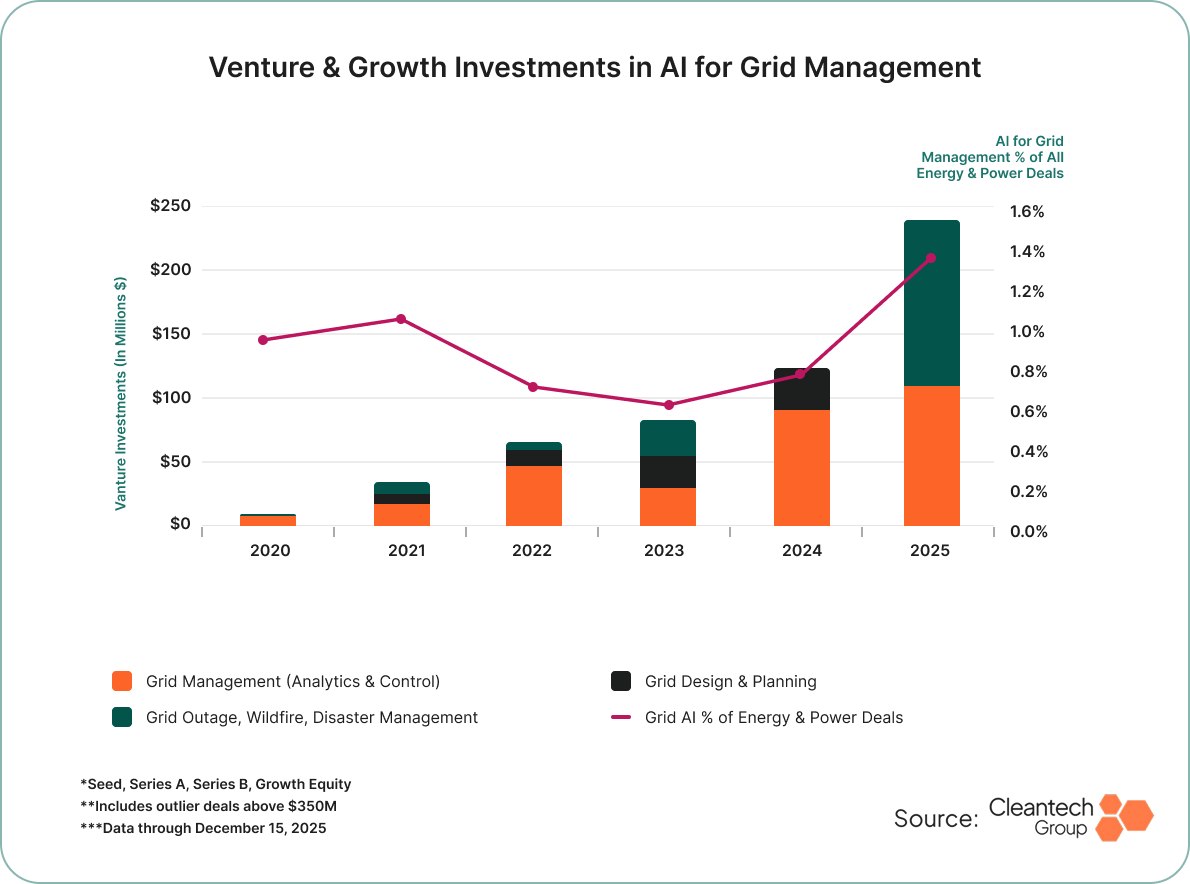

Grid Management: AI is simultaneously straining global power systems and providing the tools to relieve that strain. This has been a breakout year for grid management AI as power demand creates urgency to identify latent capacity.

- Argentina-founded innovator Splight leverages continuous data on grid activities to predict events and prescribe actions in real-time, versus only indexing actions against worst case scenarios.

- Jua is a high-precision weather forecasting AI that facilitates ultra-accurate energy trading recommendations, reducing grid balancing costs and improving capacity.

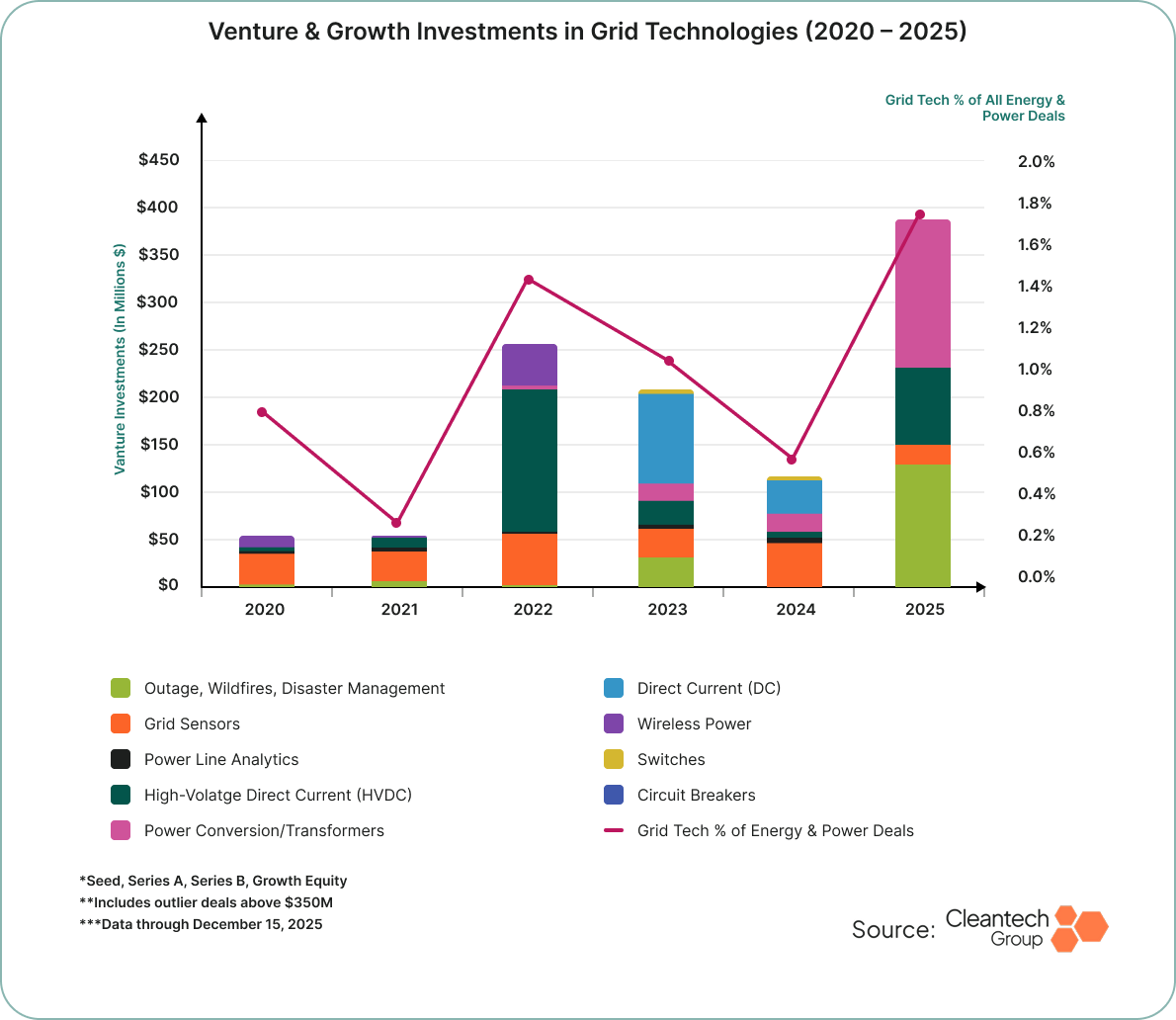

Grid Resilience: Avoiding the CapEx Trap

As utilities manage growing electricity demand, the dual imperatives of avoiding unnecessary CapEx buildout and ensuring continuity of services have taken hold. Continuity requires tracking the compounding climate threats that target grid infrastructure annually. Data centers and EV charging depots are presenting new commercial demand markets for these technologies.

Technologies for grid resilience experienced ahead-of-schedule growth in 2025, and the mix of Global Cleantech 100 award recipients testifies to the variety of solutions the market is seeing

- High-Efficiency Transformers: DG Matrix provides modular, programmable electrification for AI data centers and EV charging, while IONATE has reinvented magnetic systems in transformers with AI control modules.

- High-Capacity Transmission: Veir has developed a cryogenic cooling system for high-temperature superconductors to deliver 5–10 times conventional power capacity. TS Conductor can double or triple capacity on existing infrastructure.

- AssetCool: Uses robotics to apply temperature-reducing coatings to power lines to increase capacity.

As noted previously, AI has had a breakout year in grid management. These physical upgrades are complemented by intelligence from AiDash, which processes satellite data to predict and prioritize vegetation threats that cause outages, reducing liability costs from disaster events like wildfires.

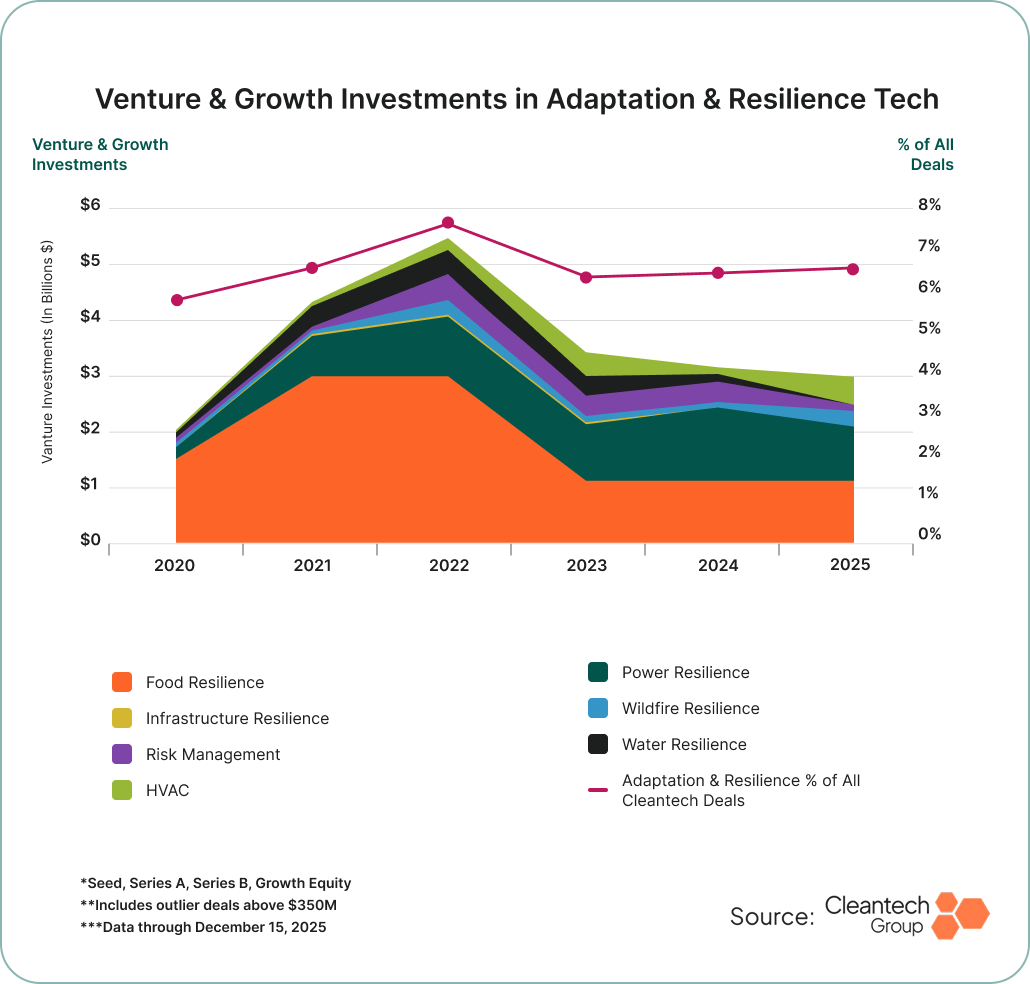

Adaptation and Resilience Presence in Global Cleantech 100: Slow but with Consistent Themes

Climate adaptation and resilience remains a consistently under-recognized theme. Multiplying weather events are still largely unaddressed, even with better technology coming into the market. However, certain pockets like wildfire resilience are maturing:

- Pano AI: Provides early wildfire detection via an AI-powered camera network.

- BurnBot: Uses robotic systems for prescribed burns to control risks before fires break out.

- Arbol: An insurance innovator offering extreme weather payouts in as little as two weeks.

Is Water Innovation Making its Way into the Mainstream

Like adaptation & resilience, water innovation has long been deemed risky by corporate adopters and cleantech investors. However, beneath the data, the 2026 Global Cleantech 100 gives us reason to believe that a new sense of urgency may be growing.

That urgency is logical, too. By 2050, 31% of global GDP will be exposed to high water stress. The motivation to ramp up water-intensive processes like semiconductor manufacturing and mineral extraction makes water stress an especially urgent problem.

- Aquafortus: Purifies high-salinity industrial brines with 90% less energy than conventional methods.

- Moleaer: Uses nanobubbles to reduce chemical/energy use in agriculture and wastewater treatment.

- ZwitterCo: Employs zwitterionic chemistry to prevent membrane fouling in wastewater reuse.

- Indra: Offers physio-electrical wastewater systems for infrastructure-deficient areas in India.

We expected resource efficiency to return to the spotlight as the macroeconomic environment tightened. While policy support for embodied carbon has fluctuated, solutions for reducing energy and water waste remain popular. This is evidenced by Wint (water flow monitoring) and Laiier (leak detection sensors). Building energy efficiency is also back in vogue with Aeroseal and Luxwall (vacuum-insulated glass).

As the geopolitical order shifts toward self-sufficiency, we expect the concepts of “durability” to endure. Cleantech innovators will continue to facilitate the continuity and predictability of economic systems. The boundary-pushers in the 2026 Global Cleantech 100 will be the same ones that bring cleaner approaches into the mainstream by winning the durability battle.

And while 2025 was a year marked by uncertainty, patterns have begun to emerge, and this cohort of 2026 Global Cleantech 100 winners gives us signal for where the second half of this decade will go.