Markets tend to discover things twice: once when the investors boom them, and again when a crisis makes them impossible to ignore. Sustainable aviation fuel (SAF) is having its second discovery. Reuters declared this week that the Iran crisis “makes green jet fuel interesting again“, a headline that tells you more about how markets pay attention than about the state of the sector. Most understand fossil fuel dependency runs through every mode of modern transport. Aviation feels it most acutely, with a fuel infrastructure built entirely around kerosene, little to no battery or fuel cell technologies at commercial scale, and limited ability to hedge against supply shocks of this magnitude.

But “interesting” or not, binding mandates are already law in the EU and UK, airlines have committed to over 52B liters of offtake and production facilities are operating with many more under construction and consideration. A dedicated community of investors, innovators, policymakers, and airlines has been working on this problem for decades and the data they leave behind makes for a different story than the one in the headlines.

The Investment Data Story

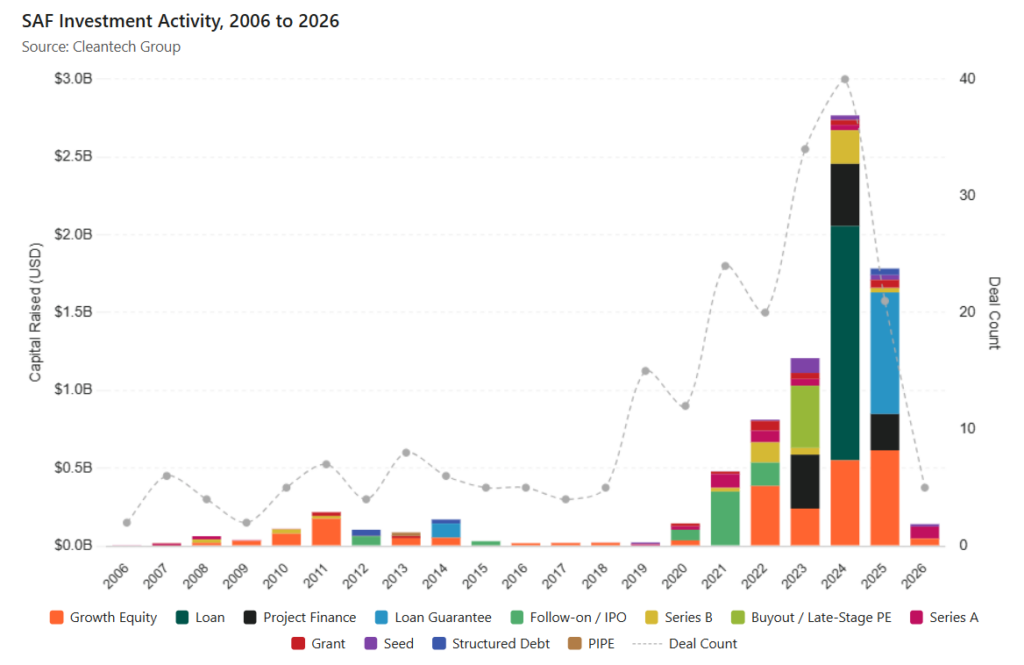

According to Cleantech Group data, investment activity across the SAF value chain, from direct producers to feedstock providers and enabling technology companies, the sector has attracted more than $8B in disclosed investment across more than 240 deals since 2006. The pace has been accelerating for years. Deal activity doubled between 2019 and 2021, and 2024 marked the most active year on record by both deal count and disclosed capital. Maturing technology, binding regulatory mandates and an expanding universe of strategic investors—airlines, oil majors, infrastructure funds and sovereign vehicles—were all making long-duration commitments to the sector.

Early activity was dominated by grants and Series A equity as pioneering companies like Gevo, LanzaTech (later spun off as LanzaJet) and SkyNRG worked to prove out the underlying technology. From 2019 onwards the types of investment shifted: growth equity rounds, project finance and structured debt began to appear at scale, the hallmark of a sector transitioning from laboratory to commercial infrastructure. Microsoft, Southwest Airlines, Airbus, Shell, Mitsui, and IAG were among those writing checks and penning offtake agreements.

The Start of the Shock

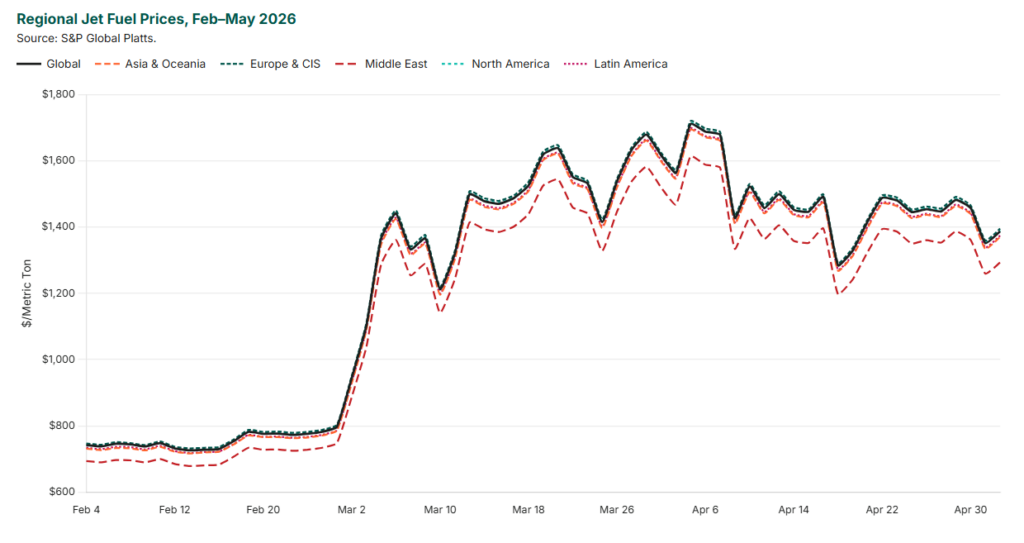

In late February 2026, U.S. and Israeli strikes on Iran set in motion the largest disruption to global oil supplies in recorded history. The closure of the Strait of Hormuz, through which approximately 25% of the world’s seaborne oil trade normally passes, delivered a supply shock that no hedging program, strategic reserve or diplomatic relation could fully absorb.

In Europe, where airlines import around a third of their jet fuel from the Middle East, prices have roughly doubled since the war began, with benchmark jet fuel spiking to a record $1,800 per metric ton in mid-March. Asia-Pacific has been hit hardest in structural terms: the region’s major jet fuel-producing nations are almost entirely dependent on Hormuz crude, leaving them simultaneously exposed as both importers and exporters when the strait closed. The U.S., the world’s largest oil producer and a net jet fuel exporter, has nonetheless seen prices rise around 70% from pre-war levels as global interconnection transmitted the shock westward. The Middle East may present the sharpest irony: domestic prices rose the least of any region, not because the region was spared, but because production that once flowed outward through the Strait was simply stranded at source.

Lufthansa has cut 20,000 flights from its schedule through the autumn, with KLM, and Scandinavian Airlines making their own reductions. The International Energy Agency (IEA) has warned that Europe may have only weeks of jet fuel supply remaining. Fuel is the second largest operating cost in aviation, and with no short-term substitute for fossil kerosene, the exposure is real. SAF is being rediscovered in boardrooms and procurement departments across the globe driven by risk management as much as any carbon commitment.

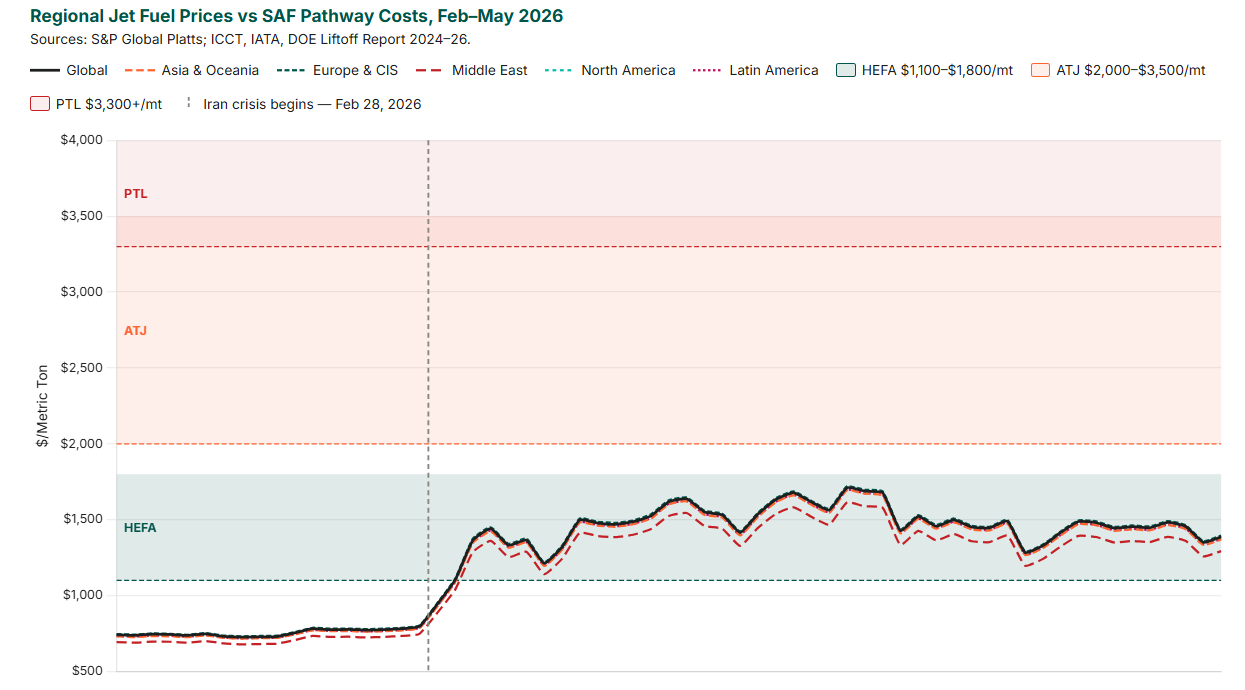

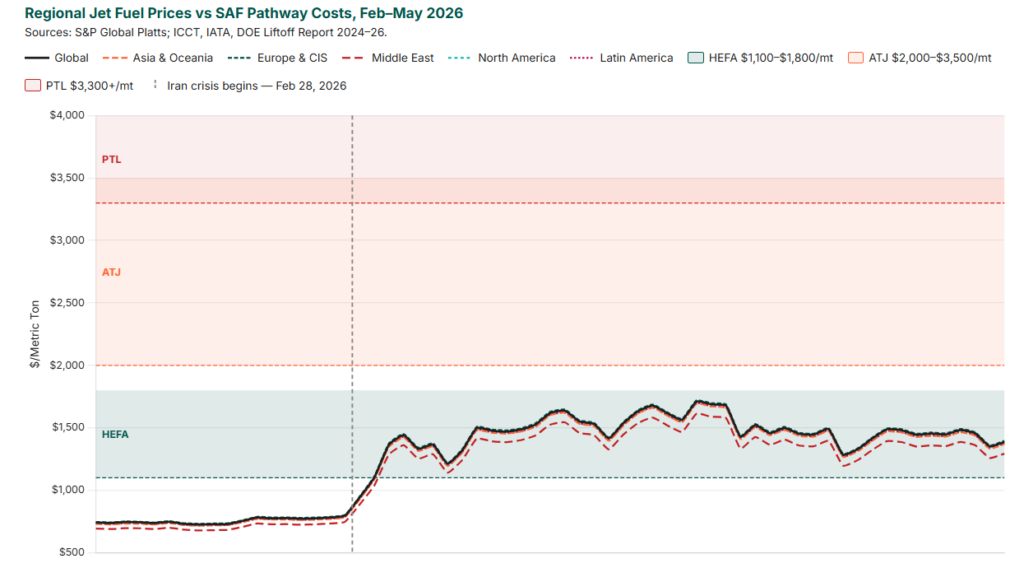

That rediscovery has a supply problem though. The SAF most immediately available—HEFA (hydroprocessed esters and fatty acids), made from used cooking oil and animal fats—cannot scale to meet a demand surge. According to IATA, around 80% of current SAF production relies on the HEFA pathway, yet total global SAF output in 2025 represents just 0.6% of jet fuel consumption. Its feedstocks are finite and already contested across road transport, and the SkyNRG/ICF SAF Market Outlook projects HEFA will hit a supply ceiling around 2030, when demand is expected to outpace what the pathway can physically deliver, at a point when mandated blending targets are still climbing steeply.

What Innovation Is Unlocking

If anything, the crisis has validated investment in three areas that together point toward a more durable supply base than HEFA alone can deliver.

The first is distributed manufacturing, and its strategic dimension goes beyond commercial logic. The move away from centralized mega-plants toward modular, containerized production units sited close to CO2 and energy sources is as much a strategic proposition as a commercial one. In Europe, INERATEC—whose ERA ONE plant in Frankfurt is Europe’s largest operational power-to-liquid facility at 2,500 metric tons of synthetic fuel per year—unveiled its Lifeline product range in March 2026 at a high-level event co-hosted with Rheinmetall, attended by representatives of the EU Commission, NATO, and senior defense leaders. The Lifeline units are containerized, rapidly deployable, and have been validated as fully compatible with existing military vehicles and aircraft by Germany’s Armed Forces Research Institute for Materials. Rheinmetall CEO Armin Papperger put the strategic case plainly: “War readiness requires a resilient energy infrastructure.” Separately, Brooklyn-based start-up AirCo announced in March 2026 that it had begun manufacturing containerized fuel production units for the Pentagon. AirCo’s mobile systems—each fitting within a standard shipping container and capable of producing hundreds to thousands of gallons of synthetic fuel per month—are designed to be transported to bases around the world, eliminating the need for fuel convoys that have historically been among the most dangerous logistical vulnerabilities in active combat zones.

The second is feedstock diversification, working to expand what counts as a viable SAF input without competing for the scarce lipid streams that constrain conventional HEFA. Houston-based Syzygy Plasmonics signed a binding six-year offtake agreement with Trafigura in January 2026 covering the entire production volume of NovaSAF-1, the world’s first fully electrified biogas-to-SAF facility. Located in Durazno, Uruguay, the plant sources biogas from the Estancias Del Lago dairy processing operation and draws on Uruguay’s renewable electricity grid to produce synthetic paraffinic kerosene with 90% lower lifecycle emissions than fossil jet fuel, with first deliveries targeted for 2028. The pathway has received ISCC pre-certification as both RFNBO-compliant and Advanced BioSAF positioning it to satisfy the most demanding regulatory requirements in the EU and UK. In Brazil, Cemvita and engineering partner Radix are advancing front-end engineering for a facility that uses Cemvita’s proprietary synthetic biology platform to convert crude glycerin—a low-value byproduct produced in large volumes alongside conventional biodiesel — into bio-oil suitable as HEFA feedstock. Adapting the process to Brazilian conditions delivered an estimated 40% reduction in cost per metric ton of bio-oil, and the approach is designed to be replicable across Brazil’s extensive network of biodiesel facilities, with a final investment decision (FID) targeted within 2026.

The third is integrated capture and fuel synthesis collapsing the traditionally sequential steps of carbon capture and fuel production into a single process, eliminating the energy losses and capital costs that accumulate at the interfaces between separate systems. Boston-based Sora Fuels closed a $14.6M seed round in April 2026, with a liquid biocarbonate electrolyzer that simultaneously absorbs CO2 from the atmosphere and converts it—using renewable electricity and water—directly into SAF. On the other side of the pond, Oxford-based OXCCU, backed by Aramco Ventures, International Airlines Group, and Safran Corporate Ventures, converts captured CO2 directly into hydrocarbons including SAF, chemicals, and biodegradable plastics via a proprietary catalytic process operating at lower temperatures than conventional Fischer-Tropsch synthesis. Neither is at commercial scale yet. But the direction they represent is the shape of a SAF industry that is not dependent on a finite global supply of any one feedstock.

The Regulatory Architecture Was Already in Place

Innovation was not the only thing moving along before the crisis erupted. Governments were already legislating SAF blending targets years before the first strike on Iran, with energy security alongside carbon reduction as the stated rationale.

ReFuelEU Aviation replaced fragmented national approaches with a single EU-wide regulation requiring aviation fuel suppliers to blend increasing shares of SAF at all EU airports—2% from 2025, rising to 6% by 2030, 20% by 2035, and 70% by 2050, with a separate sub-mandate for synthetic e-fuels beginning in 2030. The UK went further in the near term, mandating 10% by 2030—and crucially, both regimes were already in force before the crisis began.

The crisis has exposed something important about how the two regimes were designed. The EU’s non-compliance framework links penalties to the price gap between SAF and conventional jet fuel, recalibrated annually by the European Union Aviation Safety Agency. In a high oil price environment, that gap narrows and so does the deterrent. The penalty becomes softest precisely when supply pressure is highest. The UK took a structurally different approach, setting its buy-out in energy terms rather than against a commodity spread. That design doesn’t move with the oil market. Whether prices spike or collapse, the compliance cost stays fixed, a more durable floor for investment certainty.

It is the difference between a regulatory signal that holds under stress and one that bends with it. European policymakers conducting their scheduled 2027 review of ReFuelEU now have a live case study in why the design matters, and a clear model to examine.

The Economics of a Narrowing Gap

Perhaps the most shocking of all, buried in the price data is something the SAF sector has been waiting years to show a skeptical finance community. The crisis not only raised conventional jet fuel costs but compressed the premium that has defined one of SAF’s most commercial challenges.

Pre-crisis, conventional jet fuel traded at approximately $600 per metric ton. HEFA-based SAF, the most mature and cost-competitive pathway, cost in the range of $1,100–$1,800 per metric ton at market. Alcohol-to-jet pathways sat higher at $2,000–$3,500 per metric ton, and power-to-liquid (PtL) e-SAF, still at pioneer scale, ranged from $3,300–$5,200 per metric ton. The premium was real, substantial, and the primary reason that voluntary SAF adoption remained below 1% of global jet fuel consumption despite years of corporate sustainability commitments.

Today, with European and Asian spot jet fuel trading at approximately $1,400 per metric ton, the lower end of the HEFA range is effectively at parity with the conventional market. Airlines holding long-term SAF offtake agreements, signed at pre-crisis contracted prices of $1,300–$1,600 per metric ton with producers including Neste, World Energy and Gevo, now find those contracts pricing SAF at or near parity with current spot conventional jet fuel. United’s multi-year deal with Neste fixes a blended price near $1,400 per metric ton through 2027, while Delta’s Gevo contract locks at $1,300 per metric ton. Figures that looked expensive eighteen months ago look normal today.

An Uncomfortable Truth in Opportunity

February 2026 has delivered something that two decades of climate advocacy, carbon pricing, and sustainability reporting could not: a visceral, balance-sheet-level demonstration of what fossil fuel dependency actually costs and what SAF could unlock.

Optimism, though, has to be held honestly. Sustainable aviation fuel, as it exists today at commercial scale, is approximately 99% HEFA, finite and with an IEA warning that demand is already approaching the supply limits of the most-used wastes and residues. Scaling HEFA deals with one part of the problem while leaving the deeper one intact: aviation’s reliance on a fuel source whose long-term availability is constrained, delivering carbon savings that, while real, fall well short of what the word “sustainable” promises at the volumes the industry needs.

Power-to-liquid e-SAF, produced from green hydrogen and captured CO2, carries almost no feedstock constraint and promises lifecycle emissions reductions of 85% or more. It is also still years from commercial scale and hundreds of billions of dollars from the production volumes aviation requires due to large capital infrastructure sinks. The investment data captures the early stages of this journey. What it does not yet capture is arrival.

Regardless, SAF has never had a better argument. The investment infrastructure is maturing. The regulatory mandates are law. The offtake agreements are signed. For the first time, the financial and risk management case for fuel diversification stands on its own, without needing a carbon credit or a sustainability target to justify it and the industry knows it. Only time will tell if this new understanding will fade or not when the Strait of Hormuz fully reopens.

Dive into the APAC Cleantech 25

This annual selection identifies the region’s leading innovators poised for significant market disruption in the next five to ten years.