The crisis around the Strait of Hormuz has reached a new fever pitch today, with a looming deadline for a deal that many fear will not be met. Last week, Cleantech Group co-hosted a webinar with Teneo, featuring geopolitical expert Emily Stromquist and energy veteran Bret Kadison (recording here). The situation in Iran has, of course, evolved just in the past seven days, but the potential for a long-tail of effects on energy and adjacent markets has only intensified.

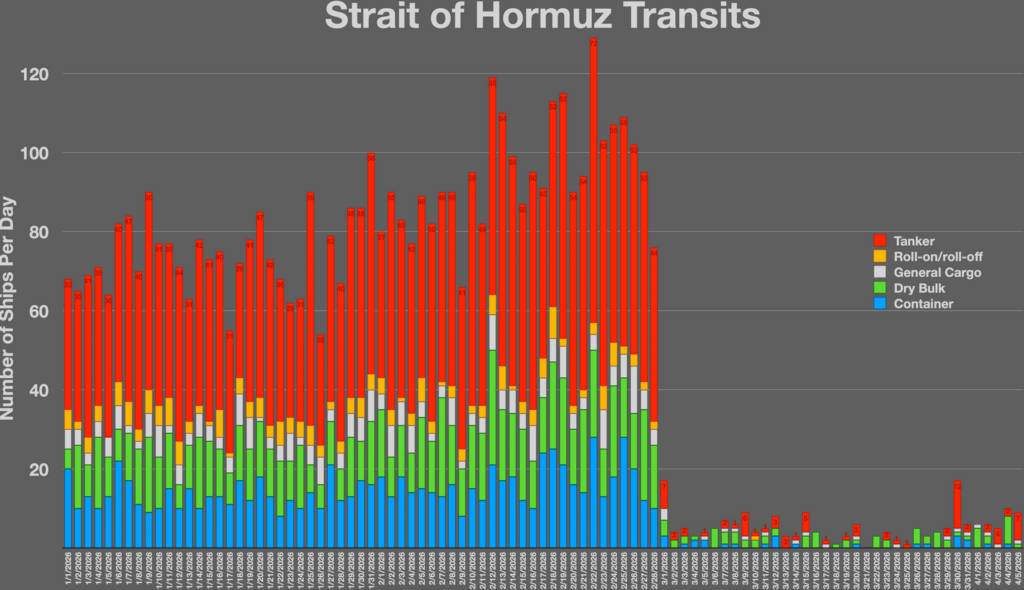

Source: International Monetary Fund Portwatch

The Conflict Is Not Heading Toward a Quick Resolution, and Markets Are Starting to Price That In

The Trump administration is caught between two objectives: reopening the Strait of Hormuz and finding a way to wind down operations. Iran, meanwhile, has little incentive to cooperate. A move on Kharg Island (through which 90% of Iran’s crude exports flow) raises the stakes further, with Iranian retaliation likely to target regional energy infrastructure and shipping options beyond Hormuz. The pattern identified in last week’s webinar was characterized as “escalate to de-escalate” (i.e., expect more activity before an off-ramp is achieved).

The Strategic Petroleum Reserve Is Less of a Buffer Than It Appears

The U.S. Strategic Petroleum Reserve was already at roughly 58% capacity before the crisis. The 172-million-barrel release has brought it down to around one-third full, a level uncomfortably close to the 25-30% floor required to avoid structural collapse. Strategic reserves also take time to distribute; they are not instantly accessible. Other countries don’t have that cushion at all, and governments are already resorting to consumption caps, and much of Asia has enacted purchase subsidies as stopgap measures. The political dimension matters too: the longer this runs, the harder it becomes for the administration to find a diplomatic solution, particularly heading into a midterm election where energy prices are a liability.

There Is Danger for Dual Disruption at Both Hormuz and Bab-el-Mandeb

Much of the market focus has been on the Strait of Hormuz, but simultaneous disruption at Bab-el-Mandeb in the Red Sea would compound the impact dramatically. There are very few alternatives available to patch over that kind of combined chokepoint. The knock-on effects would extend well beyond energy: global shipping, industrial inputs, and supply chains across multiple sectors simultaneously, with Asia particularly exposed given its heavy dependence on Gulf hydrocarbon imports.

LNG’s Role as a Bridge Fuel Is Now a Genuine Open Question

The strikes on Ras Laffan in Qatar took approximately 17% of the country’s LNG capacity offline at a moment when new supply is still roughly a year away. That has reopened a debate many thought was settled: does LNG still make sense as the default bridge fuel, or does this conflict accelerate the shift toward a more diversified energy mix? LNG also lacks the fungibility of oil, meaning that markets increasing their dependence on gas imports are actually reducing their own flexibility in the process. The question is live in a way it was not before.

A “Security Premium” Is Emerging as a Real Factor in Procurement and Investment Decisions

During last week’s webinar, an analogy was drawn to the internal carbon price that companies like Microsoft and BP use to stress-test long-term investments: a risk cost baked into decision-making not for ideological reasons, but as a financial and risk management discipline. Something similar is now taking shape around supply chain geography. Companies will start assigning genuine risk premiums to sourcing decisions that run through unstable corridors. The difference this time, compared to previous shocks like the 2010 rare earth disruption that briefly shut down Japanese production lines, is that the structural pressure feels more durable. The question is whether companies internalize this as a long-term recalibration or revert to cost optimization once things stabilize, as they have historically tended to do.

The Full Picture Is Members-Only

Members get the complete analysis. Unlock the full picture—the insights, data, and connections that will guide your next move.