2025 was a year marked by volatility across many industries, with a changed U.S. posture toward clean and renewable energy, an accelerated drive to de-couple the U.S. and Europe from Chinese minerals supply chains, all at a time when countries around the world race to AI supremacy. While it was reasonable to assume in 2025 that the cleantech theme would face a major drop-off in growth, that has manifested more as a subtle shift but with the underlying technology areas facing highly variable dynamics.

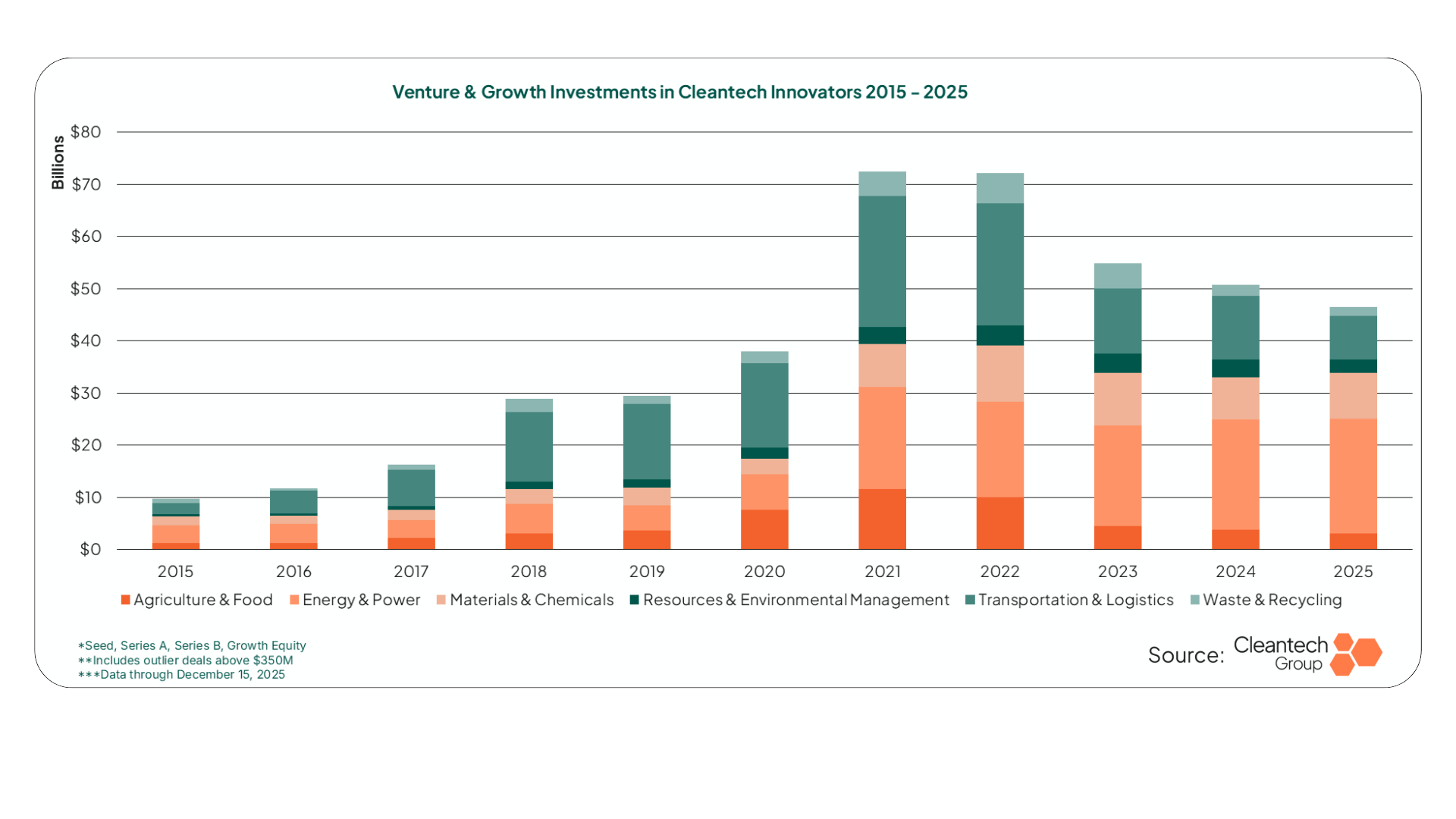

As we step into 2026, it is essential to take a step back and understand where we truly sit in the timeline of cleantech history. If you follow media reports following the space, you likely hear a narrative of a “drop-off” in venture and growth investments over the past few years. However, when we zoom out a full decade, a striking reality emerges: what comprised an entire year’s worth of cleantech investment 10 years ago now frequently happens in just a single quarter. Even as we move further away from the low-interest-rate environment of 2021 and 2022, the general trend remains decidedly upward.

It’s years like 2025 that bring into stark relief the multi-decade journey this theme is on, and the importance of understanding the long-term direction of travel across the many technology areas that comprise the cleantech theme. As we enter 2026, we can start seeing some clear patterns emerge within what has been an otherwise chaotic macroeconomic environment.

In 2026, we expect a “pressure cooking” effect. While the “Grow” category is packed with innovation, making the AI revolution more efficient and streamlining access to critical minerals, the pie is expanding at a rate that is attracting massive competition. Meanwhile, a fractured trade environment and high inflation are making it increasingly difficult for companies in the “Flow” and “Slow” rings to break out.

In conversations with many innovators, corporates, governments, and investors over the past year, it has become clear that sovereignty is the top priority at many levels of society. Governments are seeking more national sovereignty and bolstering defense, industries are seeking separation from unpredictable supply chains and sensitive commodities, and individual corporations are seeking less dependence on systems vulnerable to supply shocks and geopolitics.

The Drive for AI Supremacy and Infrastructure

The concept of sovereignty—national, and in some cases, corporate—is immediately present in the race to AI supremacy. Nations and corporations are increasingly desperate to “own” leading AI capabilities and eliminate international dependencies.

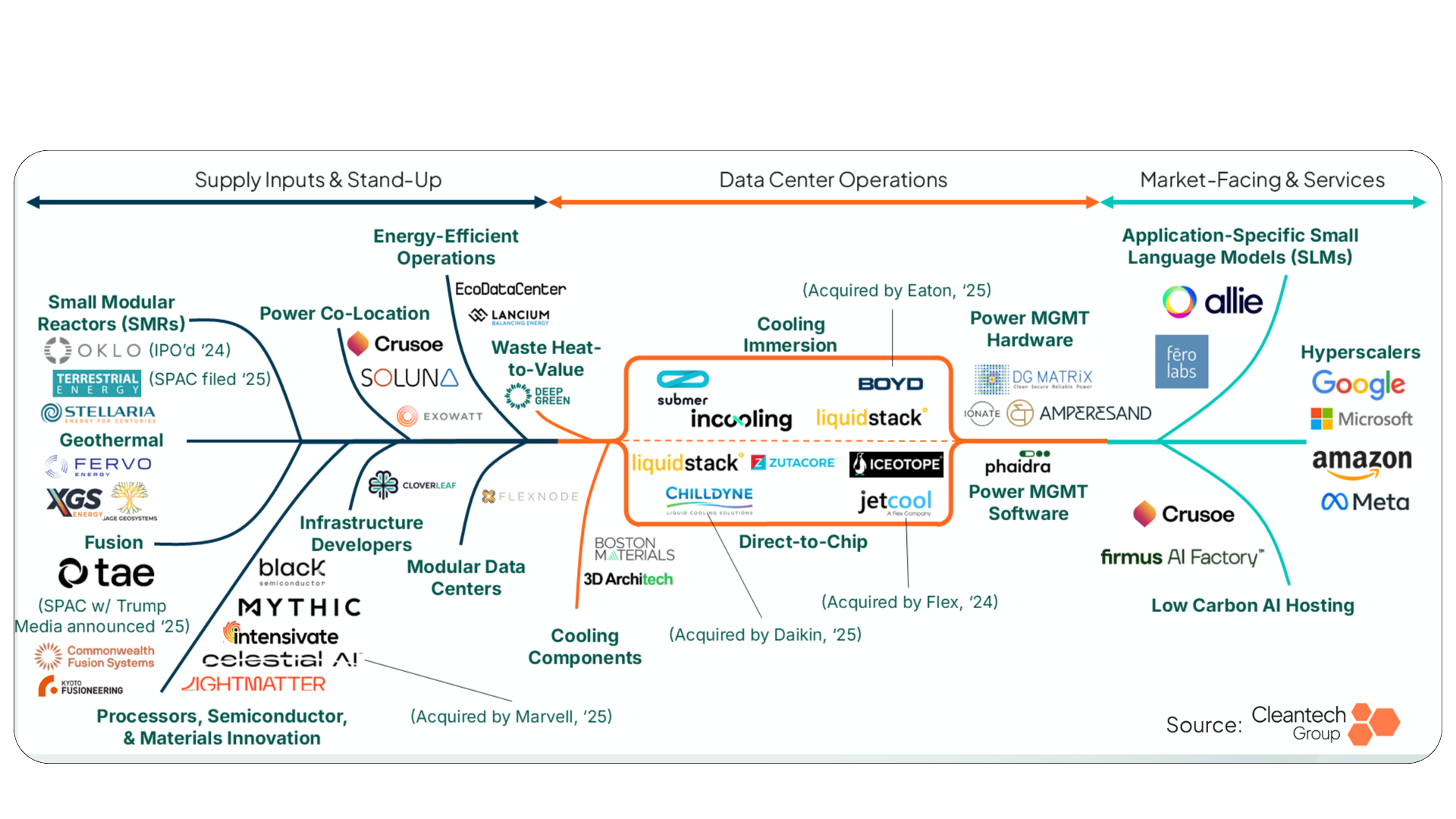

This drive has created a pull-through effect across the entire SMR-to-SLM (Small Modular Reactor to Small Language Model) continuum.

At the beginning of 2025, we predicted that it would be across this continuum that exits in cleantech would be found. That has borne out clearly since, even in an environment where cleantech exits have been sparse (tech exits in general, for that matter).

Indeed, the race to stake a claim in AI data center operations has placed industrial power electronics and HVAC companies in a position to be influential acquirers of innovative technologies:

- Daikin (an air conditioning giant) acquired direct-to-chip cooling company Chilldyne in November 2025.

- Eaton acquired Boyd Thermal in October 2025 to bolster thermal management offerings.

We expect that, with the continuing energy requirements of AI compute, liquid cooling will remain as a critical theme in 2026. Going even further, it is likely that—similar to chips and semiconductor materials—cooling technology is going to slowly work its way into AI sovereignty and national security conversations this year.

While HVAC incumbents acquiring liquid cooling companies may not be a shocking development for most, interesting developments are happening at the baseload power side of the continuum. In a more “left field” move, the merger between TAE Fusion and Trump Media Group highlights how even fusion energy is working its way into national security discussions via the AI supremacy conversation.

While the TAE and Trump Media deal grabbed the most headlines, 2025 was a year of significant commercial milestones in fusion, including Commonwealth Fusion’s power purchase agreements (PPA) with Google and Eni , and Helical Fusion signing Japan’s first-ever fusion PPA with Aoki Super.

Nuclear fission will continue to benefit from the AI race in 2026. Oklo announced on January 9th that it would receive early funding from Meta for a 1.2GW small modular reactor installation in Ohio. This announcement came just days after Terrestrial Energy announced signature of an Other Transaction Authority (OTA) agreement with the U.S. Department of Energy (DOE) on the path to pilot an Integral Molten Salt Reactor (IMSR). In December 2025, the DOE announced $800M in funding for SMR construction with the Tennessee Valley Authority and Holtec. The demand signals from hyperscalers, coupled with U.S. administration support provide a clear signal that the SMR space will continue to advance in 2026.

We expect that advanced geothermal will continue its upward trajectory in 2026, as a reliable source of clean baseload power for data centers, utilities, and even the defense sector. The momentum is building in advanced geothermal, with major reservoir discovery (see Zanskar’s October 2025 discovery of a site with 100MW potential), significant fundraising endorsements (see Google’s recent backing of Fervo Energy), and accumulating PPAs with innovators, including Fervo and Sage Geosystems. All signs point up in this space.

The “Race to the Center” of Compute Efficiency Rages on in 2026

And while there have been many headlines dedicated to the growing drive to secure baseload power for data centers, until recently, the energy-efficiency of the IT equipment has fallen outside of many climate tech conversations.

There is increasing conversation around the rate at which inference computing will increase in importance, versus today’s imperative of securing centralized facilities for AI training. As AI becomes more important in the physical universe (think Industry 4.0, autonomous vehicles, smart city, defense applications), more inference computing will move to the edge to reduce latency.

Innovation in AI chips for edge computing will increase in importance as a result, and we are already moving toward a reality where established chip suppliers see these edge-chip innovators as collaborators. This is substantiated by the $20B licensing deal betwee NVIDIA and Groq. We’ll be watching this space closely, especially as more commercial and industrial corporates seek to gain their own version of AI sovereignty, bringing AI services on-site.

Additionally, we expect activity at the nano level of cooling and heat management materials, such as Boston Materials (carbon fiber), NovoLinc (roll-to-roll manufactured, vertical copper nanostructures), and 3D Architech (3D-printed nanostructures), designed to transfer heat off chips in liquid cooling environments.

2025 was the most active year in recent memory with regard to grid tech deployments and investment. What is significant in this space is that the data center boom has stimulated demand pull across the value chain.

- New approaches to critical grid power management, e.g. solid-state transformers (see DG Matrix and Amperesand) and AI-enabled transformers (see IONATE) are re-awakening demand for a once thought commodity part of the grid. It’s worth noting that demand for new transformer types is coming from both the grids and the data centers they serve—creating two paths to market for innovators in this space.

- Software managing the grid has become more comprehensive, and the value chain offers multiple levels of solutions to manage an increasingly complex grid. Solutions ranging from sensor and software-based line ratings are being met with increasing demand urgency. Increasingly, the way the grid is modeled is becoming a linchpin to planning for unforeseen demand and complex risks (see physics-informed digital twin companies Neara and ThinkLabs).

- Importantly, there is an increased emphasis being placed on disaster avoidance and management—technology to plan for resilience (e.g., Rhizome) and monitor for threats from weather events (e.g., Iceye and Orora Technologies) will be essential to ensuring that the investments being made in grid hardware are able to deliver.

AI-Enabled Cleantech – Success Factors Are in the Details

It isn’t just the infrastructure side of the AI ledger that is poised to see activity in 2026; we also see a complex ecosystem of AI applications in cleantech. Looking beyond investments, we see AI in cleantech through the lens of “Zones of Opportunity”.

- Contested Commodities: Crowded spaces like Commercial Building management offering incremental OpEx gains to adopters.

- Battleground Bets: Competitive areas like materials discovery, which can push the envelope on R&D and scaling in deep tech spaces but have shrinking competitive windows.

- Unclaimed Upside: High-impact, under-saturated areas that create “0 to 1” revenue opportunities for adopters. See AI for mining and AI for geothermal (e.g., Zanskar) as tools that allow access to brand new projects that previously were not thought possible or not obvious.

AI is now taking aim at its own infrastructure challenges in some ways, as new AI tools seek to ease the challenges associated with the growth of the AI industry. While AI growth creates challenges for the power system, it is also promising to unlock efficiencies within that same system.

See the sheer amount of investment activity in AI for grid management this past year for an indication of how much the market is valuing these tools for speeding up grid growth and reducing operating costs. Importantly:

- Time-to-Power: Tools like GridCARE, GridUnity and Splight use AI and real-time data to find optimal routes to interconnection for both data centers and generating assets.

- Planning and Optimization: ThinkLabs is designing reliability into grid infrastructure projects from the initial planning stage, a recent collaboration between Thinklabs and Southern California Edison demonstrated reduction of time to run complex power flow models from days to minutes.

- Physical Monitoring: Companies like Prisma Photonics use fiber optic cables as acoustic sensors, while Gridware uses self-powered sensors to monitor asset health in real-time.

While not grid management per se, companies like Emerald AI and Hammerhead who are optimizing compute workloads in data centers are providing positive knock-on effects to the rest of the grid in managing the challenges associated with AI deployment.

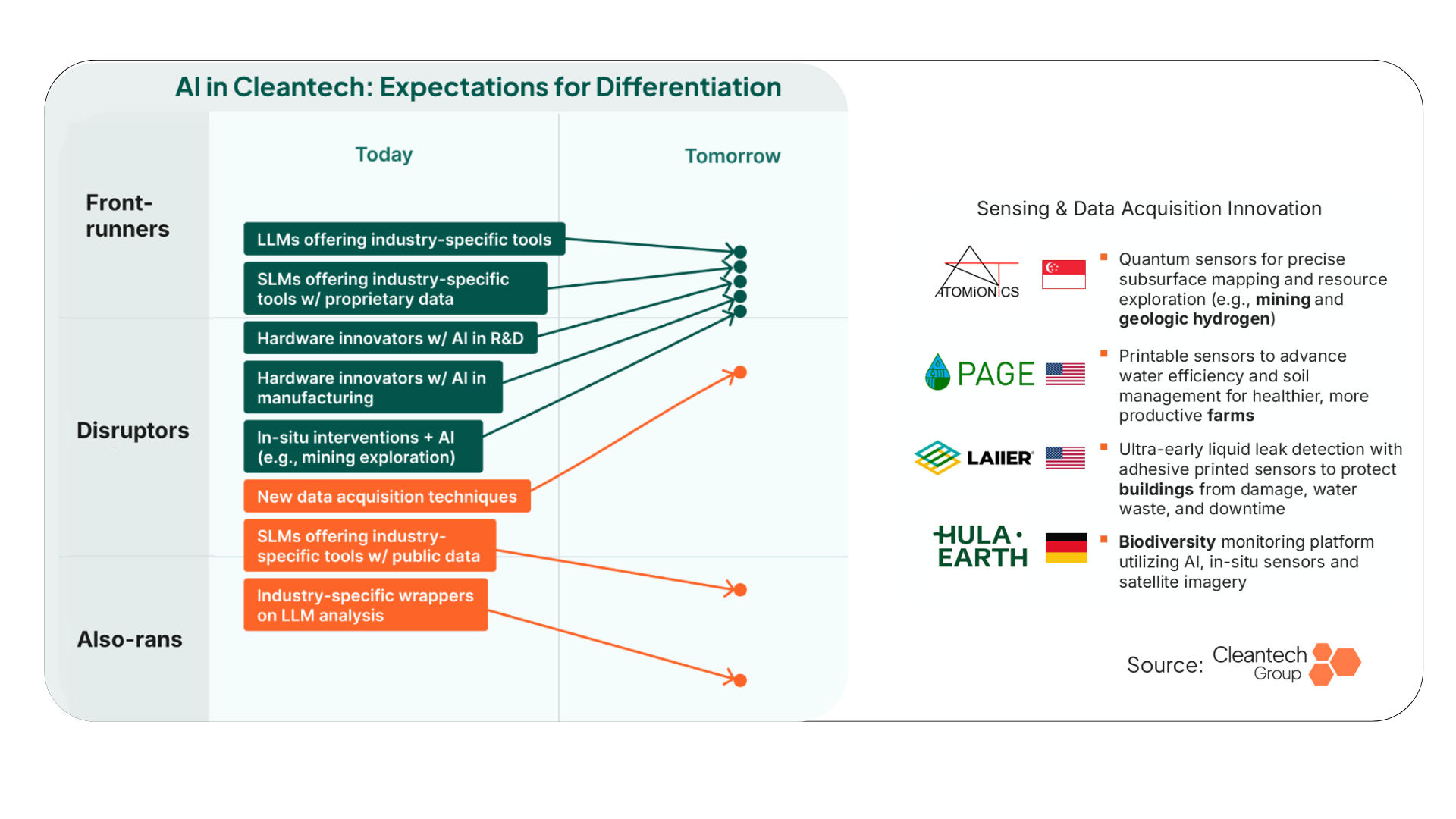

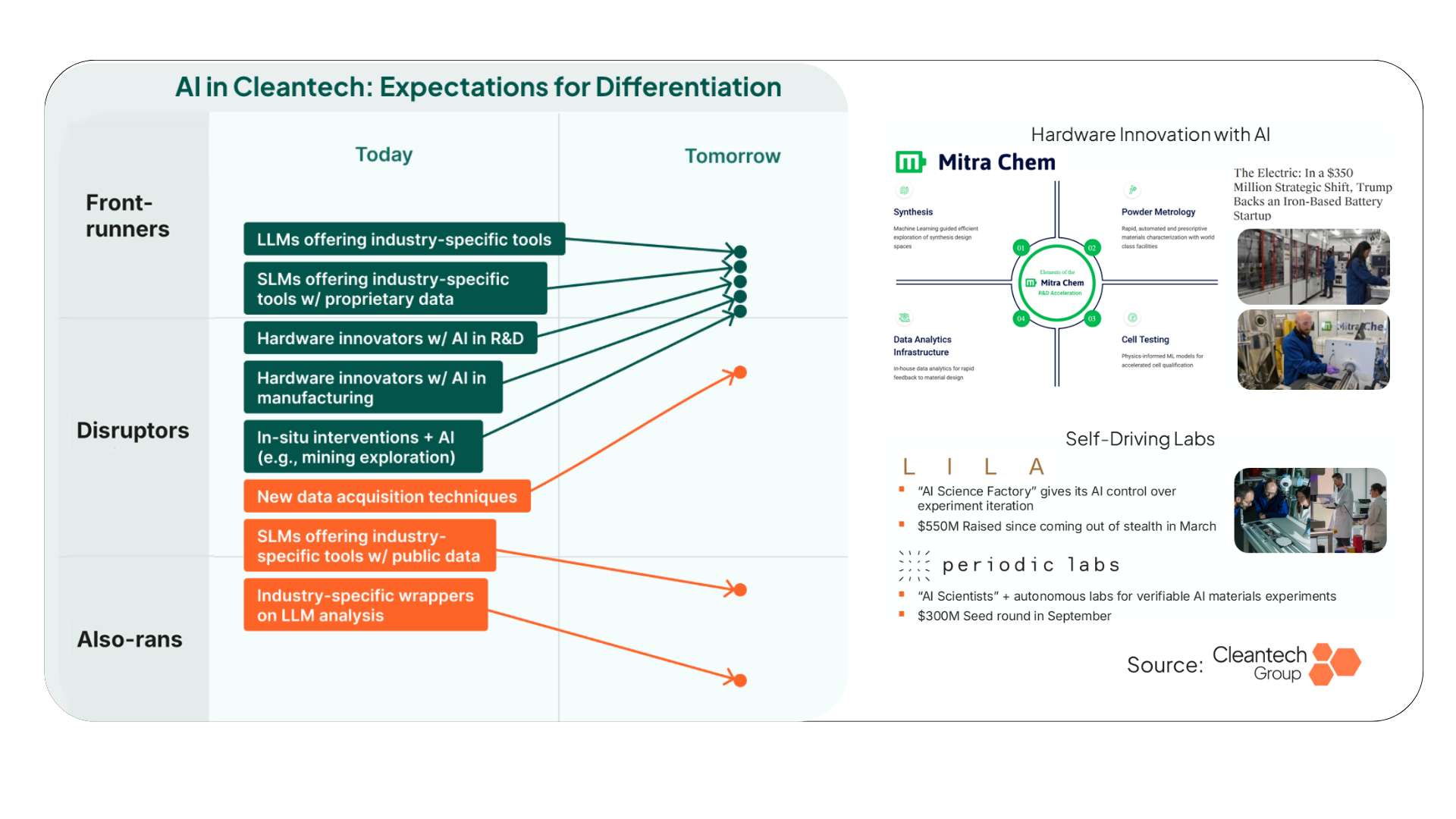

Differentiation Beyond Algorithms

While a reasonable question lingers around a potential AI bubble in cleantech, we expect the movements in the ecosystem to look less like a bursting bubble and more like a crashing wave—AI tools relying on publicly available data or wrappers around LLMs are unlikely to be able to compete, especially against companies with some type of proprietary data. In 2026, we expect significant differentiation from companies that have unique approaches to proprietary data acquisition.

- Atomionics: Quantum sensors for precise subsurface mapping in mining and geologic hydrogen.

- Page Technologies: Printable sensors for water efficiency and soil management.

- Laiier: Adhesive printed sensors for ultra-early liquid leak detection in buildings.

- Hula Earth: Biodiversity monitoring using Al and in-situ sensors.

We are witnessing a “wave of creative destruction” as software-only platform materials discovery plays are increasingly threatened by closed-loop science and self-driving labs companies. These are companies where AI is used not just to formulate materials, but to take control of experimentation and production in the physical universe. The ultimate advantage of companies in this space will be their ability to sell end products, not just platform services (IP ownership has long been a challenging business model question for materials discovery companies).

See momentum just in the past 12 months from companies innovating in closed-loop science:

- Mitra Chem: Utilizing ML-guided synthesis and physics-informed models to accelerate iron-based battery production. In late 2025, it was reported that Mitra Chem was included in a U.S.-Japan deal brokered by President Donald Trump to bring over $350M to the company.

- Lila: An “Al Science Factory” that gives AI control over experiment iteration, having raised $550M since March 2025.

- Periodic Labs: Utilizing “AI scientists” and autonomous labs for verifiable experiments, raising a $300M Seed round in September 2025.

We expect that in 2026 the continued development of closed-loop science will make many software-only materials discovery less viable.

The Cleantech & National Security Nexus Will Become More Apparent than Ever

The global push for more sovereignty and supply chain stability is drawing forward the security benefits of many clean technologies while also accelerating the growth journey of many companies at a rapid rate.

While some technology areas such as earth observation have obvious dual-use benefits, the realities of modern war have brought to the fore the need for more decentralization in critical systems: energy, water, fuel supplies. There are many cleantech sectors uniquely positioned to deliver on this decentralization, and we can see that reflected in the mix of cleantech innovations now gaining traction with defense adopters:

- In 2025, German defense technology company Rheinmetall partnered with e-fuels innovator INERATEC, calling synthetic e-fuels “indispensable for modern defense readiness”.

- The U.S. Defense Innovation Unit doubled down on geothermal at military installations in 2025 with an expanded initiative that includes Fervo, Zanskar, Greenfire, Sage Geosystems, Eavor, and Teverra.

No tech theme has seen a more obvious endorsement from the defense ecosystem than that of critical minerals. In July of 2025, the U.S. Department of War made a landmark agreement with MP Materials that included $400M of stock purchases and a 10-year agreement to purchase Neodymium-Praseodymium (NdPr). The Department of War subsequently provided a $620M loan to Vulcan Elements as a part of a larger partnership to produce magnets within the U.S. These demand signals are rippling through the supply ecosystem in real time.

While the defense interest has had an observable stimulating effect on the ecosystem, it is worth noting that technologies vary across mineral type, and at different levels of the value chain. Fast de-risking and prove-out of unit economics will still be essential for companies in the space to progress into market readiness in time to catch the demand wave that continues to roll right now.

We also see an observable set of demand signals coming from the defense industry when analyzing earth observation and weather modeling technologies. Earth observation technologies have for years been engaged for dual use (if a satellite imagery analysis can identify environmental damages, it likely can identify adversary troop movements…).

However, it’s notable just how fast the uptake is accelerating: in just the last few months of 2025, ICEYE secured a $2B contract with Rheinmetall for the German Ministry of Defence and agreements with the Finnish and Portuguese air forces for satellite monitoring.

As discussed in recent analyses, AI is allowing weather forecasts to move beyond traditional numerical weather prediction into lighter, but more accurate weather models. The defense industry is taking note: Tomorrow.io partnered with Palantir in 2025 to enable “end-to-end automated weather decision-making” across defense and government, while Atmo lists the U.S. Air Force and Navy as customers for its AI weather forecasting database.

Adaptation & Resilience: Tech Flowing to Market in Some Verticals, Battling Bottlenecks Elsewhere

Technologies for adaptation to climate change remain at a generally flat growth trajectory with regard to investments. However, it is important to consider that the technology surface area in adaptation and resilience is wide and addresses many different types of customers. As such, the technology verticals grow at different speeds.

Cleantech Group’s Adaptation & Resilience “Velocity Gradient” finds the majority of technologies falling into one of two slices: highly competitive supply ecosystems (“Competitive Drag” and “Pulsed Flow”) without ideal buying signals, or clear customers but who are engaging disaggregated technology suppliers (“Customization Drag” and “Linear Stream”). The spaces that are breaking out, such as grid monitoring and earth monitoring, have rich supply ecosystems with a high degree of cross value chain collaboration and a robust buyer ecosystem that speak a common language.

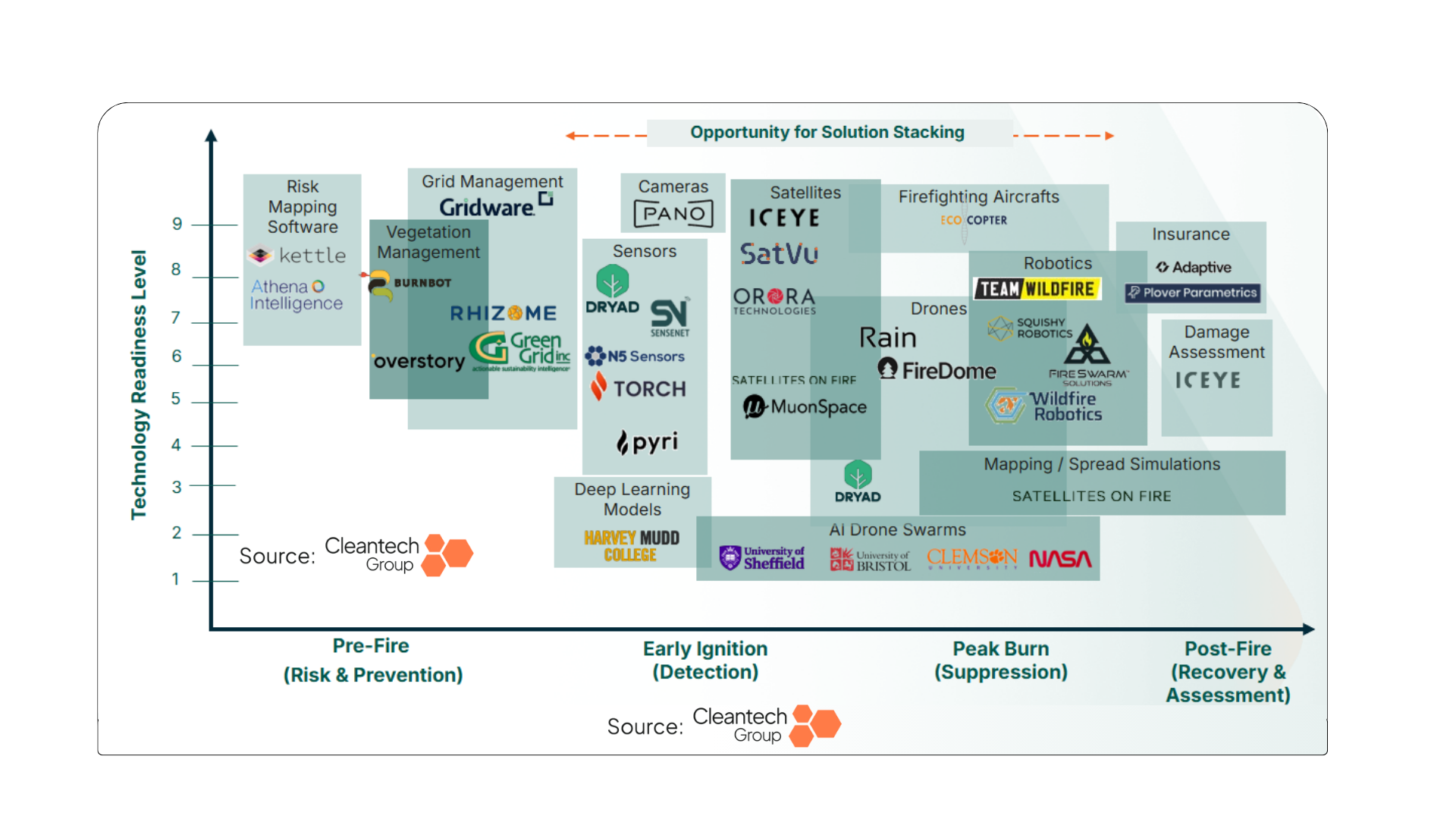

While the private sector has been slow to back some adaptation technologies, wildfire detection is a bright spot that is edging towards the middle high-velocity category. In 2025, wildfire tech saw its biggest year of investment yet. We are moving out of the “niche market” (restricted to high-risk areas) and toward a “market-winning scenario”.

The characteristics of the market that have allowed wildfire detection to break into a faster growth path include:

- Technological Fusion: Al algorithms now fuse sensor, drone, and satellite data to eliminate false positives, allowing innovators to take technologies off the shelf or collaborate to deliver high effectiveness.

- A highly integrated supply ecosystem, now with technology across the fire “lifecycle” to address risks (see the surface area of technologies, below).

In wildfire technologies specifically, the buyer pool has also moved beyond just utilities and insurance companies in the most exposed regions to a demand ecosystem that is slowly becoming more global and diverse (commercial and industrial customers are now entering the demand pool).

A testament to increasing customer fluency in wildfire detection systems is the ability of companies using lower-cost, low friction technologies to deliver insights without high levels of customer education. See 2025 LATAM Cleantech 25 awardee Satellites on Fire, using established supply chains to deliver a highly affordable detection service.

What Will Continue Facing Headwinds in 2026?

We posited in January 2025 that carbon removals would be a sector comprised of supply chasing demand. That has proven to be the case in the 12 months since. While investments ticked up in 2025, the amount of deals dropped significantly. The buyer pool is far too small; a heavy majority of purchases are made by Microsoft alone, with too obvious an absence of a rich buyer pool to have confidence that the market can absorb the sheer amount of technology in the system today. While the early demonstrations happening today may provide the basis upon which these technologies can come down the cost curve for the 2030s, this space will remain challenged in 2026.

Hydrogen has been challenged on both supply and demand sides of the equation in the past year. In January of 2025, we predicted headwinds in hydrogen, mostly on the basis of production costs, but project cancellations from major players like Statkraft, Neste, and Shell have intensified the chill in the sector. The new hydrogen markets once pursued by innovators, markets like seasonal energy shifting, distance transport, have not yet borne out, leaving hydrogen mostly confined to traditional spaces like ammonia fertilizer production. In these conventional spaces, there is much work to be done in reducing the cost of hydrogen production to meet buyer price tolerance.

Coming into a year where we feel patterns are emerging in the volatility, we feel there is more to the picture even than what has been discussed throughout this article. See our 2026 Bingo Card for a few more predictions, below. As always, feel free to reach out and trade perspectives with us.

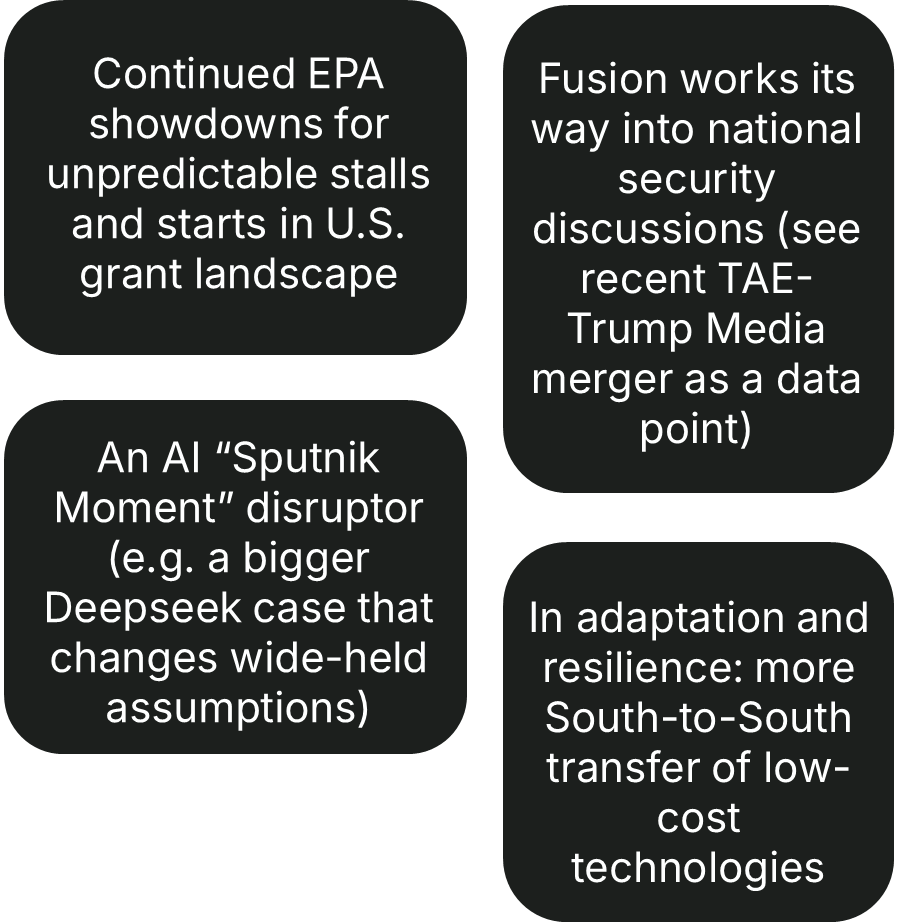

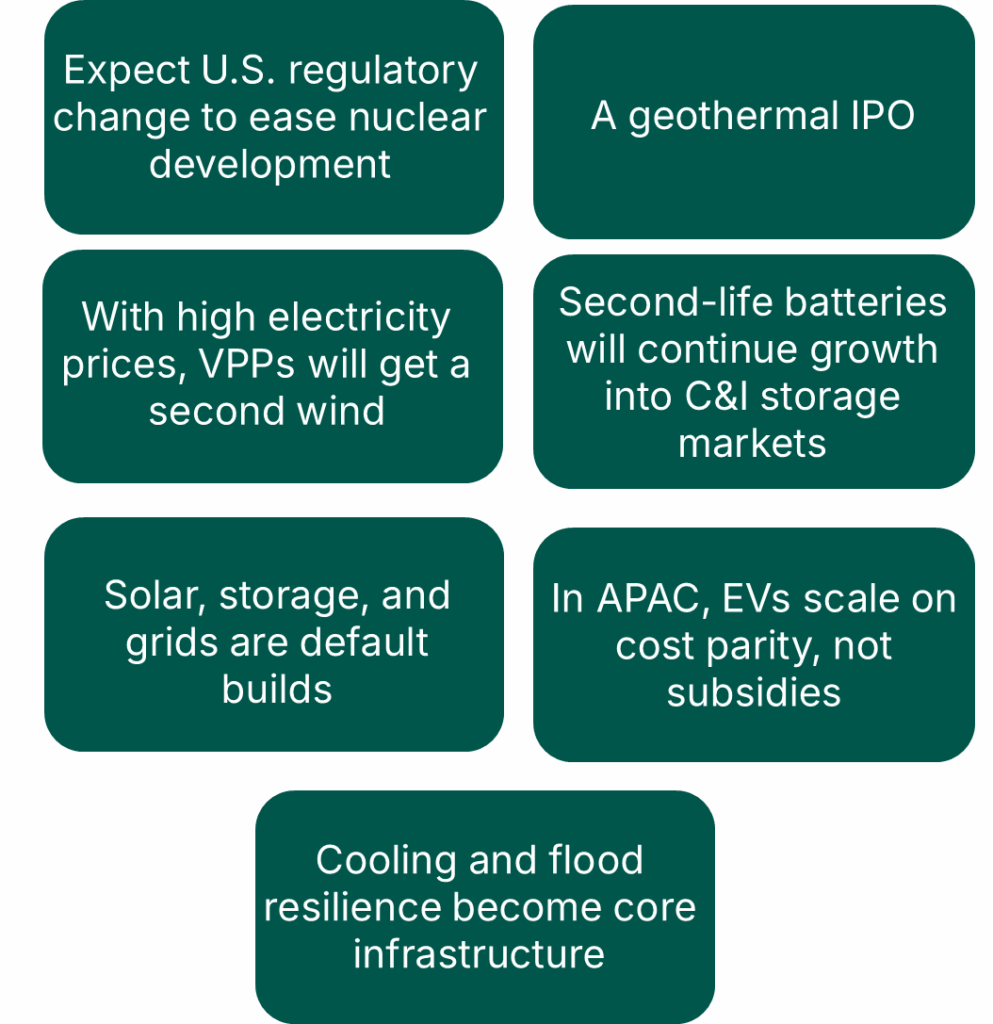

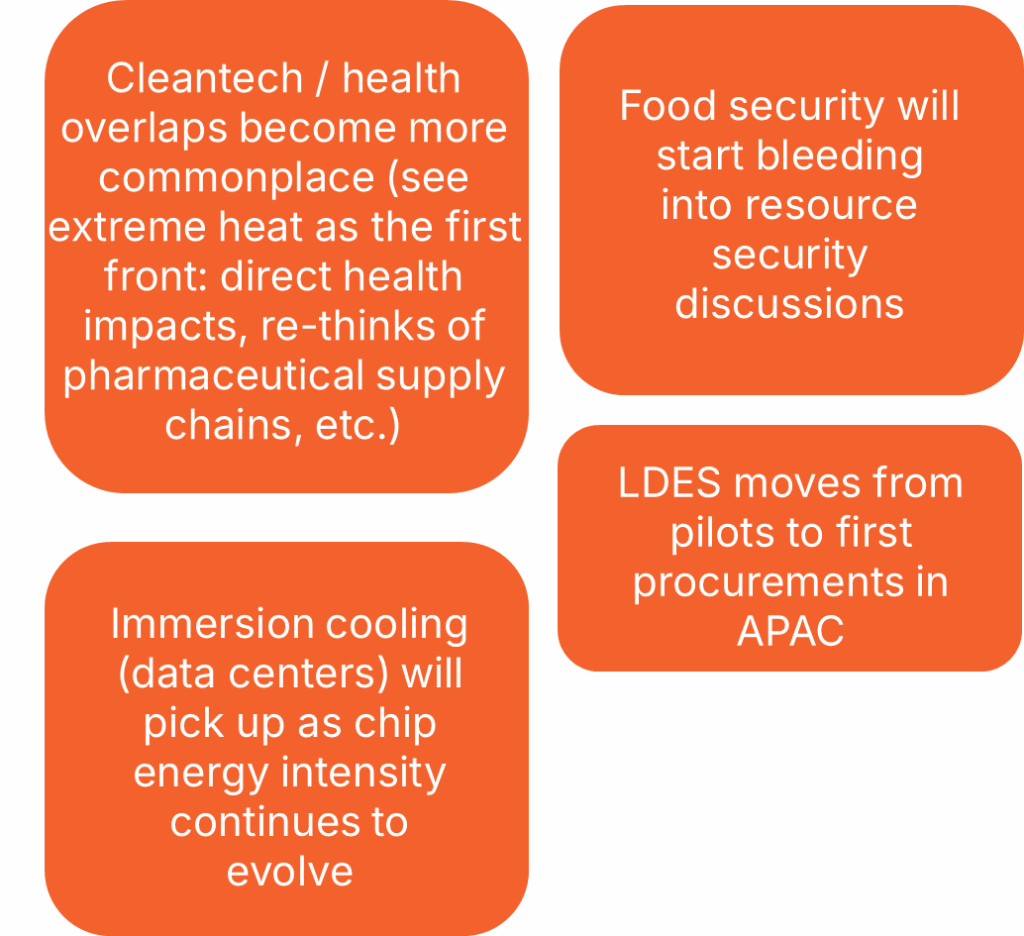

2026 Bingo Card: What Else Do We Expect?

Safe Bets

Coin Flips

Swing Factors