In last quarter’s APAC analysis, we covered a wave of electric mobility deals that indicated a growing market for vehicles and infrastructure developed in APAC, for APAC. And while investment numbers were notably quieter overall in APAC this quarter, a different trend was on display underneath the top-line numbers: budding momentum in highly exportable technologies. Fusion and energy-efficient compute were the most observable trends this past quarter, though with some continued enthusiasm for critical materials innovation.

Fusion in Japan: Is a Cluster Developing Before Our Eyes?

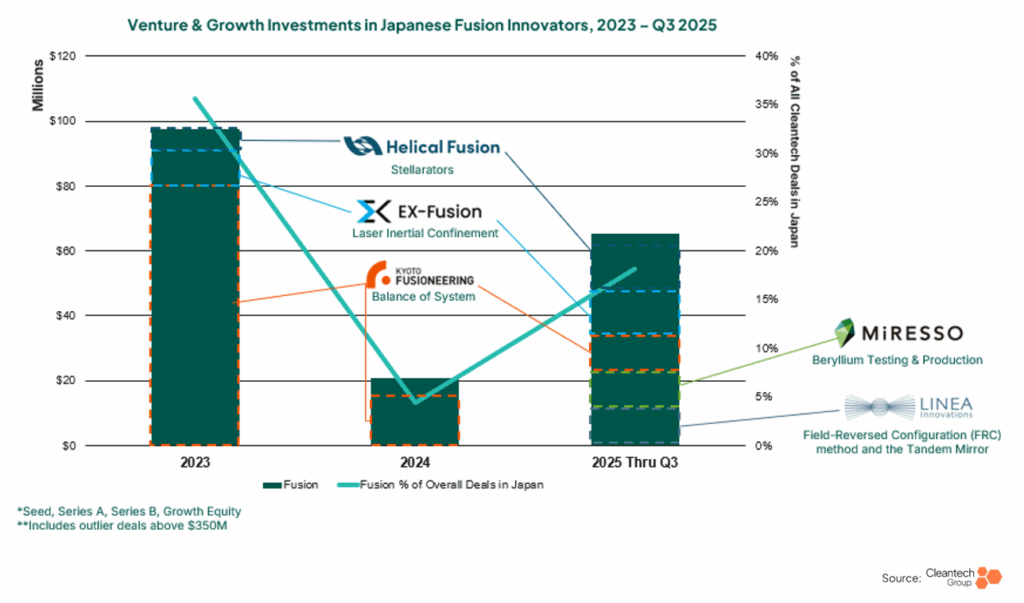

Progress continues in the advancement of an emerging fusion industry in Japan. While the investments in Japanese fusion dipped last year, we see continuity in the companies that comprised a landmark 2023 fundraising year in Japan once again making leaps forward in development.

The investment deals only tell part of the story-–it is becoming clear that Japan intends to not only bring fusion to its power supply, but also to stand up a comprehensive ecosystem of suppliers and technical know-how. There are clear advantages building in Japan, and all indications are that the country sees itself as a potential global fusion innovation cluster.

Earlier this year, the Japanese government revised its Fusion Energy Innovation Strategy which aims to achieve power generation demonstration by the 2030s (earlier than the previous target). This strategy emphasizes:

- Public-Private Collaboration: Actively bringing start-ups and major industry players together (e.g., through the J-Fusion Council).

- Building a Domestic Supply Chain: Shifting focus from just international collaboration (like ITER) to building a domestic fusion ecosystem.

Japan holds a critical position in the supply chain for high-temperature superconductors (HTS), which are essential for compact magnetic confinement reactors (e.g., those used by Tokamak Energy and Commonwealth Fusion Systems).

Fujikura Ltd. and Furukawa Electric Group are major, established Japanese incumbents in the HTS wire and magnet technology space, and are global kingmakers in fusion.

- Fujikura has invested in both the Japanese start-ups (Kyoto Fusioneering and Ex-Fusion) and U.S.-based Commonwealth Fusion Systems (CFS), to which it also supplies HTS wire.

- Furukawa Electric has partnered with UK-based Tokamak Energy to establish a joint operational base in Japan for HTS magnet manufacturing, also supporting the domestic FAST project.

So far in 2025, we have seen some familiar Japanese fusion companies refresh their coffers with new investment rounds but are also seeing newer companies enter the scene. What’s striking about the mix of fusion innovators that Japan is launching, is that there is not just one reactor type or component that Japan is showing strength in-–there is a diverse range of technologies that can serve different corners of the future fusion market.

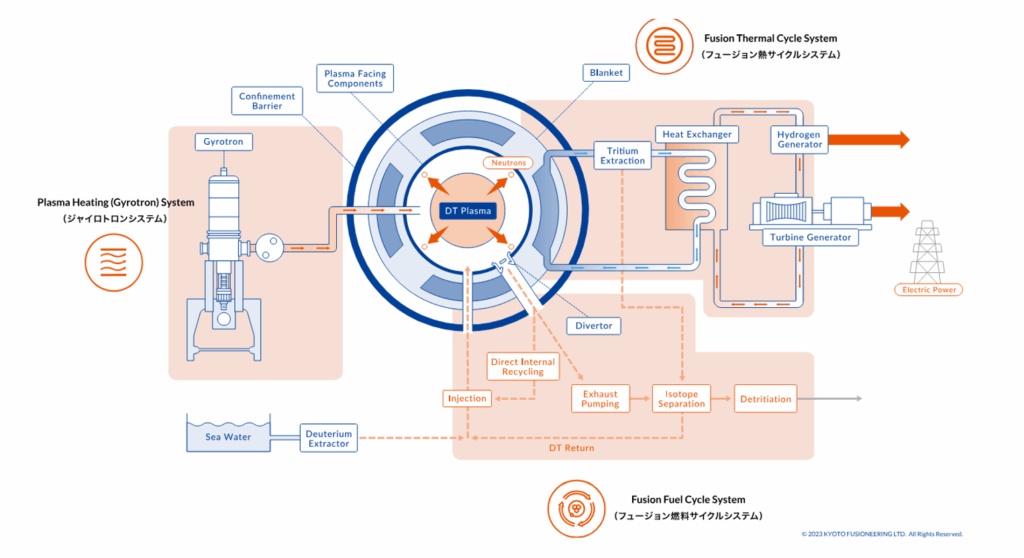

Not a reactor company, but a balance of plant (BoP) supplier, is Kyoto Fusioneering (a 2024 Cleantech APAC 25 awardee). For fusion energy, the BoP components are one of the most significant hurdles in transitioning from a scientific experiment (like ITER) to a commercial power station. Kyoto Fusioneering’s core systems include:

- Fusion Thermal Cycle System (Energy Conversion): The technology required to extract the immense heat generated by the fusion reactor and convert it into usable electricity or industrial heat. This includes the inner blanket structure, liquid metal loops, and heat exchangers.

- Fusion Fuel Cycle System (Tritium Management): The systems needed to process, recover, and re-circulate the fuel, particularly Tritium, which must be bred within the reactor itself.

- Plasma Heating System (Gyrotrons): The specialized, high-power microwave systems necessary to heat the fusion fuel (plasma) to ignition temperatures.

The BoP focus forward positions Kyoto Fusioneering for an industry that will have consistent demand pull and can benefit from cost efficiencies that Kyoto Fusioneering’s modular approach enables. The company tacked on $9.8M to a recent Series C in September.

Elsewhere in fusion supplies and services, MiRESSO raised a $12.4M Series A in August. MiRESSO is a service provider to fusion companies, using a proprietary low-temperature refining technology (alkaline solution and microwave heating) that operates at 300° C/normal pressure, significantly reducing the cost, energy, and CO2 emissions associated with traditional high-temperature refining.

Kyoto Fusioneering’s Balance of Plant System

There has also been activity in Japanese fusion reactor companies this year-–again, note the variety in approaches of companies getting funded:

- Helical Fusion ($15M Series A in July): Stellarator-type magnetic confinement. Leveraging Japan’s long history with the Heliotron concept, they are developing their Helix Program to achieve practical fusion. Note: Helical Fusion will be a speaker at Cleantech Group’s upcoming Tokyo Spark Event December 3rd.

- Linea Innovations ($12M Series A in June): Field-Reversed Configuration (FRC) and/or Mirror confinement concepts, building on Japan’s expertise in these alternative magnetic approaches.

- EX-Fusion ($16M Series A in June): Commercializing laser-based inertial confinement fusion (ICF), a technology that creates fusion by compressing fuel pellets with high-power lasers.

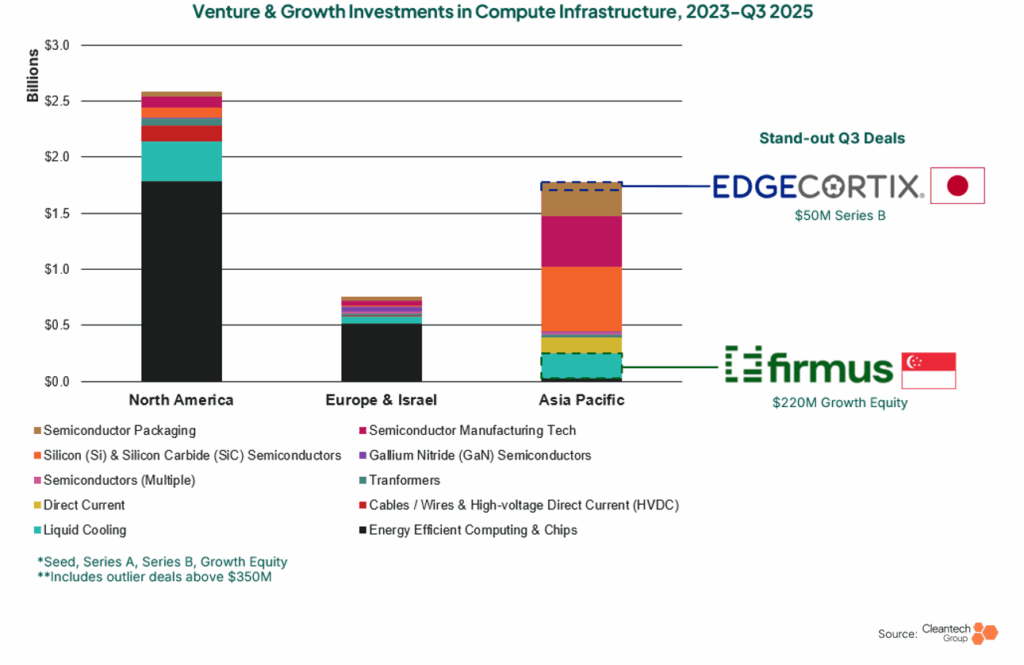

Energy-Efficient Compute: APAC Innovation Will Hit Global Markets in Short Order

We wrote earlier this year about the emerging prominence of APAC innovation across the spectrum of energy-efficient compute. And while it’s a challenge to stack up to the North America investment numbers right now, we are seeing APAC innovation getting global recognition in this space, and some growing companies with a clear global expansion path.

Taking on the daunting task of cooling data centers at the equator, Firmus Technologies is slashing energy for hyperscalers through an end-to-end liquid cooling system for high-intensity compute. Firmus’ key products are its modular 1-MW single-phase immersion “HyperCube” AI-Factory containers, run by the in-house FactoryOS platform. In September, Firmus raised a $220M round, including participation from Nvidia, who will be a partner at Firmus’s forthcoming 150MW Project Southgate, which has reported ambitions to eventually scale to 1.6 GW.

Chips and semiconductors for AI efficiency remain a key area of focus in APAC, though we are observing a shift toward niche markets where demand pull for edge computing cases is strong. Think defense, smart cities, industry 4.0, intelligent vehicles-–any instance where processing efficiency and response time is crucial. EdgeCortix (Japan) has developed the SAKURA-II AI Accelerator, bringing generative AI to low-power chips that sit directly in the point-of-use. EdgeCortix raised a $50M Series B in August.

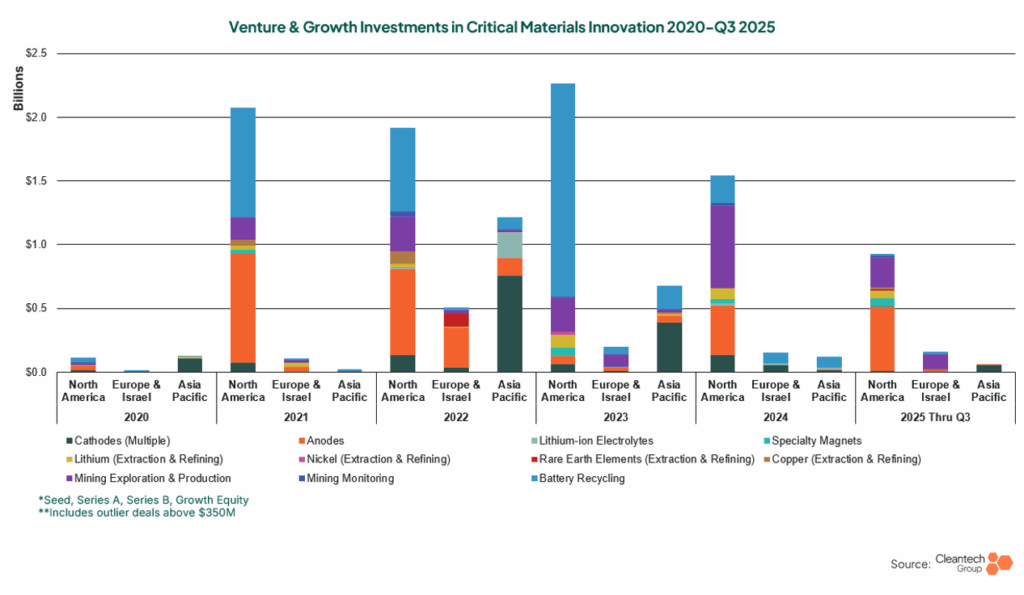

Critical Materials Innovation in APAC – Will it Rebound in Q4?

While investments in APAC critical materials innovation has cooled over the past two years, the drive to diversify supply chains continues globally, and APAC is still launching exportable technologies that can support home markets, and friendly market supply chain diversity.

A new frontier in subsurface mapping, quantum sensing offers a unique opportunity to model underground mineral deposits and develop surgical strategies for extraction. Atomionics of Singapore has developed the GRAVIO™ quantum-grade gravity sensor and the OREO™ AI geologist software, which together act as a “virtual x-ray” for the Earth. Atomionics claims that its quantum sensing enables high-resolution subsurface mapping up to 10x faster than conventional methods, with potential to reduce failed drilling (waste) and minimize environmental impact. Note the interest from both the mining and defense industries- Atomionics’s September $12.7M.

The drive to diversify supply chains also includes continued innovation in energy storage products, both for mobility and stationary applications.

- 3DC of Japan (2025 APAC Cleantech 25) creates high-performance battery components using Graphene MesoSponge® (GMS), a cutting-edge 3D carbon material developed at Tohoku University.GMS is used to enhance battery performance in applications such as conductive additives and advanced silicon-based anodes for lithium-ion batteries. 3DC raised a $16.7M Series A in August.

- Offgrid Energy Labs (India) has created a unique ZincGel® battery technology for cost-efficient, safe, and long-duration stationary energy storage (6-12 hours). The technology uses abundant, non-toxic zinc-bromide chemistry, offering a safer and more sustainable alternative to lithium-ion for large-scale grid applications. Offgrid Energy Labs raised $15M in a Series A in September.

APAC’s latest activity underscores that even in a quieter quarter, the region is laying the groundwork for technologies with global impact and long-term competitive strength.