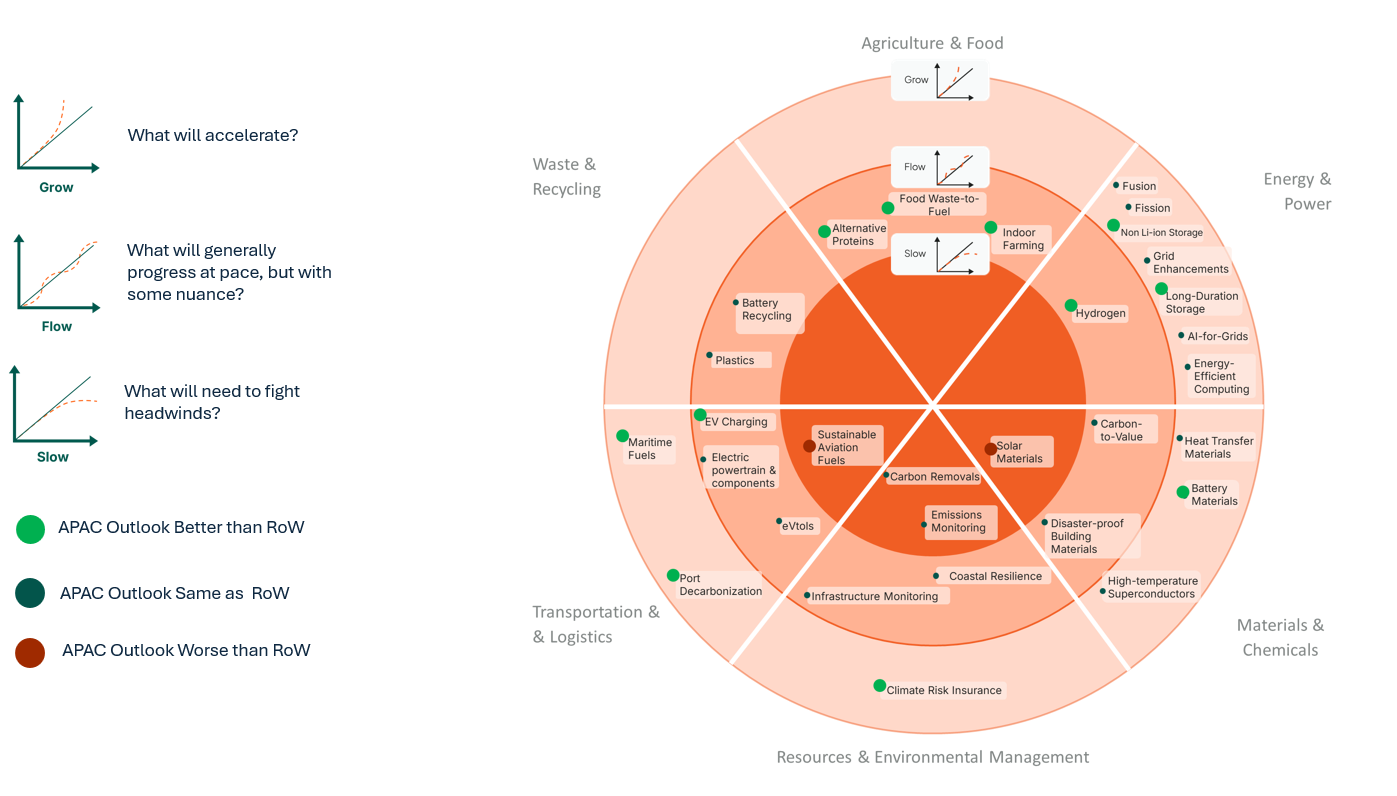

In our 2026 annual outlook and Global Cleantech 100, we described the cleantech theme experiencing a “Pressure Cooking” effect in 2026. Much of the global cleantech theme is experiencing this effect through a combination of: 1) a race to sovereignty (AI supremacy, cleantech for national security), and 2) the drop-off of some deeper decarbonization technologies due to project cost realities and policy melt.

In some technology areas Asia Pacific is moving in lock step with the rest of the cleantech world (e.g., AI infrastructure, critical minerals), but digging a layer deeper, it becomes clear that Asia Pacific is moving forward in some of the areas that the West is putting on pause, but also is also continuing full speed in technologies developed in APAC, for APAC.

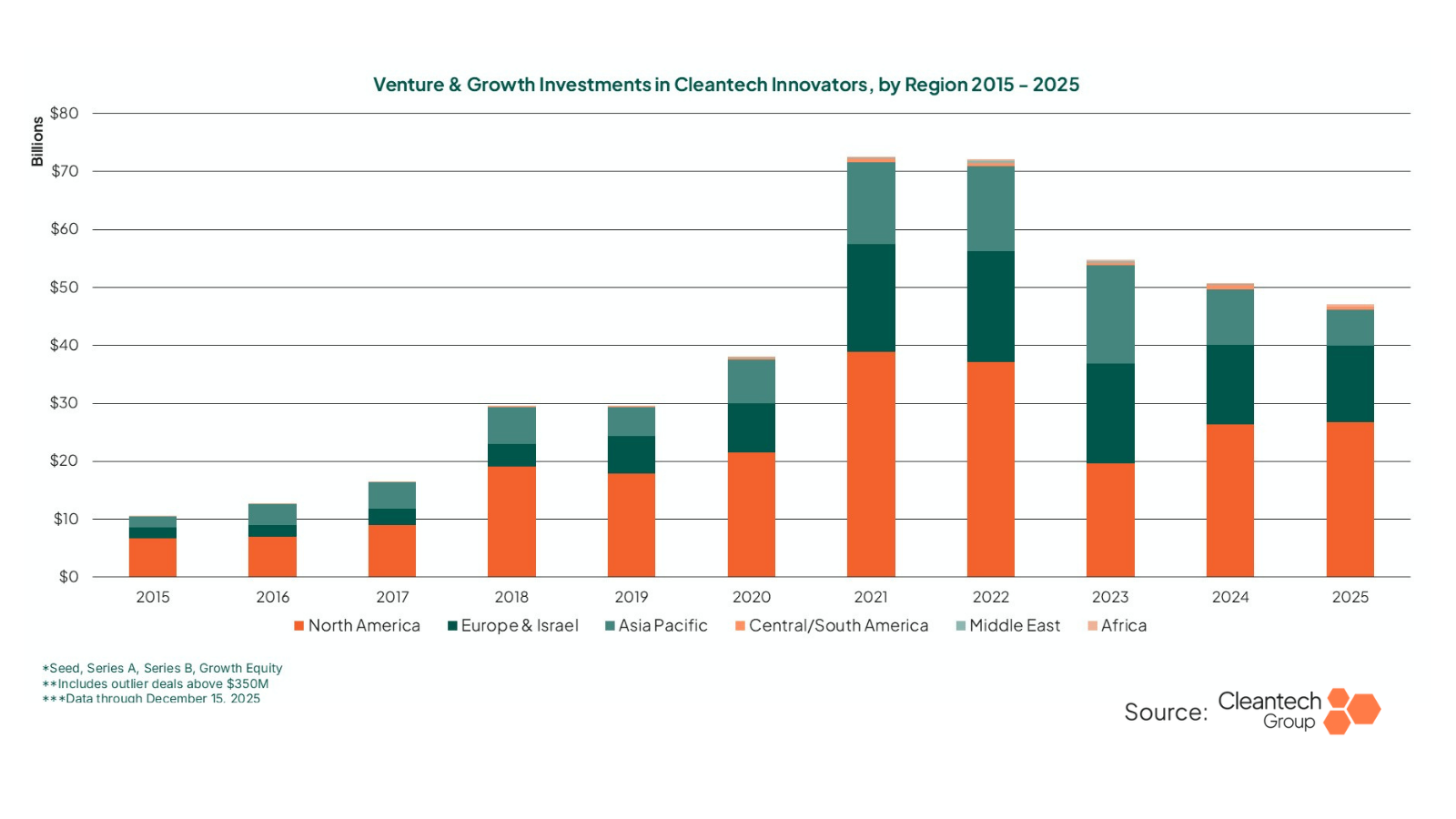

On the surface, investment numbers in APAC-based cleantech innovators told a glum story in 2025, returning the lowest top-line investment figure since 2019. With certainty, part of this story is the dramatic speed with which Chinese innovators in solar, battery storage, and EVs have either exited or graduated the equity continuum and moved into debt and project financing. Indeed, local champions are emerging elsewhere in APAC, and growing into regional incumbents as a result, see India’s Ola Electric Mobility, who IPO’d in 2024 after a series of debt rounds totaling nearly $300M. The growth of local champions like Ola and Ather Energy in India has enlivened an ecosystem that other electric two-wheeler innovators can thrive in (see discussion on Indian electric mobility further below).

Fusion in APAC 2026 – A Battle of Breakthroughs

If purely following investment dollars, the U.S. is dominating in fusion innovation. And while much of the innovation and initial corporate partnerships are happening in the U.S., this is a space that has not been “won” on a global level yet. 2025—and indeed, the first few weeks of 2026—leave us confident in the hypothesis that Chinese and Japanese fusion innovators will become even more globally competitive in 2026.

China’s back-to-back triumphs—setting a 1,066-second plasma record in January 2025 and shattering the Greenwald density limit in January 2026—signal the early results of the country’s drive to be a global fusion competitor. The encouraging scientific results are likely to ripple through the ecosystem, allowing the tokomak innovators in China to develop more critical mass. In 2026, we’ll be watching Chinese tokomak innovators Energy Singularity and Startorus Fusion closely. Both companies have begun building war chests to ready themselves for the lift ahead: Energy Singularity raising $240M in spring of 2025, and Startorus $143M in January 2026.

Helix Fusion’s Katana Helical Stellarator

Japan has long been global fusion research powerhouse, and is home to the world’s leading high-temperature superconductor manufacturers. When examining the fusion innovation ecosystem in Japan, what becomes immediately apparent is that there is a wide surface area of fusion innovation taking hold, with innovators less competitive with each other domestically and more attempting to bring different reactor types or components to global markets. There

- Kyoto Fusioneering has quickly become a “tier-1 supplier” to the global fusion industry, supplying the vital components needed by most in the industry, such as gyrotrons (high-power plasma heaters) and tritium fuel cycle systems. In November, 2025, Fusion Fuel Cycles Inc., a landmark joint venture between Kyoto Fusioneering and Canadian Nuclear Laboratories (CNL) began construction on UNITY-2. UNITY-2 will be the first facility in the world to demonstrate a complete deuterium-tritium fuel cycle at a scale ready for commercial power plants.

- Helical stellarator innovator Helical Fusion announced in December 2025 Japan’s first-ever Power Purchase Agreement (PPA) for fusion energy with Aoki Super.

- Laser inertial confinement innovator Ex Fusion is planning to establish its own facility and begin manufacturing key components off the back of a December 2025 fundraise.

- MiRESSO is aiming to become a global Beryllium supplier. The company uses a proprietary low-temperature microwave refining process to produce Beryllium, a critical “neutron multiplier” metal required for fusion reactor blankets.

- Clean Planet is developing Quantum Hydrogen Energy (QHe) fusion with “Condensed Matter Nuclear Science” techniques. These techniques generate heat at much lower temperatures (under 900°C) than plasma fusion.

Indian Electric Mobility Faces a Crucial Window on Small Vehicle Leadership in 2026

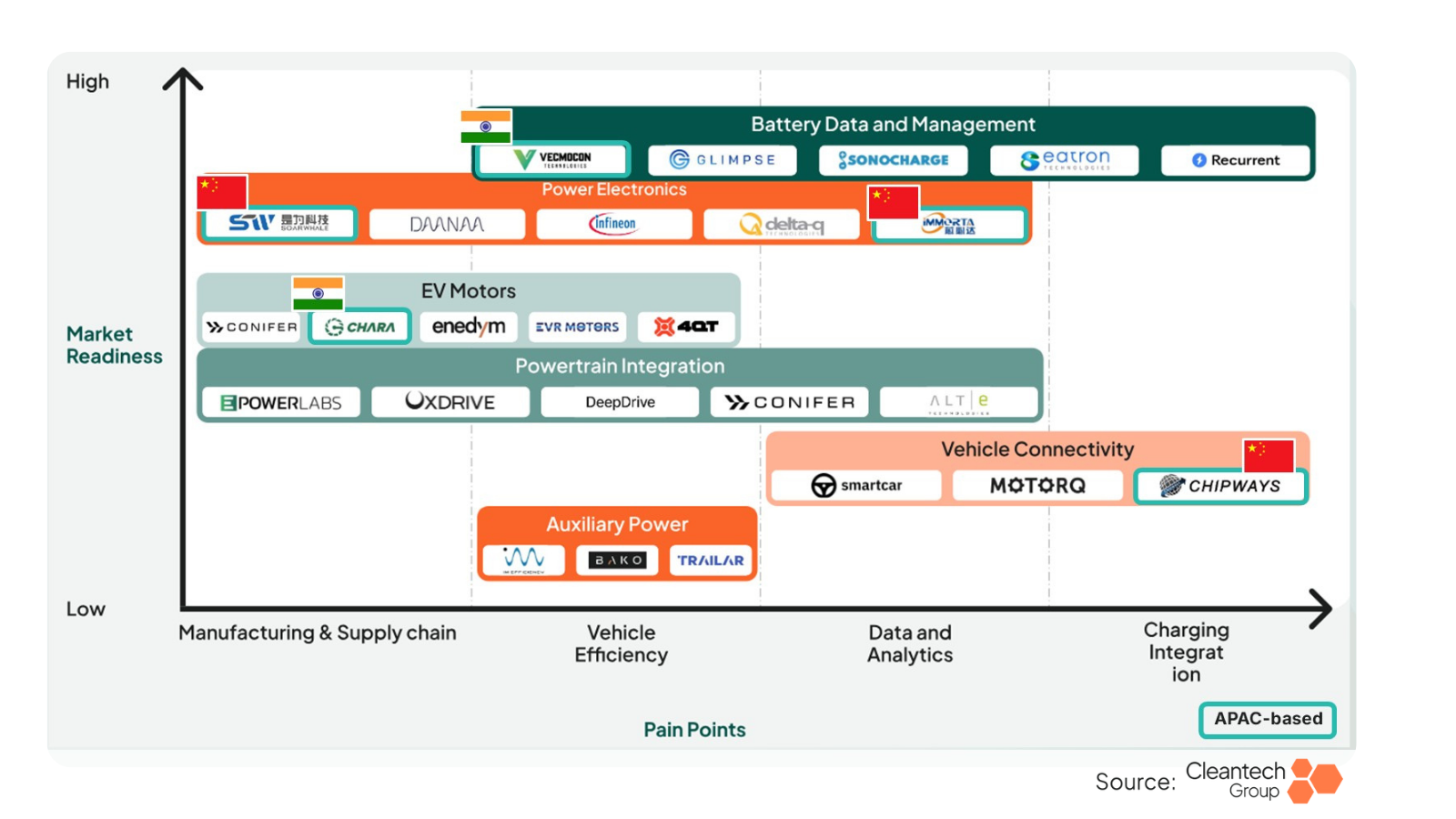

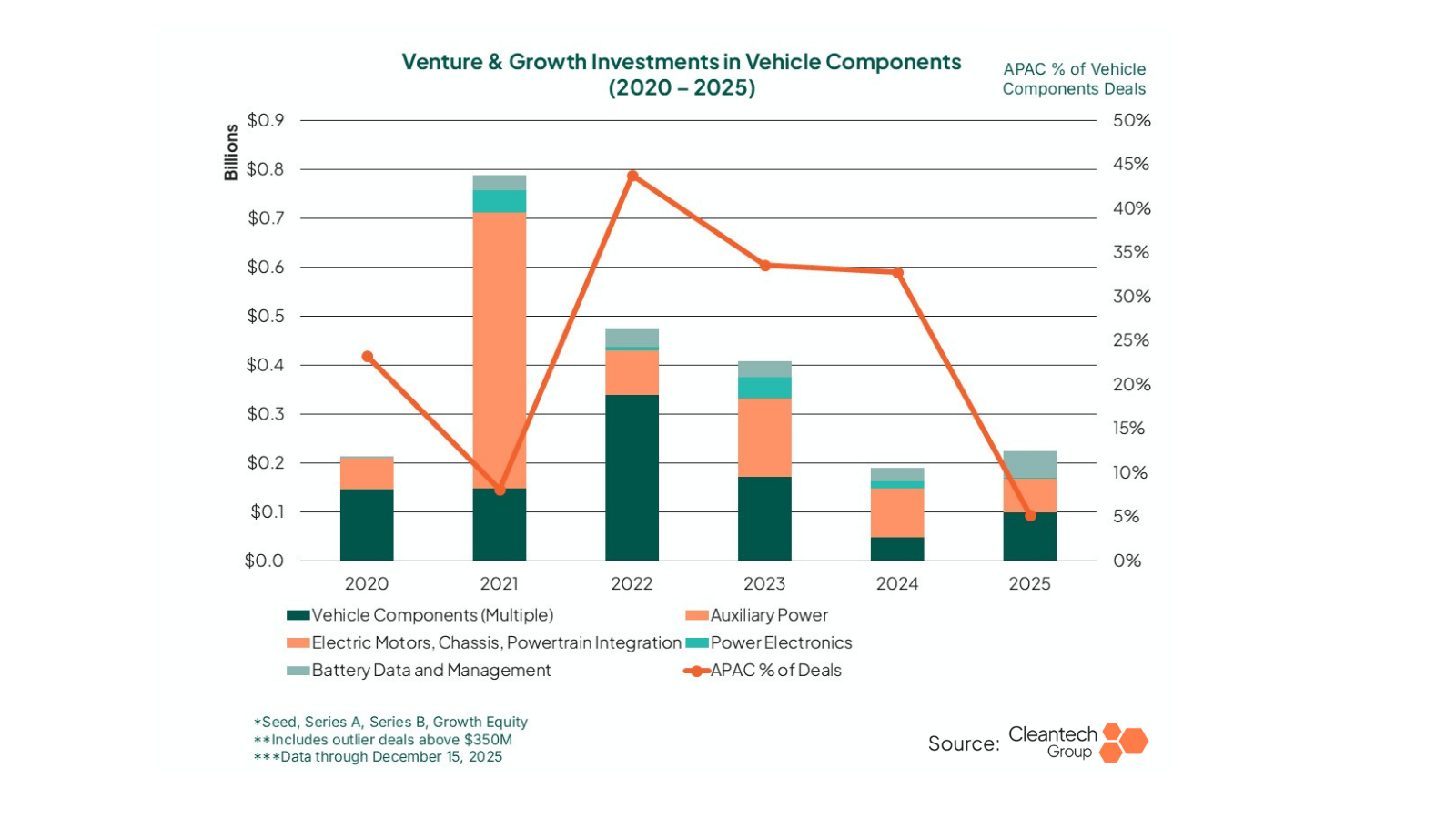

The high penetration rate of electric vehicles in the Asia Pacific, especially electric passenger vehicles, buses, and trucks in China, but also electric two and three wheel vehicles in India. This has created an above-average presence of APAC players in the ecosystem of top components innovators.

Innovation in Vehicle Systems and Components

And while the investment numbers show a clear downward trend for APAC innovators in 2025, this is likely more a matter of the “graduation” effect mentioned above. As the leaders in vehicle production settle into a rhythm of bankability, we expect the market adoption speed to continue generating a pull-through effect on electric mobility innovation in APAC, but in some specific spaces.

We noted in mid-2025 that we expected an ecosystem of both electric two-wheelers and EV charging infrastructure in India to flourish. That has largely borne out, but India will enter a crucial phase for innovators in 2026: India is slated to end its primary volume subsidies for electric 2-wheelers in March 2026. The market will transition to performance-based incentives (e.g., minimum 80km range, 40km/h top speed, and regenerative braking), meaning that companies in this space will need to compete on market economics of vehicles or move into higher-performance product offerings.

The supply ecosystem appears to be ready for the next phase of growth, with a robust value chain for electric mobility that has crystallized in India in recent years:

- Ultraviollette developed India’s first premium electric sports motorcycle that rivals 300cc-400cc ICE bikes in speed and technology

- Everest Fleet is one of India’s largest fleet management companies, providing thousands of EVs and CNG vehicles to ride-hailing giants like Uber and Ola while scaling up its green-only logistics

- Chara has developed “rare-earth-free” motors and controllers, using innovative Synchronous Reluctance technology to reduce India’s dependence on imported magnets.

- Neuron is a specialized manufacturer of high-performance Lithium-ion battery packs for 2-wheelers, 3-wheelers, and light commercial vehicles, focusing on smart BMS and domestic GWh-scale production.

Importantly, the growth in electric mobility has created reverberations throughout the Indian transport sector, with new and novel transport for cold chain technologies coming out of the country.

- New Leaf is a unique system that achieves low temperatures for transport and stationary cooling directly powered by biomass rather than powering system with electricity produced from biomass

- Yotuh has developed a battery-powered refrigeration unit independent from vehicle drive, which is more efficient and has lower emissions than conventional diesel-powered solutions for the cold chain

Watch companies like New Leaf and Yotuh closely—these innovations are addressing a critical challenge (food & pharmaceutical stability) during a time when global temperatures are rising consistently, and much of the Global South is left under-addressed by incumbent cold chain solutions. These types of local solutions developed for the Indian market have high applicability in Southeast Asia, South America, and Africa as well.

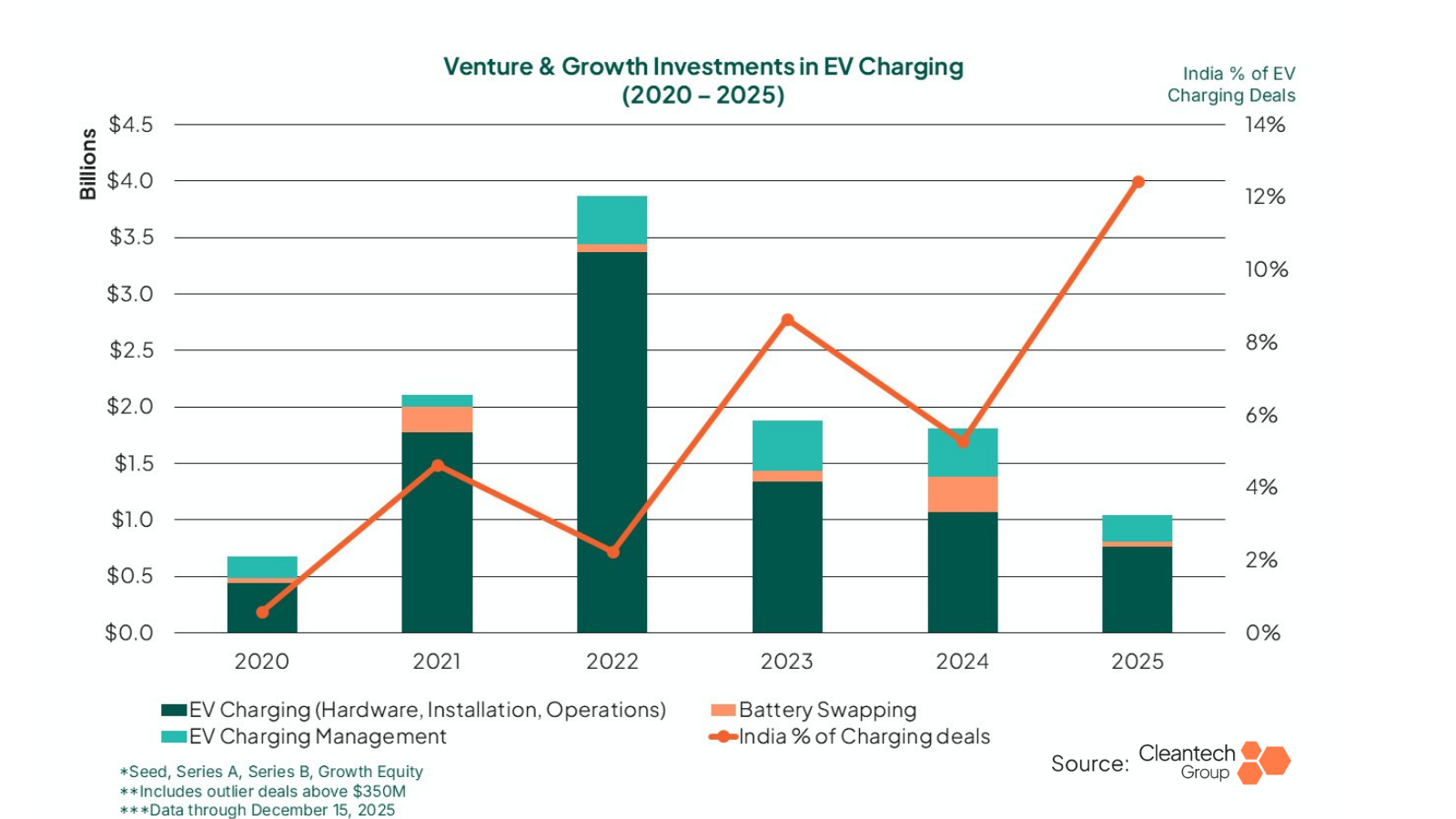

India is also in a position to take leadership on South-to-South tech transfer potential in EV charging. As can be seen from the chart below, EV charging has seen a drop-off in financing globally this past year, but this is mostly attributable to the fact that the “winners” have already been ordained in the Western world. Indian innovation—uniquely tailored to India and other regions with high volumes of two- and three-wheel EVs—is not slowing down.

- Indian battery swapping innovator Battery Smart has rolled out swapping networks across the country. The swapping and battery-as-a-service model reduces costs for drivers up to 40%, addressing range anxiety and long charge times, and increases electric mobility uptake.

- VoltUp similarly focuses on Battery-as-a-Service (BaaS) through a battery-swapping network, allowing 2W and 3W drivers to swap a depleted battery for a fully charged one in under two minutes at partner fuel stations (like BPCL), essentially eliminating charging wait times.

- Bolt.Earth operates an “Airbnb-style” decentralized network where individuals, apartment complexes, and shops can host their own charging points and earn revenue. It is currently India’s largest charging network, prioritizing high-density, low-cost AC charging points for two and three-wheelers in places where people live and work.

- Kazam acts primarily as a sophisticated software-as-a-service (SaaS) and energy management platform for enterprises. Partnering with major OEMs (like Bajaj and TVS) and fleet operators to manage large-scale charging infrastructure, providing the tech stack that monitors vehicle downtime and energy loads for commercial fleets.

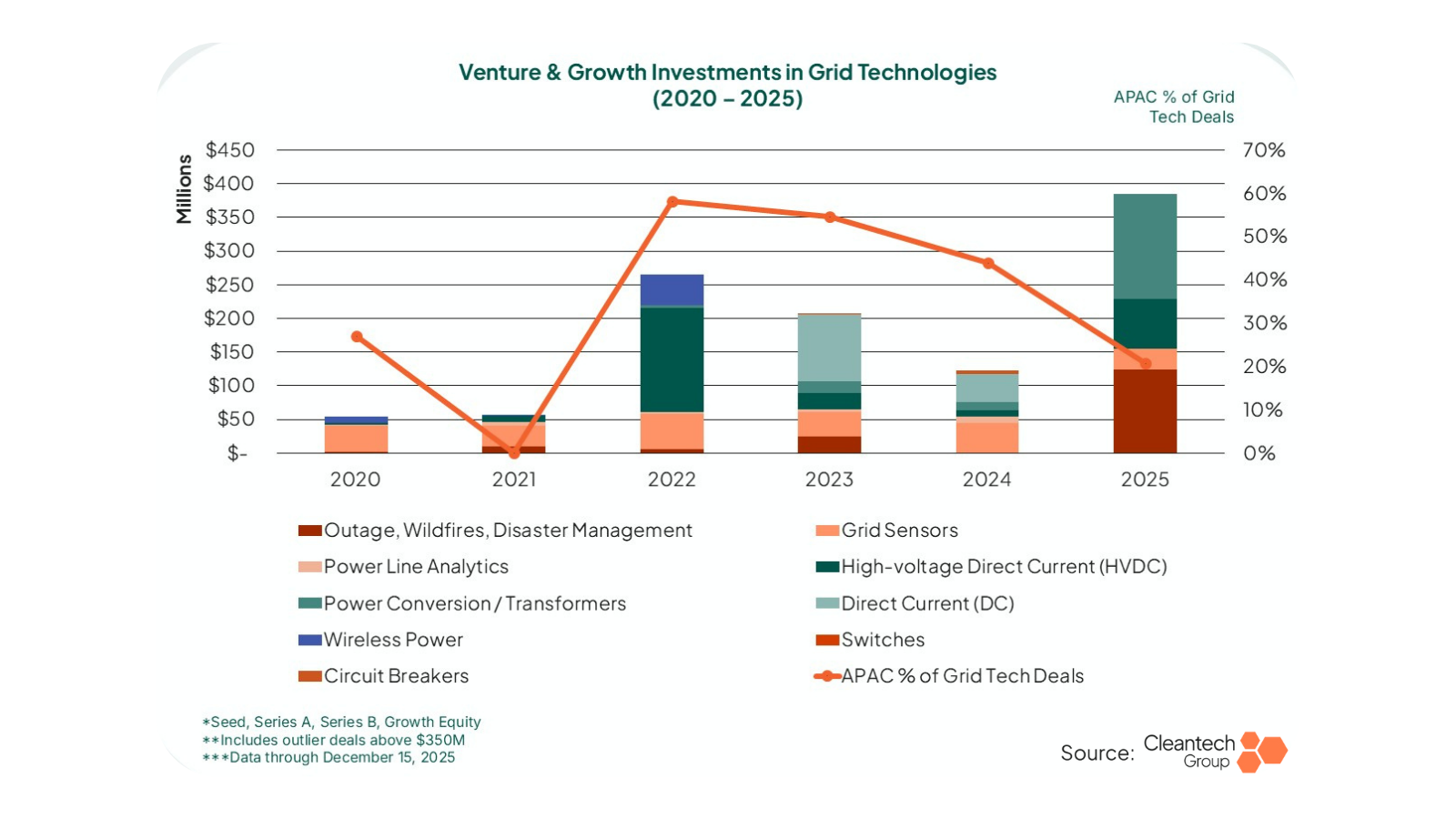

Watch Grid Upgrades Across APAC to Spot New Global Competitors

The best test of a new technology is to perform in a real-life environment. APAC is, in some pockets, seeing demand outpace supply, and new technologies are being pulled into real projects on a schedule ahead of the rest of the world.

Australia is expecting to require an additional 10,000km of new transmission lines to connect to new generation sources, to enable AEMO’s ambitious net-zero by 2050 plans. The urgency creates an opportunity for innovators to smooth the frictions of rapid grid expansion in Australia and then look to export markets where many countries are racing to catch power supply up to data center demand.

- Neara is an Australian innovator offering physics-enabled digital twins to model grid buildouts and plan against potential weather disruptions

- Global Cleantech 100 awardee Infravision is accelerating the time it takes to deploy new grid infrastructure by stringing transmission cables by drone

Singapore is becoming a living lab in constrained optimization for net zero. Singapore’s target for net zero by 2050, on a grid that is mostly gas-powered today, represents an opportunity for technologies that support energy efficiency to see ahead-of-schedule de-risking in real projects. This is observable immediately when looking at technologies piloted in Singapore that can be applied to data centers globally.

- Solid state transformer innovator Amperesand saw early deployments at Singapore’s port, and, after a series of fundraising rounds has now scaled operations to the U.S.

- Firmus Technologies deployed its liquid immersion cooling “Hypercube” at a data center in Singapore, and after proving out results, is now prepping Project Southgate in Australia, with over $300M raised for the effort so far.

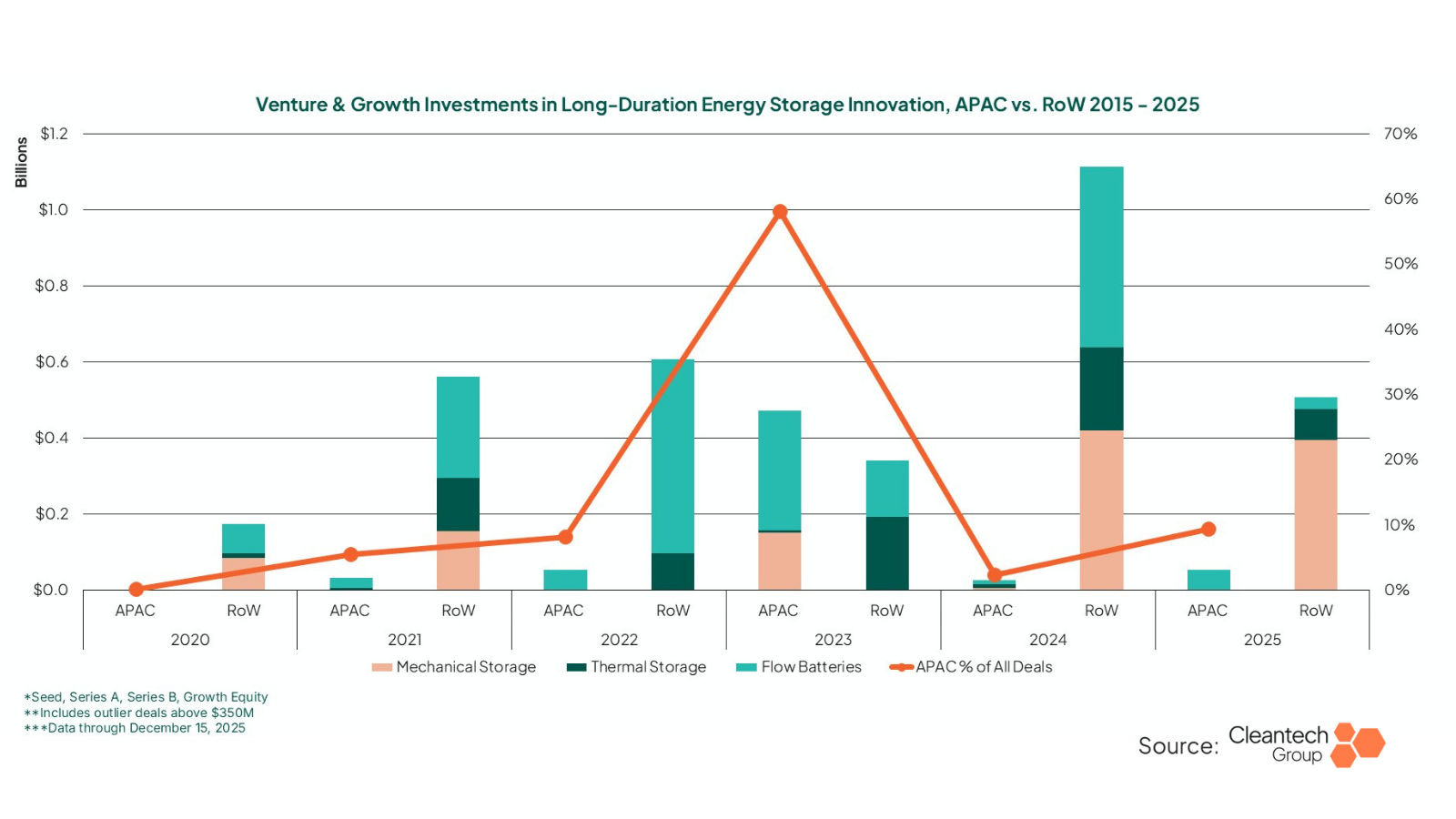

Long-Duration Storage – Can APAC Rebound while the U.S. Pulls Back?

While the United States was for a few years hurdling ahead in both technological breakthroughs and rapid entry into demonstration for long-duration storage (LDES) technologies, the pullback of Office of Clean Energy Demonstration grants, coupled with cancelled tax credits for renewables, has put a chilling effect on the space. The U.S. leaders are still performing, and some are finding projects in Europe as well.

Asia Pacific, however, feels both a fertile landing ground (given deep renewables penetration in places like China and Australia), but also a potential source of the next wave of LDES technologies.

Vanadium flow batteries have been the focus of LDES medium in APAC for some time, with more regional access to vanadium, and clearer demand signals from grids with high renewables penetration. Dalian Rongke remains the incumbent in the space in APAC, but innovators are entering the frame around APAC.

Singapore-based VFlowTech is undertaking regional expansion at a rapid clip, growing in both battery deployments and establishing supply chains (see 2025 partnership in India to recover vanadium from mining waste). VFlowTech is differentiating itself from competitors partially in its hybrid vanadium lithium-ion offering: this hybrid formulation allows customers to optimize for shorter storage with the lithium-ion part of the battery and hold charges for longer durations with the vanadium portion, when necessary.

Korean vanadium flow innovator H2 raised $16M to scale manufacturing from 330 MWh to 1,200 MWh. H2 also has international growth traction, including an October 2025 deal to sell vanadium flow batteries to a series of commercial buildings in Australia.