Fervo Energy began trading on Nasdaq under the ticker FRVO on May 13, 2026, after pricing its IPO at $27 per share. The deal raised $1.89B in gross proceeds on 70 million shares, implying a fully-diluted valuation of roughly $7.65B. Shares opened around $35, approximately 30% above the IPO price, implying an open-day market capitalization near $10B. That represents roughly 3.5x the $2.86B post-money valuation set by the December 2025 Series E, in five months.

The Strategy: De-Risk Through Iteration

Fervo took dead aim at total cost of delivery by avoiding the temptation to get too innovative in the tech stack. Instead of custom technologies, the company relied on proven fracking and power generation, focusing on iterating through projects to generate learning effects. The strategy: leveraging familiar tools to de-risk unfamiliar geologies.

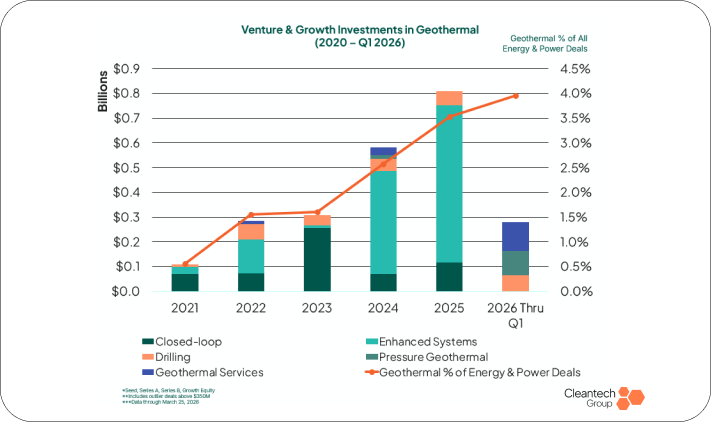

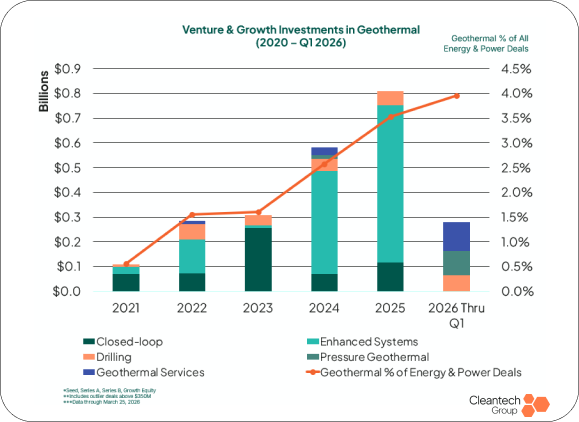

The IPO timing is significant. Geothermal has never been more prevalent in cleantech. Coming off 2025 with record equity financing, geothermal comprised a higher percentage of energy and power deals in Q1 2026 than ever before.

The Financial Case

The financials, on their face, are not a power-company story: $138,000 of 2025 revenue against a $58M net loss. The bull case sits in the $7.2B of long-term contracted revenue Fervo cites, the 500 MW under construction at Cape Station, and a credible learning curve from $7,000 per kilowatt today toward a $3,000 per kilowatt Nth-of-a-kind target.

The mainstream now understands geothermal’s promise and sees Fervo as a front-to-back project developer, power producer, and technology clearing house. Fervo is being recognized as geothermal’s “West Point,” not as a utility.

Why Enhanced Geothermal Is Now Realistic

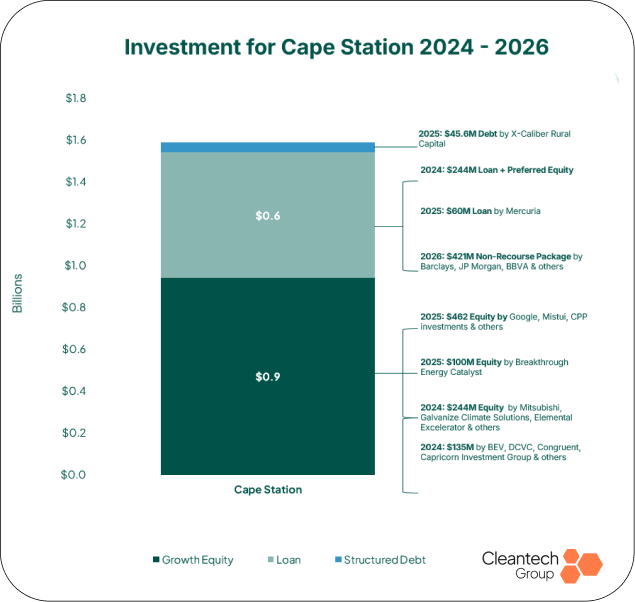

Fervo’s March 2026 $421M non-recourse facility, underwritten by RBC, Barclays, HSBC, and J.P. Morgan, marks the first time a top-tier syndicate has financed a first-of-a-kind EGS project at the project level without DOE Loan Programs Office backing. This credit decision changes the cost-of-capital math for every comparable developer, not just Fervo. The facility is non-dilutive and held off Fervo’s balance sheet, insulating the equity story from any project-level delay or cost overrun at Cape Station.

Fervo Energy $421M Debt Financing

Fervo closed a record $421M non-recourse debt round for Cape Station Phase 1, backed by nine major banks. The key: de-risking EGS by using proven oil and gas drilling techniques, making it bankable to traditional lenders.

Proof points: PPAs with Google, Southern California Edison, and Shell; Project Red’s 3.5MW with zero thermal decline; Cape Station’s per-well costs halved to $4.8M.

Why it worked: Non-recourse financing lowers capital costs. Banks fund proven economics, not unproven tech. Fervo’s strategy—public proof points, economics first, bankable risk models—sets the playbook for hard-tech scaling.

The Geothermal Framework Agreement signed with Google Energy on March 19, 2026 is the structure other hyperscalers will copy. It is also the most concentrated single-customer risk in the prospectus: the upcoming approximately 3 GW Google buildout is non-binding and audited at each stage. Google holds right of first refusal on any newly developed Fervo capacity through March 2028, potentially limiting Fervo’s ability to diversify its hyperscaler customer base during the critical near-term scale-up window.

Between 2019 and 2021, Fervo acquired a 595,900-acre subsurface land position at roughly $4 per acre. With EGS now bankable and hyperscaler demand pulling forward, that land is now a strategic moat newer entrants will struggle to replicate.

The Journey to $3,000 per Kilowatt

Between Project Red (2023) and ongoing Cape Station construction, drilling speed has improved roughly 70%, and well costs have fallen close to 75%. The IEA estimates Fervo’s drilling at approximately 30 meters per hour for parts of Cape Station, on par with mature shale.

Drilling costs have historically been one of the crucial bottlenecks in geothermal project development, raising the stakes for each well and risking financier confidence after false starts.

Cape Station’s first 500 MW is under construction with first power expected in late 2026 and approximately 100 MW operational by early 2027. An additional 1.5 GW is permitted at the same site.

The “GeoCluster” model described in Fervo’s S-1 is built around standard 50 MW Organic Rankine Cycle units and is explicitly a manufacturing-style learning curve, not a bespoke power-plant model. The model leverages already-available technology for power generation and avoids custom build-outs. It is an exercise in de-risking the modular approach, not de-risking the underlying technologies.

FervoFlex: A New Layer

FervoFlex adds another layer to the Fervo value proposition. Under testing at Cape Station, FervoFlex closes the production well and continues injecting, storing fluid in the granite reservoir. The pressure created by the mismatch between injection and production during the “charging” phase serves as an accelerant when “discharging,” creating a fast flow to increase power output and potentially counteract parasitic load.

If it works at scale, every EGS project becomes a long-duration energy storage asset. As promising as FervoFlex is, it will face stiff competition from LDES mediums that have received recent market validation, including Form Energy’s recent agreement with Google and Noon Energy’s with Meta.

Risks to Watch

The journey to $3,000 per kilowatt, and indeed maintaining $7,000 per kilowatt, has a number of uncertainties. The S-1 acknowledges the right risks to watch.

The Google relationship presents a potential single point of failure. While validating, it concentrates commercial fate in a single counterparty with structural audit rights.

Flow rates from a fully engineered reservoir are not yet demonstrated over multi-year operation. Lower-than-expected flow translates directly to heat loss and degraded plant economics. The S-1 notes the risk: decreases in heat-in-place reservoir temperature or sustainable flow rates over time, including as a result of thermal drawdown, changes in fracture conductivity, short-circuiting, permeability loss, scaling, or lower-than-expected recovery factors.

Induced seismicity is acknowledged as both an operational and a perception risk. A true seismic event would likely exceed the company’s ability to financially support a solution. However unlikely, public perception and resulting regulation pose the more likely obstacle. The S-1 states: “If regulators impose additional restrictions, monitoring, or permitting conditions specific to EGS stimulation and injection, our ability to develop or operate projects could be delayed, constrained, or made more costly. Public opposition to perceived or real seismic risks could also raise permitting hurdles and community engagement costs.”

What It Means for Geothermal at Large

Fervo’s IPO provides a validating case for geothermal as a category. Mainstreaming the concept and associated business models will carve a path for other geothermal companies.

The Full Picture Is Members-Only

Members get the complete analysis. Unlock the full picture—the insights, data, and connections that will guide your next move.