Geologic, or “white” hydrogen, has been one of cleantech’s most hotly debated storylines for the better part of a decade. The pitch is seductive: hydrogen forming naturally underground, carbon-free, potentially at costs below $1/kg. That’s a price point that would unlock mass adoption across fertilizers, steel, shipping, and power generation in a way that green hydrogen, still ranging from $4–$12/kg in most markets, simply cannot. The global hydrogen market is projected to hit $1T by 2050. Whoever cracks low-cost, clean supply at scale wins a very large prize.

The problem? You don’t know if the hydrogen is there until you drill. And drilling is expensive. And even then, you might not find anything.

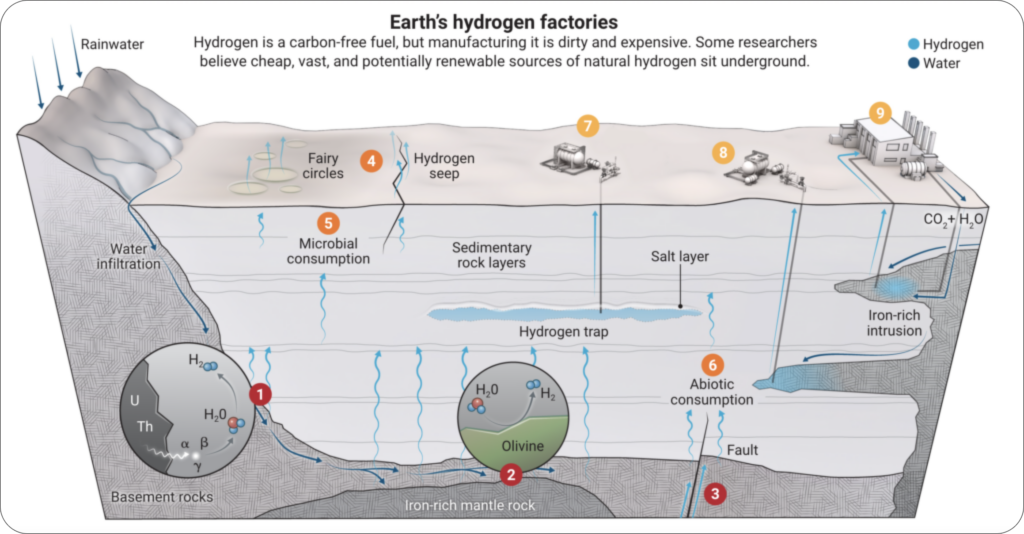

Source: (GRAPHIC) C. BICKEL/SCIENCE; (DATA) GEOFFREY ELLIS/USGS

Schrödinger’s Hydrogen

Natural geologic hydrogen is, in a very real sense, Schrödinger’s hydrogen. The resource simultaneously exists and doesn’t exist until you open the box, meaning you put a drill bit in the ground and see what comes out. Unlike oil and gas, where decades of seismic science give operators decent confidence before they drill, hydrogen exploration lacks a validated playbook. Subsurface accumulations require a rare alignment of source rock, migration pathways, a suitable trap, and an impermeable seal. And even when all of that lines up, microbial activity in shallow reservoirs can consume up to 90% of the hydrogen before it ever reaches a wellhead.

The sector’s sole commercial data point remains Hydroma’s well in Bourakébougou, Mali, which has powered a local village with 98%-pure hydrogen since 2011. A remarkable proof of concept, and also a sample size of one.

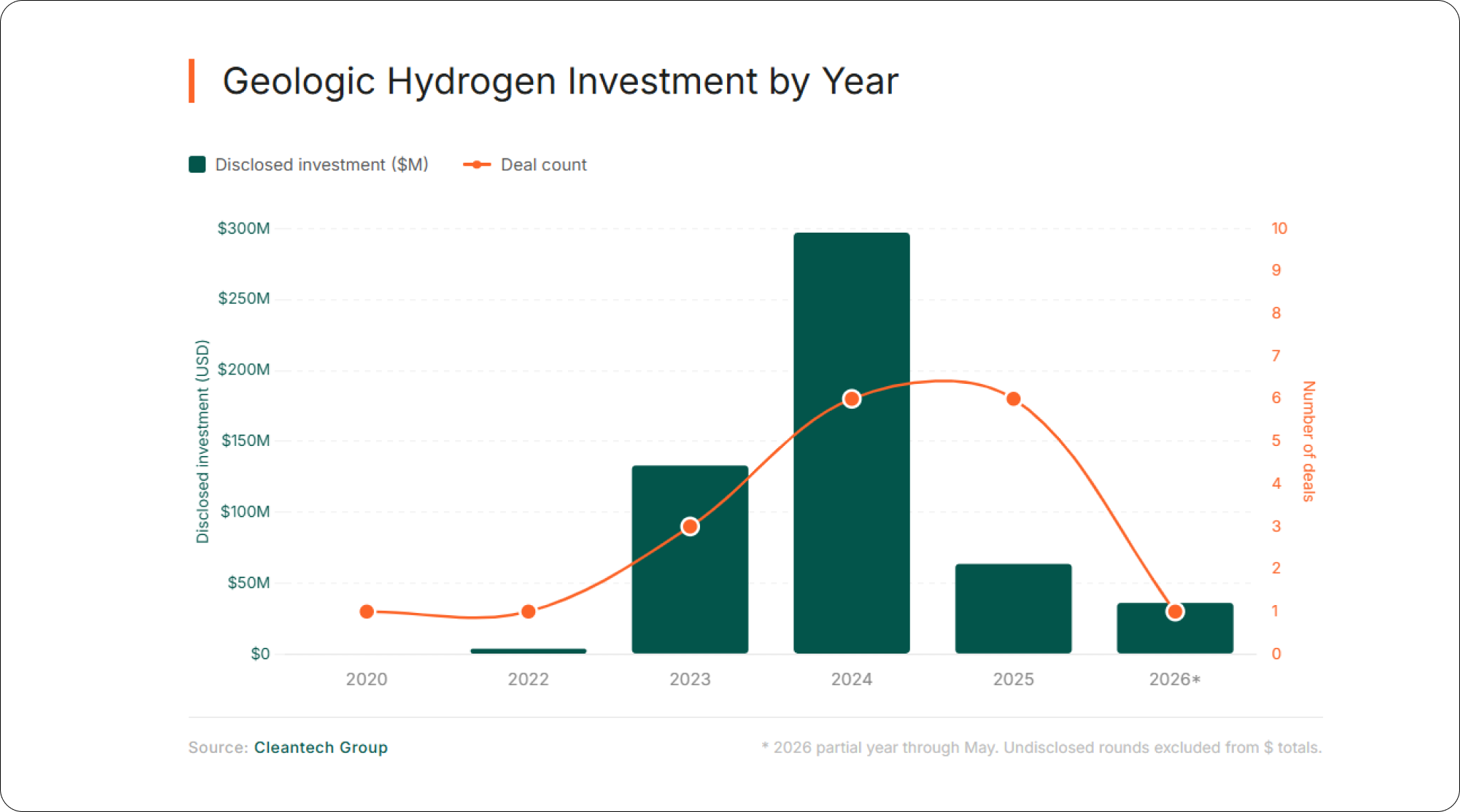

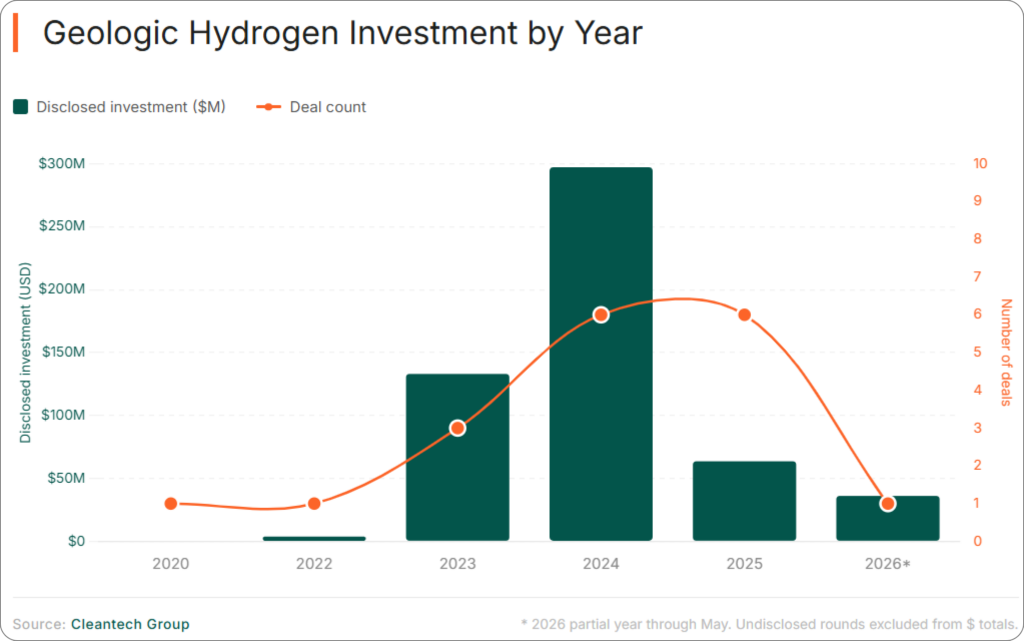

None of this has stopped capital from flowing. The natural hydrogen space has attracted over $500M in venture investment with essentially no commercial production to show for it, and the money keeps coming. Denver-based Koloma has raised nearly $400M, including a $245.7M round in February 2024 and a further $52.4M in October of that year, backed by Bill Gates’ Breakthrough Energy Ventures, Amazon’s Climate Pledge Fund, Khosla Ventures, and Mitsubishi Heavy. Despite the war chest, the company has been notably quiet following its test drilling program, declining to comment on production well plans or exploration locations. UK-based Snowfox Discovery, a spinout from Durham and Oxford Universities backed by BP Ventures and Rio Tinto Ventures, closed an oversubscribed $30M Series A in early 2025. French exploration company Mantle8 followed with a roughly $34M Series A in May 2026, bringing its total raise to around $44M. The round, backed by Breakthrough Energy Ventures and Bpifrance, will fund what the company calls the world’s most advanced natural hydrogen exploration and drilling campaign. The company’s chairman put it plainly: the next two years are about proving that what their technology has pinpointed can actually deliver sustained, commercially viable flow.

That’s still a box waiting to be opened.

If You Can’t Find It, Make It

A small but growing cohort of companies has drawn a different conclusion from natural hydrogen’s exploration challenges: stop looking for what the Earth already made, and trigger the same reactions yourself.

Engineered, or stimulated, geologic hydrogen works from the same underlying chemistry, primarily serpentinization, where water reacts with iron-rich olivine rock to release H₂. The difference is that instead of searching for where nature ran this reaction over millions of years, developers select suitable rock formations that are globally distributed and well-mapped, then deliberately accelerate the process using heat, catalysts, or electrical stimulation.

A few commercial approaches have emerged, each attacking the problem differently. GeoKiln uses downhole electrical heaters derived from Shell’s legacy in-situ oil upgrade technology, raising formation temperatures to trigger serpentinization on demand. Vema Hydrogen injects proprietary catalysts with water into ophiolite and banded iron formation rock, removing the need for continuous energy input once the reaction is underway, and has already drilled pilot wells in Quebec as of February 2026. Addis Energy goes a step further, targeting subsurface ammonia rather than hydrogen by injecting nitrate-source water alongside catalysts, aiming to skip the hydrogen handling challenge entirely by producing a product that plugs directly into existing fertilizer and maritime fuel infrastructure. Eden GeoPower takes the most distinct approach of the group, applying high-voltage electrical currents to fracture iron-rich rock and raise local temperatures simultaneously, creating the permeability and thermal conditions needed for the serpentinization reaction to proceed, with ARPA-E-funded pilots underway on peridotite formations in Oman.

Risky Business

Engineered hydrogen doesn’t eliminate risk. It relocates it.

The exploration risk of “is there hydrogen here?” is replaced by the engineering risk of “can we actually produce hydrogen at commercial rates, purity, and cost from this rock?” Reactions that naturally unfold over geological timescales must be compressed into months. The subsurface is opaque. Lab results have consistently failed to replicate cleanly at field scale across energy technologies. Iron-bearing minerals are consumed in the process, making well life and depletion rates unknown territory. And the produced gas is rarely pure hydrogen, meaning purification at surface adds cost and complexity. No engineered subsurface hydrogen project has reached commercial production anywhere in the world. Every cost claim in this space is self-reported and pre-field-validation, and should be treated as lab-scale projection until pilot results say otherwise.

Fancy Placing a Bet?

If any of these approaches works at scale, it would represent one of the more significant energy discoveries in a generation. In the near term, hydrogen demand will continue to be dominated by the industrial sector, specifically refineries, ammonia plants, and chemical processors that collectively represent a $100B+ market and require no infrastructure changes on the customer side. That’s the ultimate landing zone, but it’s one already dominated by grey hydrogen from steam methane reforming and coal gasification: cheap, carbon-intensive, and deeply entrenched.

The more interesting longer-term opportunity may lie with a different class of buyer: energy-hungry operators who need reliable, high-volume power without grid dependence or fossil fuel exposure. Data centers facing structural electricity constraints, green steel producers who need consistent feedstock to displace coking coal, and maritime shipping companies searching for a viable path to decarbonization are all staring at the same problem. They need baseload clean energy that today’s infrastructure simply cannot reliably or affordably deliver. Below-$1/kg geologic hydrogen, produced at or near the point of demand using publicly mapped geology, is one of the few proposed solutions that could plausibly serve all three without requiring a new continent of renewable power infrastructure to back it up.

The next 12–24 months are decisive. Pilot well results from Vema in Quebec, GeoKiln in Kansas, and Addis’s first field deployment will determine whether the engineering thesis has legs. On the natural side, Koloma’s next move, Snowfox’s exploration results, and Mantle8’s drilling campaign will test whether the exploration thesis is any closer to commercial reality than it was when the first hundreds of millions went in. If any of them deliver, expect a significant rerating of the entire sector. If they don’t, the conversation about whether geologic hydrogen is energy’s next frontier or an elaborate exercise in geological optimism will get considerably louder.

For now, the cat is still in the box, but that doesn’t mean you should take your eyes off it.

Get in touch to explore what else we’re exploring across the Energy & Power landscape at our upcoming forums.