Last year, as we published the Cleantech 50 to Watch, the world stood on the edge of a U.S. presidential election, and with it, a great deal of uncertainty about the direction of policy and investment. A year on, that uncertainty has evolved into something more tangible. Tariff reshuffling, the One Big Beautiful Bill Act, and renewed push back on renewable energy development, have created both drag and opportunity.

We’re seeing project timelines stretch even as demand for solutions intensifies. Innovation is pressing forward, but in a more uneven landscape.

At the start of 2025, we introduced our Grow, Flow, and Slow framework to describe what we expected to accelerate, progress steadily, or face headwinds in the year ahead. As the months have unfolded, we’ve been revisiting and revising that framework constantly as the world changes quickly around us.

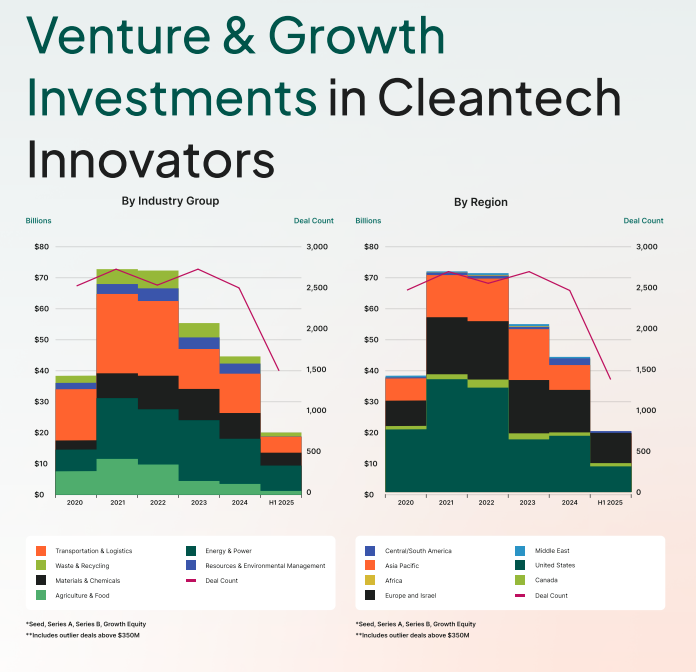

Investment patterns tell an important part of this story. Despite expectations of a sharp downturn in Energy & Power–particularly in the U.S.–the reality has been more of a reshuffling than a retreat.

Top-line funding numbers can be misleading, but the composition of that capital is shifting in fascinating ways. As shown in the charts below, venture and growth investment remain resilient across most regions, even as deal counts flatten. The innovators breaking through now are not necessarily in familiar categories, and the Cleantech 50 to Watch offers a strong signal of where the next wave is emerging.

Energy Efficient Compute–The Next Frontier in AI Efficiency

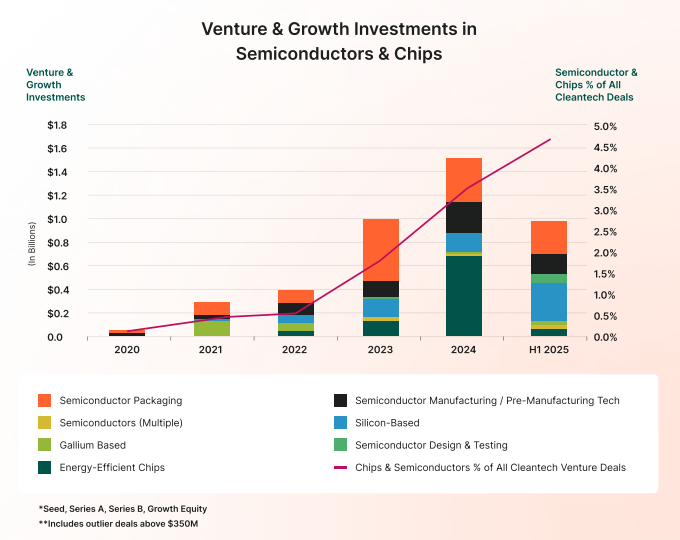

If AI was last year’s buzzword, in 2025 it’s become a language unto itself. We’re now seeing a complete ecosystem forming around all facets of energy use reduction to accommodate the many form factors and use case of AI in cleantech. Energy-efficient computing, often an afterthought in cleantech and climate discussions, is ripe for innovation from semiconductor materials to rack-level power management.

The data bears it out: as shown below, venture investment in chips and semiconductors has risen sharply since 2023. But what’s really exciting is the variety of innovation. Read further below to see instructive cases from this year’s Cleantech 50 to Watch.

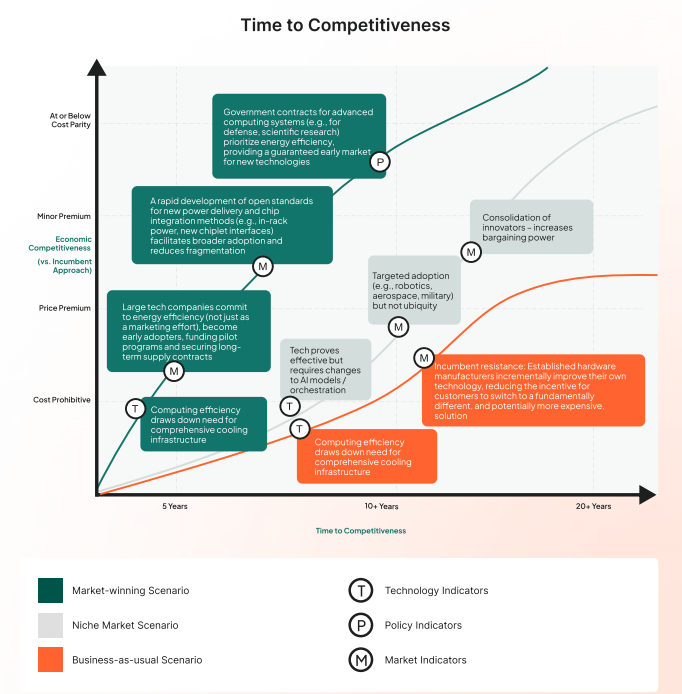

The investment numbers certainly reflect a growing faith that these types of companies will be a source of growth in the future, but the true indicator will be earlier-than-anticipated corporate adoption. While many of these technologies have strong OPEX reduction credentials, the sticker prices are likely to remain high until manufacturing economies of scale are achieved. However, operating in what today is a price inelastic market is a window of opportunity, that, if seized, could accelerate the trajectory to cost parity of the energy-efficient compute stack.

This year’s Cleantech 50 to Watch features more companies innovating in compute efficiency than ever before. What’s striking here is not only the emergence of this trend, but that there are a variety of solutions landing on the list-–from the furthest upstream of materials for semiconductors all the way to software and power management at the rack level.

- Gallox Semiconductors: Gallox’s Gallium Oxide devices will first be adopted in mission-critical applications where a 3x efficiency gain over silicon carbide warrants a price premium (think high-speed EV charging, solid-state transformers for the power grid). The largest opportunity for Gallox will be where it can perfect the gallium oxide manufacturing process to outpace silicon carbide and gallium nitride on scale and cost.

- SEMRON: SEMRON will first become cost-competitive in the high-value edge AI market. Think of applications in smartphones, VR/AR headsets, and autonomous systems where running generative AI locally is a competitive advantage. If manufacturing achieves scale and the costs per compute-unit fall, SEMRON chips have the opportunity to become cost-competitive for a wider range of edge devices, e.g., industrial IoT and consumer electronics.

- Neuralwatt: Neuralwatt’s core value proposition is immediate and compelling. It’s a software layer that optimizes power management for GPUs in data centers, requiring zero code changes to AI models or orchestration systems. This means customers can deploy it immediately to get a direct and measurable return on investment (ROI) by lowering energy costs and reducing carbon emissions.

- Palanquin Power: Palanquin’s focus is on the entire rack-level power delivery system, not just individual components. Their series-connected architecture allows for the use of cheaper, denser converters while maintaining high efficiency. As with other companies in the space, velocity of data center customer acquisition, within this high-demand environment, will be the deciding factor.

AI is a Force in Cleantech, and Not Just as a Software

As we have stated in previous analyses, the ability for AI to be an enabler in cleantech is being proven out in real time. While for many, the first inclination is to think of AI as being limited only to software, we indeed see a mix of solutions ranging from pure-play software to digital-physical intersects, and to AI as an underpinning driver of deep tech development.

Cases from this year’s Cleantech 50 to Watch indicate which industries are hungriest for the AI accelerant:

- Materials Discovery: Entalpic is a generative AI platform that accelerates materials and chemistry R&D by designing new molecules and materials from scratch. Scaling requires overcoming computational and physical bottlenecks in material discovery, which they address by creating a “flywheel” where the AI learns from continuous feedback and data.

- Agentic Factories: JunaAI‘s technology uses a multi-agent reinforcement learning platform to autonomously control and optimize complex industrial systems, such as chemical plants and factories in real-time, improving with time and accumulation of processes run.

- Weather Modeling: Beyond Weather‘s AI-based weather modeling differs from incumbent technology, which primarily relies on Numerical Weather Prediction (NWP).

- While NWP models use supercomputers to solve complex physical equations and fluid dynamics (very reliable for near-term extreme weather), Beyond Weather leverages machine learning to identify patterns in vast datasets of historical and climate data to provide faster and more cost-effective forecasts that extend beyond the typical 14-day horizon of NWP models, focusing on long-range, sub-seasonal to seasonal predictions.

Note that the opportunity in weather modeling is not just attracting innovators to the space, but incumbents as well. Google Deepmind’s WeatherNext and Microsoft’s Aurora are examples of incumbents with large-scale infrastructure and high-powered AI models that are developing application-specific offerings to industry.

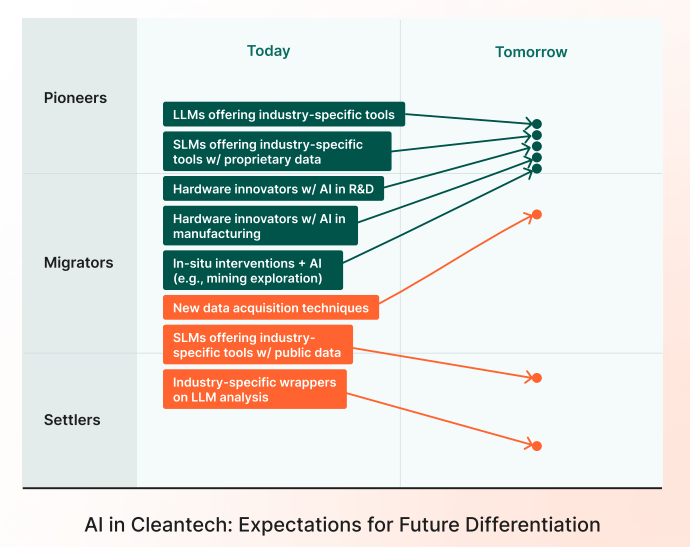

With all of this said, it is misrepresentative to view AI as a golden ticket to success in cleantech (in any space, really)-–many companies have ridden the wave of enthusiasm over the past few years, but we predict a meltaway of those without a distinct advantage.

Advantages for AI-enabled companies in cleantech will come from unique data acquisition and the ability to create differentiated outcomes in physical processes. And likely to the chagrin of many in the innovation space, the large tech companies developing generative AI capabilities will capitalize on the moment by launching industry-specific applications (e.g., the illustrations of weather modeling above, and also Google’s Firesat).

Crop Science – Quietly Making its Way into the Mainstream?

While 2025 has brought with it much controversy and debate around the world’s will to pursue climate mitigation strategies, the effects of changing weather patterns, pest migration, and disease evolution pose a systemic threat to the world’s food system. We have seen an expansion in recent years of crop science approaches, but the scientific challenges of developing a crop treatment and achieving on-farm adoption are daunting.

What has come through clear in this year’s Cleantech 50 to Watch is that the innovators in the space are taking full aim at improving crop yield as a primary value proposition, while also generating an emissions reduction, pollution reduction, or resilience benefit.

- IMIO creates regenerative, all-natural microbial inoculants to help farmers cultivate high-yield crops without chemicals.

- Qarbotech utilizes a patented biocompatible nanotechnology that enhances photosynthesis, leading to increased crop yields and improved fruit quality.

- NetZeroNitrogen has developed a non-GMO biofertilizer using endophytic nitrogen-fixing bacteria that colonize plants and reduces the need for synthetic fertilizers.

- Silvec Biologics is a biotechnology company developing a non-GMO, RNA-based vaccine to protect trees, vines, and bushes from harmful pathogens.

PAGE Technologies is an interesting enabler of the digital / physical intersect, re-inventing the sensors that go into soil and water measurement by employing particle-polymer inks so that sensors can be produced in a mass-scale roll-to-roll manufacturing process. This begs the question of where else are “entry points” for AI into the crop science space.

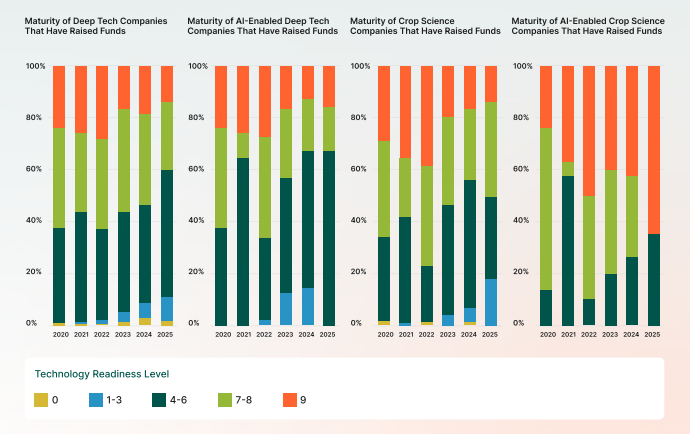

Interestingly, while crop science stands to be one of the biggest beneficiaries of the AI revolution (think gene editing and fertilizer development), we do not see the same acceleration effect of AI on the ability of companies in the space to scale-–yet. In the graphic below, our data suggests that in deep tech at-large, usage of AI somewhere in the process is allowing younger, lower TRL companies to grow faster. The inverse is true for crop science companies, where the AI-enabled ones raising funds skew later-stage.

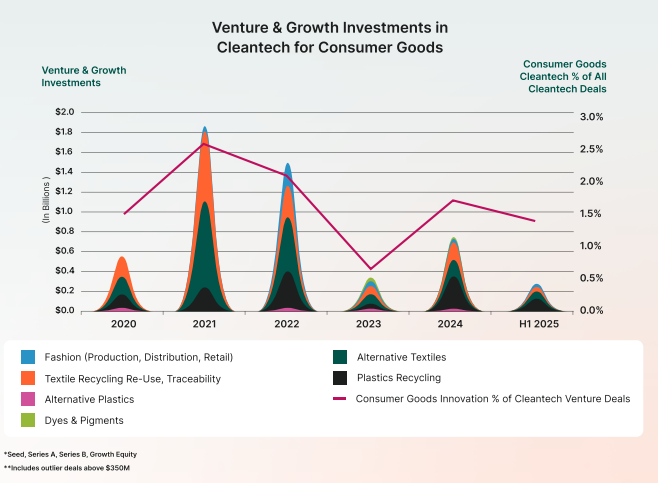

Consumer Goods Cleantech – Are We Finally at the Starting Line?

At the beginning of this year, we posited that with a macroeconomic downturn on the horizon, resource efficiency would be back in vogue. And while we have indeed seen activity on plastics and textiles happen in fits and starts over the years, the difficulties of feedstock management and low-cost valorization processes are daunting. Given the size of the problems, the mix of alternative solutions and circularity has never amounted to a significant percentage of the cleantech investment mix. Beyond the investment numbers, what gives us reason to believe that the 2025 Cleantech 50 to Watch indicates something new?

At least 8 companies on this year’s list are tackling consumer goods sustainability–from textile recycling (re.solution, Syntetica) and plastic recycling (Radical Dot, Driven Plastics, Extracthive) to the creation of bio-based materials from waste (Tomtex, Carbon Cell, Sengong). This focus on advanced recycling and novel materials is a direct response to the limitations of traditional mechanical recycling, which struggles with mixed and contaminated waste and often results in lower-quality products.

The innovators on this list are not simply addressing the “easy” waste; they are tackling the last-mile problem—the complex fiber blends, multi-layered plastics, and carbon fiber composites that have historically been unrecyclable. In addition, as both plastics and textile recycling innovators continue tackling the challenge of blended materials, there is likely to be an opportunity for collaboration and technology transfer.

The broader market for sustainable materials is substantial -with a projected value of over $800B by 2032-–but very geographically “pocketed” (think China and EU). Look for solutions that bring new production methods close to the demand markets. Take special note of Sengong, who has reported that their manufacturing process for PVA (Polyvinyl Alcohol), a material that can be used 50x over but is also water soluble, is near par cost with PET-based plastics. With a mature and at-scale manufacturing base at their fingertips, expect Sengong and other Chinese innovators in these spaces to become more prominent, fast.

Ecosystems

At the early stages of company development, the importance of ecosystems is being felt more acutely than ever. Since we began tracking the early-stage journeys of companies, we have seen a further “tightening” of ecosystem journeys, with this year’s Cleantech 50 to Watch demonstrating the most overlap we’ve ever observed in the list (i.e., multiple companies engaging the same ecosystem actors).

Note the prominence this year of regionally focused ecosystem actors such as SGInnovate (Singapore), Invest Nova Scotia and Nadarra Ventures (Canada), Sprin-D (Germany), and Innovate UK with a mandate to provide a springboard for local companies to succeed on the global stage. The corollary to the “push” ecosystem actors is the “pull”, focused on leveraging a given geography’s strengths to help companies land there and leverage local advantages. Massachusetts is clearly maintaining a position of strength as a place where cleantech companies can grow or land but generally need to be-–as seen in the results from the Massachusetts Clean Energy Center and Greentown Labs.

We extend our congratulations to all 50 companies receiving this award in 2025-–a year when innovators are tasked with pushing the limits of their respective fields, but also the global macro conditions.

Cleantech has never been more interdisciplinary, or more essential. The 2025 Cleantech 50 to Watch highlights innovators rewriting the rules of what’s possible in computing, agriculture, consumer goods, and resource management.

Their collective message is clear: progress in cleantech is no longer siloed. It’s systemic, data-driven, and global. The year ahead will test not only technologies but the ecosystems that sustain them.