The Problem with Current Financial Systems Are…

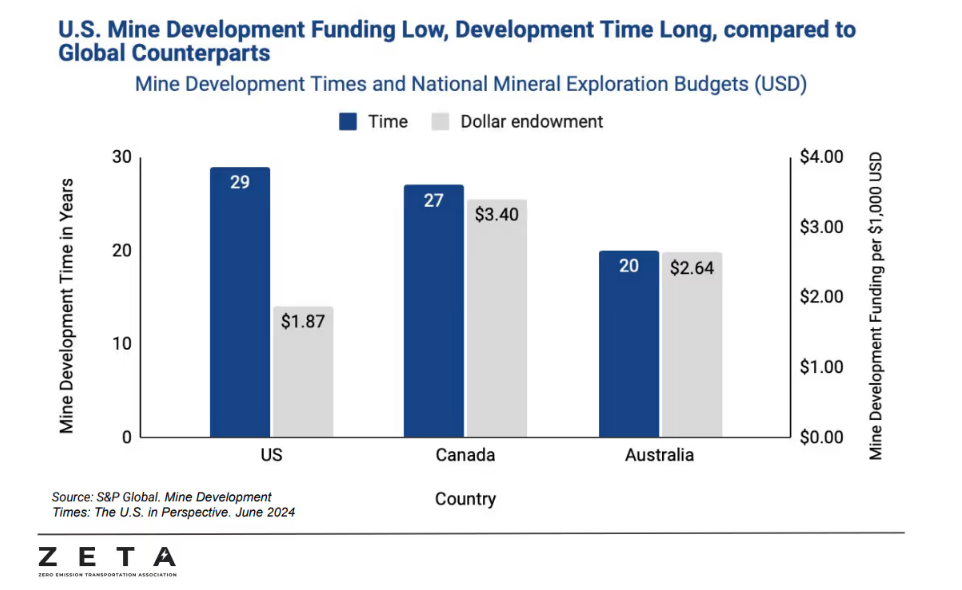

Current financial systems are a significant bottleneck—or even an active deterrent—to long-term climate strategy. Mining innovation is no different, with heavy infrastructure requirements for power, transport, logistics, etc. Many struggle to fit the traditional high-return, quick-exit venture capital model.

The typical pressure VCs face is to find a profitable company that returns the greatest possible return in the quickest time. VCs must identify a disruptive technology with potential to achieve a high-valuation exit (IPO/acquisition), ideally in no more than five years or so. This approach works for many cleantech solutions that have low CAPEX requirements and strong adoption readiness.

But what about the more advanced deeptech solutions with high CAPEX, large infrastructure requirements, and not quite mature market readiness? These might include solutions that we know must scale in the coming decades but do not have the strongest economics now.

Think mining, but also carbon capture, nuclear, recycling, etc. These solutions tend to have long development cycles and long-term returns in the 20-30+ year range. These present a huge deterrent and lower the potential for high, quick returns such that traditional finance structures won’t or simply cannot back them.

True, the complexity of funding requirements is immense. One must account for technology readiness level (TRL), funding stage, business model, CAPEX, infrastructure readiness, market demand, and more. However, in many cases, waiting will ultimately cost double, triple or even more at the pace we’re going (or lack thereof)—and that’s just monetary terms.

The good news is that critical mining projects are progressing, often bolstered by significant public sector funding. We’re also witnessing increasingly clear coordination between private and public sectors. And most excitingly, we’re seeing some innovators exploring unique financing structures and business models to bring these essential projects online.

Major Trend: Clear Private-Public Coordination

Critical minerals are perhaps the most important strategic area of opportunity as major tech companies move to secure supply independence in the wake of geopolitical shocks. The U.S. is coordinating by taking minority equity stakes in critical mining projects in addition to significantly contributing via blended finance structures. In addition, corporates are backing these projects by throwing their weight in finance and scale-up expertise.

July 2025

MP Materials, a producer of rare earth elements (REEs), struck a multi-billion-dollar commitment:

- $150M loan by the U.S. Department of Defense, purchase of $400M worth of shares (15% stake) & a 10-year offtake agreement

- Additional $500M PIPE commitment by tech-giant, Apple, to launch a recycling facility to produce rare earths from post-industrial scrap

- JPMorgan Chase and Goldman Sachs Bank to finance a whopping $1B to satisfy expansion goals

October 2025

Lithium Americas, a producer of lithium carbonate from hard rock, at its Thacker Pass Project in Nevada:

- The U.S. DOE acquired a 5% equity stake

- Committed additional $100M in equity and loan amendments

- Acquired additional 5% stake in Lithium Americas/General Motors JV

Trilogy Metals, a producer of copper, zinc, gold, and other valuable metals, at its Upper Kobuk Mineral Project in Alaksa:

- The U.S. Department of War committed $35.6M equity

- Acquired 10% stake

November 2025

Vulcan Elements, provider of rare earth magnet recovery technologies, raised over $1.4B through a blended finance structure. Funds will be used to support the expansion of 10,000 tons of production capacity to secure rare earth magnets for semiconductors and other critical technologies. This includes:

- $620M direct loan from the Department of War’s Office of Strategic Capital

- $550M in private capital

- $50M of federal incentives from the Department of Commerce under the CHIPS and Science Act

December 2025

Korea Zinc was set to sell $1.9B worth of shares or 10% stake to the U.S. government and private investors for its $7.4B Tennessee project to build an integrated smelter producing base metals and critical minerals. However, the move has resulted in opposition from its largest shareholders who have already moved to seek a court injunction that would block Korea Zinc from issuing these new shares.

In a recent LinkedIn article, Ashley Zumwalt-Forbes referred to the U.S. as quietly building a mineral sovereign wealth fund. This is essentially a state-owned investment fund that uses various capital sources to generate returns for taxpayers. But Zumwalt-Forbes warns that there is not nearly enough oversight nor transparency to declare these as innovative approaches to rebuilding domestic minerals capacity—but time will tell.

On the other side of the pond…

December 2025: Germany-based Vulcan Energy, a developer of lithium extraction projects from geothermal brines, raised over $2.56B to scale its Lionheart lithium project in Germany. Vulcan Energy is uniquely positioned to succeed with the colocation of geothermal power that aims to significantly reduce operational expenses with added power generation benefit for dual revenue. Its funding is consistent with industry projects on the order of billions of dollars and includes:

- $1.4B in senior debt from the European Investment Bank and the Export Credit Agency (ECA)

- $944M PIPE from KfW, HOCTIEF, Siemens Financial Services, and Demeter IM

- $237M grant from the Government of Germany

Crowdfunding—Once a Novelty Now a Legitimate Fundraising Tool

High capital costs and long fundraising cycles continue to slow progress, prompting some innovators to turn to an unconventional avenue: crowdfunding. This approach has been especially popular for junior minors, including those outside of the cleantech ecosystem. Still, it’s a growing trend being utilized to drive smaller, yet high-volume commitments as low as $500. This method has received positive public sentiment for those who view these as opportunities to become strategic players in a historically well-known gatekept industry. A few examples:

- 2023: UK-based Cornish Lithium crowdfunded $6.2M to extract lithium from geothermal brine projects

- 2024: UK-based Green Lithium crowdfunded over $1.7M Series A to support its first plant’s late-stage development phase for lithium refining

- 2024: Most impressively, U.S.-based EnergyX crowdfunded $75M to obtain ownership and rights over its own lithium projects without partnerships with miners

- 2025: UK-based Astra Mining launched a small campaign to raise over $370K for its broad minerals extraction portfolio, including rare earths, nickel, copper, and more

What’s to Come?

Looking forward, expect continued engagement by both the public and private sectors as corporates move to secure supplies of base metals and critical minerals. As evidenced by Apple and GM, we anticipate a wave of long-term offtake agreements and partnerships to bypass the volatile spot markets and insulate from geopolitical shocks. While these initiatives aim to boost mining, it’s heavily focused on extraction, particularly in North America.

A critical piece remains: what about refining?! More on that later…