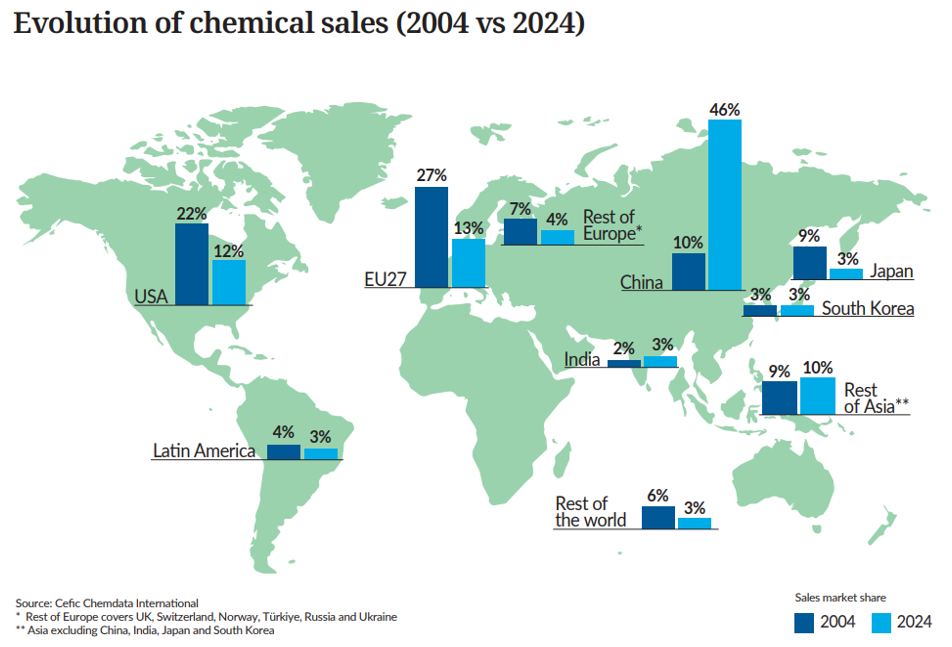

China Now Controls 46% of Global Chemical Sales

It got there the same way it took over solar, electric vehicles, and steel—state-directed capital, deliberate overcapacity, and sustained pricing pressure until competitors close. Ten of the world’s top 50 chemical companies are now Chinese. Wanhua Chemical, which barely existed in 2011, now generates revenue equivalent to roughly one-third of BASF’s. It’s still building.

On top of China flooding the base market, the closure of the Strait of Hormuz in February 2026 was a preview of systemic risk the entire industry has been ignoring. The Middle East supplies nearly half of global polyethylene exports, one-third of global sulfur trade, and the fertilizers that feed half the world—all flowing through a single chokepoint.

Europe Is the Clearest Casualty

Between 2022 and 2025, E.U. chemical plant closures grew six-fold by capacity, reaching 37 million metric tons permanently retired, or 9% of Europe’s entire output. The energy cost gap is the engine: European natural gas prices averaged two-and-a-half times U.S. prices throughout 2025, making European ethylene production twice as expensive as America’s and four times the Middle East’s.

- Dow closed three plants across Germany and Wales in 2025 and announced 4,500 job cuts in January 2026 after reporting a $657M loss.

- INEOS closed its allylics and chlorine plants in Rheinberg, Germany in October 2025, both producing inputs for defense and aerospace. Its CEO called European energy policy “industrial suicide.”

- Solvay shuttered plants in the U.K., Portugal, and Germany as part of $235M in cost reductions.

- BASF is preparing to spin off businesses representing 37% of its total sales.

Europe’s response has been to bet heavily on green hydrogen, and the logic is sound. Over $2.5B has flowed into hydrogen investment in the E.U. since 2016, and the infrastructure case for a northern European green hydrogen hub is genuine. But the sectors being decarbonized through hydrogen are not the sectors that are closing. Green hydrogen addresses ammonia, methanol, and refinery processes. The capacity draining away from Europe is in upstream petrochemicals, polymers, and basic inorganics. Europe may successfully build the world’s best green hydrogen network and still lose the downstream industry that was supposed to use it.

The most powerful tool available—extending CBAM to cover polymers, petrochemicals, and basic chemicals—would force Chinese imports to face the same carbon cost European producers pay without a cent of direct subsidy. It remains only partially deployed.

The U.S. Enters This Story With the Strongest Hand

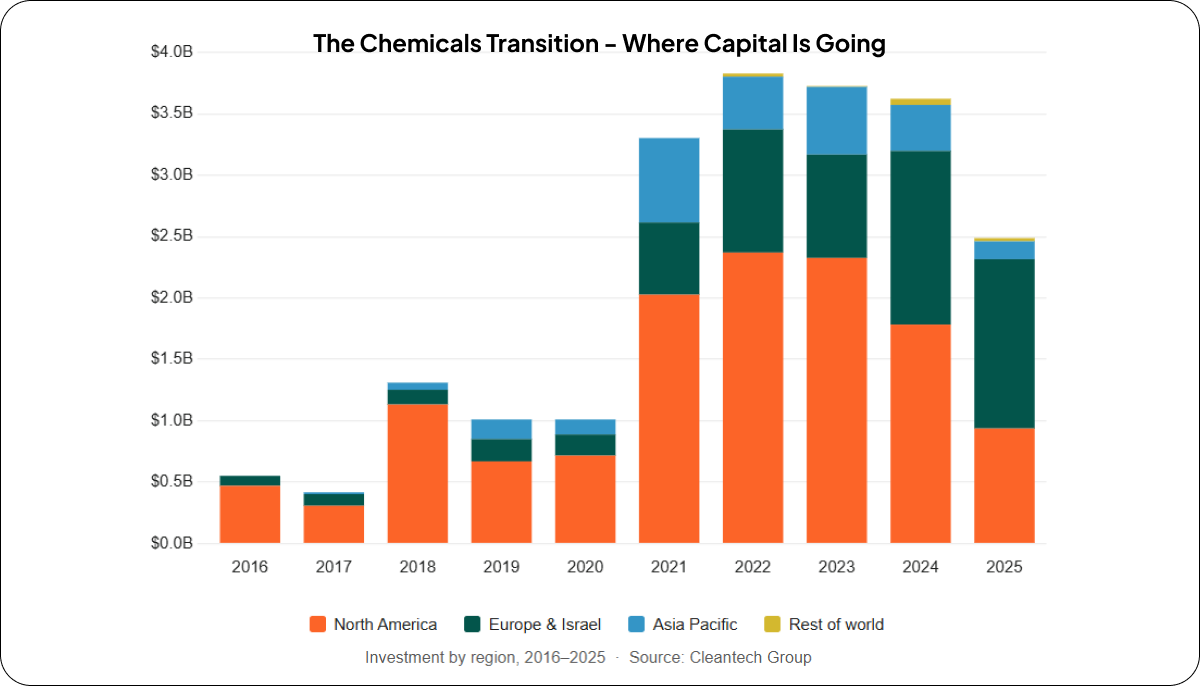

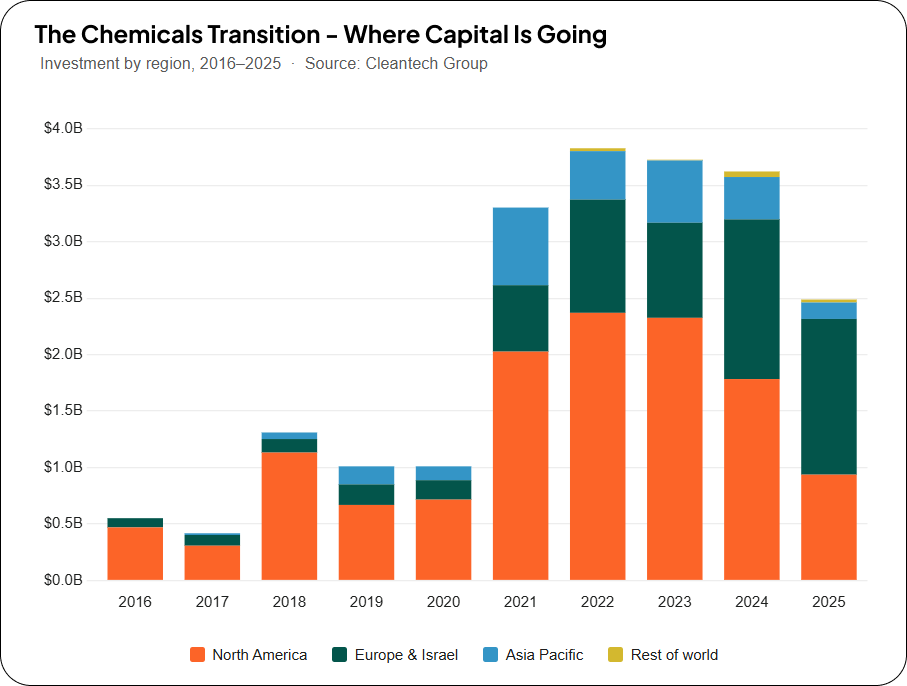

Cheap shale gas, a $200B Gulf Coast infrastructure base, and until recently the most coherent industrial policy framework in the IRA: but the advantage is slipping away. U.S. trade policy on chemicals has been in near-constant legal flux, with tariff regimes imposed, struck down, and reimposed in quick succession. The IRA’s $6B in industrial decarbonization grants and green hydrogen and CCUS credits—praised by non-U.S. chemical executives as a model for industrial policy—are being rolled back. Venture and growth equity investment in the chemicals transition peaked in North America in 2022 and has fallen 61% since. Capital raised is not the same as technology delivered, as Zymergen, Amyris, and Danimer Scientific all discovered after filing for Chapter 11.

The rest of APAC is also feeling the pressure. Japan is closing four ethylene crackers—nearly 30% of national capacity. Asahi Kasei’s president noted that Japan’s crackers have run below break-even utilization for 44 consecutive months. South Korea’s ten largest producers signed a government-brokered agreement in August 2025 to cut 25% of naphtha-cracking capacity, explicitly citing Chinese competition. South Korea’s agreement makes clear this is a global problem.

The Picture Isn’t Entirely Bleak

Chemical recycling—enzymatic depolymerization, gasification of complex waste streams—is advancing beyond the contested pyrolysis debate. Carbios is building the world’s first industrial-scale enzymatic PET depolymerization plant in France, operational by 2027–2028. Bio-based specialty chemicals are building commercial scale in Germany and the U.S., in segments where Chinese commodity competition is least relevant. Verbio and CropEnergies are both opening commercial-scale bio-based chemical facilities in Germany in 2026. In Texas, INEOS and Trillium Renewable Chemicals started up the world’s first demonstration plant for bio-based acrylonitrile in early 2025. AI-driven catalyst discovery is a long shot but a genuine one—Copernic Catalysts has already demonstrated an ammonia catalyst achieving twice the yield of competitors at milder conditions, potentially increasing plant capacity by 47% without new infrastructure.

But none of this keeps a cracker open that’s scheduled to shut next year. The world needs to wake up and smell the chemicals before there are none left to smell.