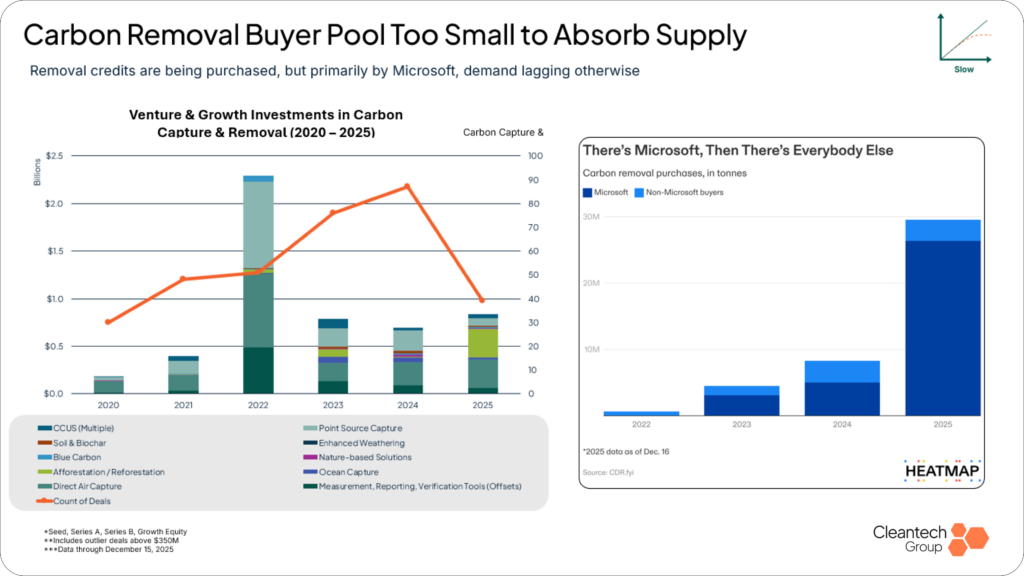

On April 10, Microsoft announced it would be pausing new purchases of carbon credits. This is the market’s majority buyer.

Even before Microsoft’s announcement, there were too many suppliers in the space and not enough demand to absorb them. We expect pivots, bankruptcies, and company shutdowns in this space to accelerate through the year.

The trend of major tech companies buying offsets was, in our view, always temporary. These companies are making advances in AI training efficiency and data center optimization that have material cost benefits, with some contracting large clean energy loads for energy supply stability. There are, in other words, emissions-reducing activities that are not primarily climate-motivated.

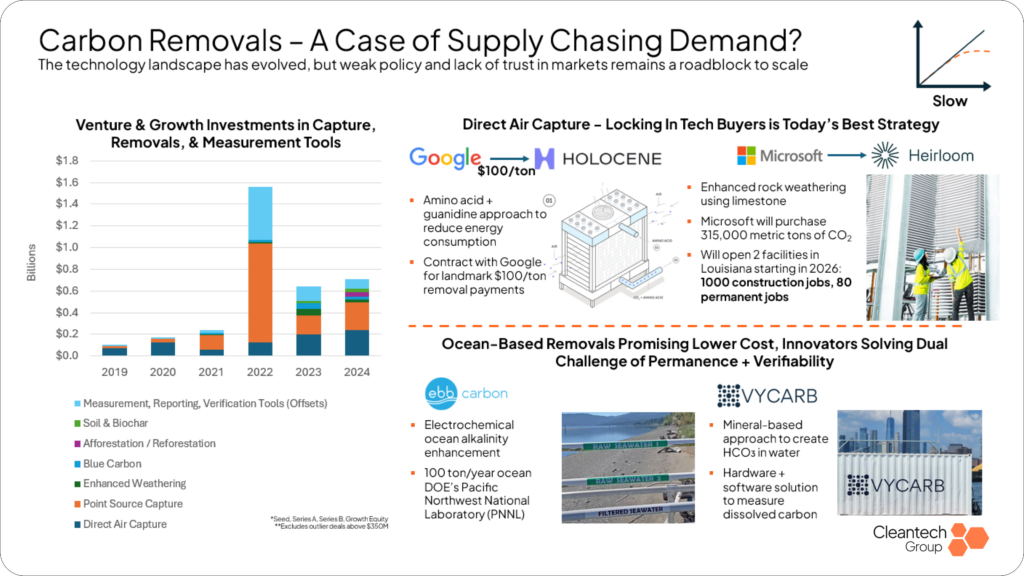

The removal models that remain viable going forward will have a clear case for co-benefits: a marketable product aside from carbon credits, though carbon credits may serve as a revenue layer on top. In the near term, direct air capture (DAC) and ocean-based removals are likely to suffer the most, while soil-based and biochar approaches can argue an agricultural yield increase.

We Called This in January 2025

We have stated since January 2025 that the carbon removals market, though at that time trending upward in terms of investments, was simply over-supplied, and that demand would not be strong enough to sustain the number of suppliers entering the space.

January 2025 prediction from Cleantech Group’s Annual Outlook Webinar

By the end of 2025, this was not bearing out in terms of investment dollars, but was in terms of deal count. As put forward in our 2026 annual outlook, the heavy concentration of purchases attributable to Microsoft was too much of a single point of failure in an already fragile sector.

January 2026 prediction from Cleantech Group’s Annual Outlook Webinar

(note: the two charts above use a different method—the first excludes deals >$350M)

Microsoft Was More Than a Buyer — It Was the Market’s Foundation

Microsoft, responsible for 80-90% of carbon removal purchases according to CDR.fyi, was the market’s pillar. It should not be overlooked that Microsoft’s involvement in carbon removals was more than a financial underpinning — it was perhaps the single most important contributor to the development of a common language and de facto standards in the space. The learnings from this wave of Microsoft purchases set a framework for any future revival. Nonetheless, without the market’s main customer purchasing, and with a low likelihood of a policy push in the U.S. to motivate more corporate offsetting, we expect this to accelerate what was already going to be a year of company failures in carbon removals.

It is unlikely that other large tech companies can step in to fill the void. A key underpinning of Microsoft’s motivation to purchase carbon credits was its intention to be carbon negative by 2030 and remove historical emissions by 2050 — a unique ambition. And while emissions in the U.S. are almost certain to rise in the near term from AI data centers, renewables, storage, and efficiency of AI operations are all going to be high-priority items for AI hyperscalers.

Recent major movements — including Microsoft’s power purchase agreement (PPA) with Constellation, which will partially reopen Three Mile Island, Google partnering with Form Energy for 30 gigawatt hours of storage in Minnesota, and Google’s claim of a 33x reduction in the energy cost of AI queries in one year — are all evidence of emissions-reducing activities more likely motivated by cost reduction and energy supply stability than climate.

The Full Picture Is Members-Only

Members get the complete analysis. Unlock the full picture—the insights, data, and connections that will guide your next move.