July 2, 2026 — Cleantech Group today released a new market intelligence report, Textiles Recycling, examining the technology, investment, and policy landscape for end-of-life textile processing. The report finds that textile-to-textile recycling rates remain under 1%, with only four textile-to-textile projects operating at meaningful capacity globally, and that closing that gap will require policy-driven demand signals, not just better technology.

Regulatory pressure, not voluntary corporate commitments, is the most powerful force for unlocking investment and adoption at scale. Two EU measures are landing in sequence: a ban on landfilling or incinerating unsold clothing and footwear takes effect this summer under the Ecodesign for Sustainable Products Regulation, and the revised Waste Framework Directive now requires every member state to establish textile Extended Producer Responsibility schemes, with national laws due by 2027 and programs running by 2028. France, whose Refashion scheme has operated since 2007, is furthest ahead. In the U.S., California has already passed the first textile EPR law, SB 707, and is now moving into implementation. Without equivalent mandates and fiscal mechanisms, voluntary recycling efforts will continue to fall short.

“Mechanical recycling is cheap and deployable today, but it can’t handle complex blends or return virgin-quality fiber. Chemical recycling can, but the economics haven’t worked yet and investors are burned. The industry needs both to scale together, and the only thing that will force that is regulation with teeth,”

-Buff Lopez, Associate, Materials & Chemicals, Cleantech Group

The report also highlights a structural tension at the heart of the market: investors believe downstream processing infrastructure must be established before upstream sorting and collection can scale, but without sortable, identified feedstocks, downstream economics remain unfavorable. Resolving this chicken-and-egg problem is the defining challenge for the sector over the next five years.

Core Findings

According to the report:

- Securing purity, not volume, is the bottleneck: Complex blends and mislabeled tags undermine downstream recycling across every technology pathway. Upstream sorting—increasingly enabled by AI-driven sensors and embedded traceability—is the most impactful near-term investment the industry can make.

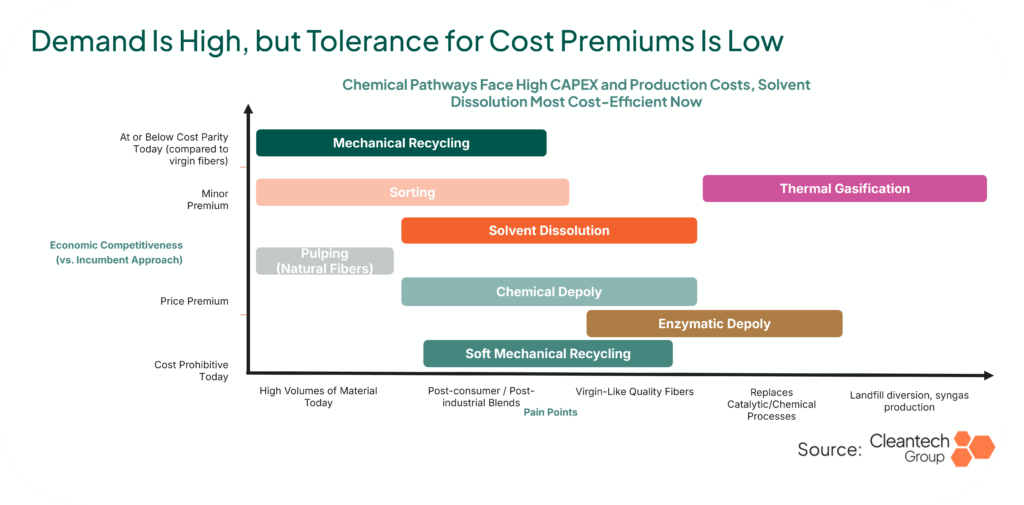

- Chemical recycling faces structural headwinds, with solvent dissolution the most promising near-term contender: Chemical depolymerization is capital-intensive and has produced high-profile failures including Circulose’s 2024 bankruptcy. Solvent dissolution is emerging as a cost-efficient alternative for processing complex blends, while enzymatic depolymerization remains early-stage but holds significant long-term potential for premium fiber recovery.

- No innovator has reached commercial scale, meaning cost-premium tolerance is still undetermined: The market accepts that some premium is necessary, but without long-term offtake agreements and plants with real operating histories, credible cost curves do not exist. Novel business models and flexible investor expectations will be required to bridge the gap.

The report concludes that the path to a functioning circular textile ecosystem runs through policy first, sorting second, and processing third. Voluntary recycling alone will not move the market. Mechanical recycling combined with advances in solvent dissolution could realistically double recycling rates by 2030—but only if the regulatory and fiscal environment forces the demand that justifies the capital.

About Cleantech Group

Cleantech® Group is the human intelligence authority on global cleantech innovation. Since 2002, we’ve helped decision-makers across industry, finance, and policy navigate the rapid shifts transforming the global economy.

Going beyond market intelligence—offering insights, strategic guidance, and curated connections to help leaders stay ahead, identify opportunities, and act with confidence. Our insight is built on over 20 years of human intelligence, proprietary data, and direct relationships with the ecosystem leaders driving change.