As conflict escalates in the Middle East and the Strait of Hormuz under pressure, six of Cleantech Group’s Market Intelligence team sat down to talk through what it all means for the sectors they cover, from semiconductors to EVs, water infrastructure, AI data centers, and dual-use tech.

What came out of that conversation was a candid look at just how deeply resource dependency runs, and why the case for cleantech has never been more urgent… or more complicated.

Anthony’s Take

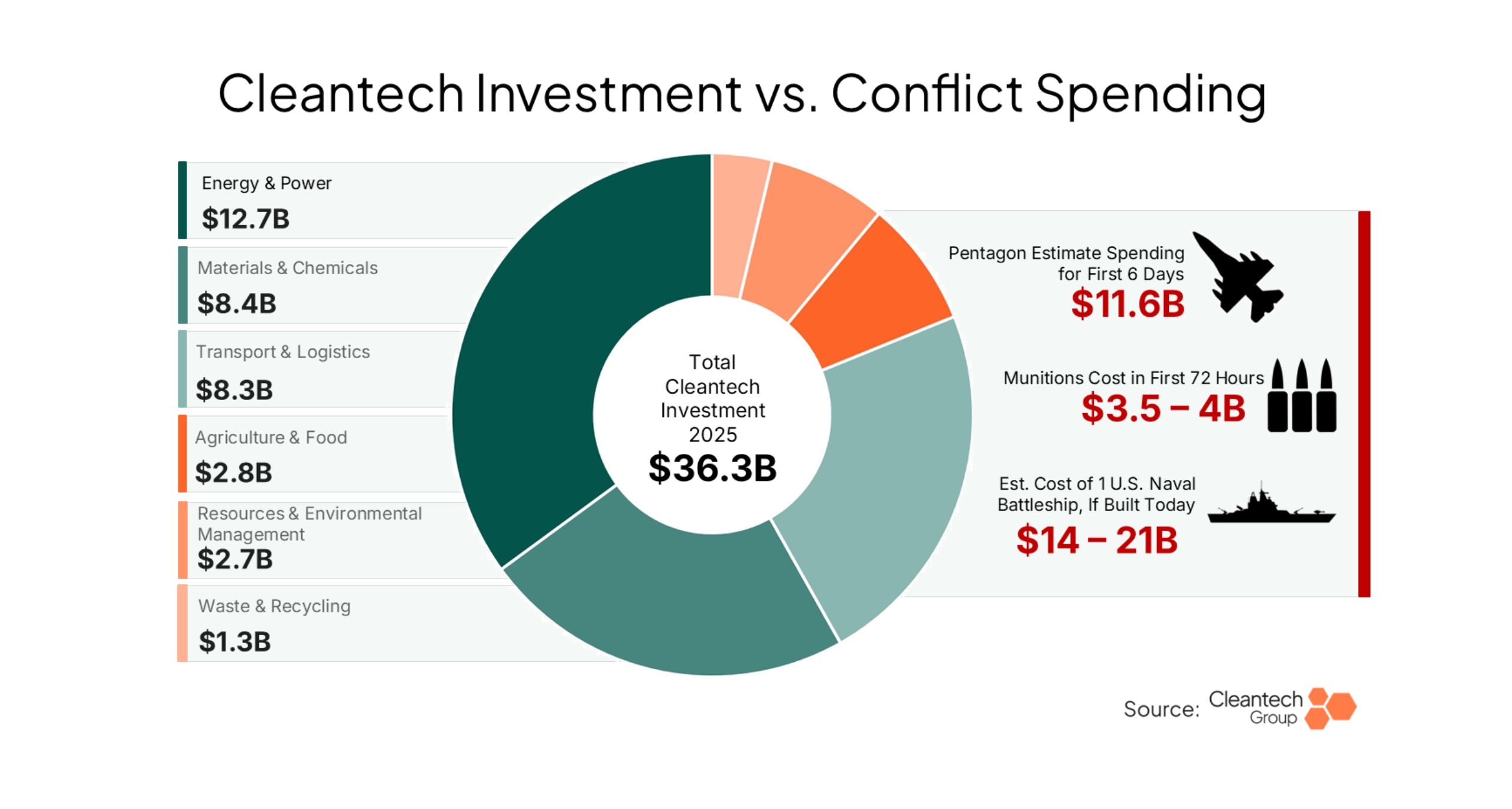

The outbreak of war in the Middle East marks a new level of global instability in an already chaotic 2020s. With certainty, the global drive toward sovereignty at national, regional, and even corporate levels will only intensify. As we put forward in our 2026 Cleantech Outlook, the cleantech and defense nexus will become increasingly apparent. The financial news is ablaze with real-time oil price updates, and stockpiling efforts like China’s are likely to be mirrored around the world, less as short-term hedges and more as long-term strategy.

Chemicals & Semiconductors:

The Invisible Supply Chain

Most people think of fuel when they think of oil and gas disruption. But Buff Lopez opened the conversation with something less obvious, and far more alarming for the tech sector.

Buff’s Take

Our clients in Japan’s chemicals space are seriously worried about the semiconductor industry. Qatar Energy has indicated they’re unable to produce liquefied natural gas, and helium, a byproduct of LNG production, is a critical component in semiconductor manufacturing. There are absolutely no viable alternatives. Bromine is another one—Israel and Jordan are major producers. On the upstream side, this is already shaking up business in a really significant way.

Diana’s Take

Its not just semiconductors, every single supply chain that potentially operates through the Middle East is getting hit. We’ve seen numerous O&G and chemical companies now pulling force majeure on their contracts due to instability. One of the big materials I’ve seen recently pop up is sulfur. People forget and/or overlook that sulfuric acid is the single most produced chemical in the world. It goes into fertilizers, mining, and manufacturing. That sulfur comes from refining in the Middle East. Now that’s gone. We’re looking at a materials shortage that affects everything.

This material shortage is also drawing attention to extraction techniques that reduce reliance on mineral acids or eliminate them entirely.

Innovators exploring alternative extraction approaches

Fertilizers, Fuels & Food Security:

The Case for Distributed Production

Nicole’s Take

Roughly a third of globally produced fertilizer passes through the Strait of Hormuz, and it has been effectively closed since the end of February. The cost of fertilizer has skyrocketed in the past two weeks, just as the planting season begins for farmers across the Northern Hemisphere. Farmers, already under climate and economic pressure, are the first to suffer, but the general public will soon see this reflected in even higher produce and food prices.

The disruption is reinforcing the case for more localized production of fertilizers, ammonia, and synthetic fuels — reducing dependence on centralized export hubs and vulnerable shipping routes.

Innovators working on distributed ammonia, fertilizer, and fuel production

- AIRCO

Energy & Power:

The Price Shock Argument for Renewables

Rising energy prices usually slow cleantech adoption down. But Zainab Gilani thinks this moment might actually be different, framing the geopolitical chaos as a potential turning point for the energy transition.

Zainab’s Take

In the hard-to-abate sector, you’re always asking: Can these electrification technologies compete with gas? If gas prices are skyrocketing, industries start asking whether they’d rather not be dependent on that volatility. I’ve seen reports of gas at $7 or $8 per gallon in parts of California. And there’s a political dimension: if gas prices are high heading into the midterms, what does that mean for this administration and the future of renewables?

Diana’s Take

There’s a striking UK Climate Change Committee model showing a repeat fossil fuel crisis in 2040 that would raise household energy bills 59% under business-as-usual versus just 4% on a net-zero pathway.

AI & Data Centers: Cleantech’s Unlikely Ally

AI is consuming energy at a scale we’ve never dealt with before. Buff sees a critical tension building, and depending on how it plays out, it could either drive the cleantech transition or blow it up.

Buff’s Take

Right now, AI’s biggest enemy is climbing energy prices. This could bring AI growth and data center expansion to a screeching halt. It’s already demanding unprecedented levels of energy, and if crude and energy prices keep climbing, nobody’s going to want to invest in that space.

Zainab’s Take

If it’s cheaper to get renewables on the grid, hopefully AI companies and data centers see this as a challenge they don’t want to face at scale later. This should encourage them to get more focused on renewables—more secure, stable baseload power rather than something subject to geopolitical volatility. We’re already seeing early signals of that thinking: Google recently partnered with Form Energy on a wind-plus-storage project in Minnesota.

Nicole’s Take

Aside from climate and economic questions, I think the attacks on Iran are highlighting moral and ethical issues with AI that have been easier to sweep under the rug until now. We´re seeing this with the ChatGPT boycott—people are calling for responsible use of AI and pulling their money from companies that are allowing their technology to be used for unconstitutional domestic surveillance, genocide, and murder of civilians.

Diana’s Take

If there was ever a time to really invest in and prop up renewables, now would be that time. The resilience argument isn’t abstract anymore; it’s a flashing signal saying: if you’re going after the AI data center play, build renewables to control your energy costs. You can’t afford to be tied to this supply chain and still run a business.

EVs: Not an Overnight Switch

Rising gas prices are the oldest argument in the EV playbook. But does this conflict actually move the needle? The panel pushed back on simple cause-and-effect.

Buff’s Take

We don’t have the infrastructure to support a sudden switch to EVs. They’re more expensive to purchase. The economy is down, and Americans don’t have the buying power. This volatility won’t immediately spike EV purchases. Look around a remote part of Texas—there’s not an EV charging station for miles. What this will do is strengthen the lobbying and investment case for those technologies.

Diana’s Take

I rented an EV in Houston once and even there, where there’s decent charging infrastructure, every station was taken. That experience would deter most potential buyers. The U.S. is deeply car-centric, commutes are long, and the last thing you want is to wait three hours to charge when you could spend two minutes at a gas pump. Convenience is still a massive factor.

Nicole’s Take

Besides charging infrastructure deployment, the final cost of charging is a major factor in EV adoption, particularly for users who would not be able to charge at home. While high gas prices are certainly a factor pushing users to EVs, where the cost of power remains high, volatile gas prices alone are not enough for drivers to make the shift to EVs. In the medium to long term, a push for energy independence could certainly drive national policies to develop and deploy energy and charging infrastructure that will drive EV use. But short term in the context of a cost of living crisis and economic stress, I doubt we will see a short-term shift towards EVs as the general public avoids unnecessary spending.

Water: The Infrastructure Nobody’s Talking About

Beyond energy and materials, a harder-to-headline crisis is quietly unfolding.

Diana’s Take

Water infrastructure in the Middle East is being actively targeted right now. Desalination plants are under threat. These people will not have water or will have very scarce water. That’s an everyday thing most of us take for granted. We turn on a faucet, and there it is. That’s clearly not going to be the case for a lot of people soon.

Buff’s Take

I was on a call yesterday and clients kept asking about water—remediation, treatment, purification—multiple times. It’s top of mind not just in the Middle East but in many parts of the world, and it’s a conversation that deserves its own dedicated expert attention.

Sunena’s Take

Hydropolitics is an increasingly important but often overlooked theme. In the Gulf, around 90% of drinking water comes from desalination, with supply concentrated in a relatively small number of large plants. This makes water infrastructure strategically vulnerable during regional conflicts, as we are seeing in this current war. Innovators such as Pani and Gradiant are working with desalination and industrial water operators in the Middle East to optimize plant performance and expand treatment capacity, while companies like Desolenator are piloting lower-carbon desalination systems in the UAE.

At the same time, water scarcity has also made the Middle East one of the most crucial hubs for water innovation. Regional companies such as ACWA Power (Saudi Arabia) are developing and operating some of the world’s largest desalination projects, while UAE-based innovators like Manhat are exploring lower-energy approaches to water production and treatment.

Ultimately, reliance on centralized desalination is pushing governments and utilities to explore more resilient approaches such as distributed systems, atmospheric water generation, wastewater reuse, and improved demand management.

Innovators working on desalination and water resilience

Conflict as a Catalyst: Defense & Dual-Use Tech

Anthony’s Take

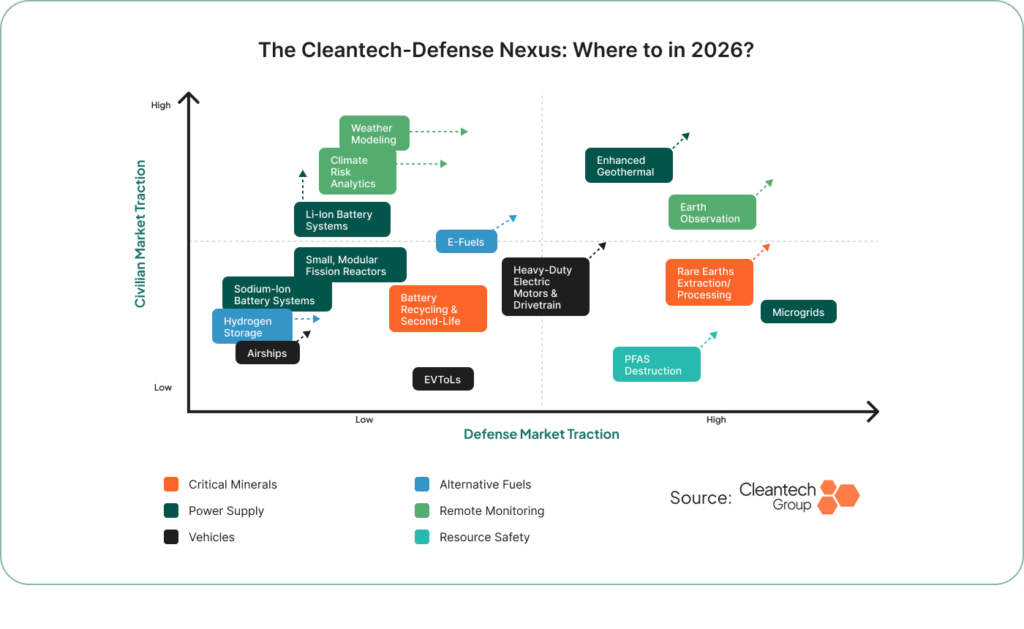

Large-scale military conflicts like this are likely to accelerate already observable interest in dual-use cleantech areas such as earth observation and weather modeling. See the urgency being displayed by European militaries engaging companies like ICEYE, and the early indicators of weather forecasting pull from the U.S. military. For example, the U.S. Air Force and Atmo.

We expect microgrids and modular power solutions, many of which are already experiencing data center demand pull, to be increasingly relied upon in times of heightened conflict.

Sunena’s Take

Modern conflicts are increasingly monitored through commercial satellite imagery and geospatial analytics, driving strong demand for earth observation (EO) capabilities. The global commercial satellite imaging market is projected to grow from about $5.87B in 2025 to over $15B by 2035, reflecting rising demand for near-real-time geospatial intelligence across defense, disaster response, and environmental monitoring.

During geopolitical crises, governments and media increasingly rely on high-cadence imagery and specifically Synthetic Aperture Radar (SAR), which can capture data through clouds, smoke, and darkness, making it particularly valuable in conflict zones. Innovators such as ICEYE, Array Labs, Capella Space, and Synspective are actively building SAR constellations and analytics platforms that serve both defense and environmental monitoring markets, highlighting the growing role of dual-use EO infrastructure. While unfortunate, increased defense demand actually stabilizes funding for EO infrastructure.

At a time when cleantech investment has faced uncertainty due to shifting climate policies and funding cycles, defense spending remains robust and is helping finance the costly satellite infrastructure that ultimately supports critical climate and disaster monitoring applications.

Innovators building earth observation infrastructure

- Capella Space

The Bigger Picture: Capitalism Meets Cleantech

The conversation wrapped on a cautiously optimistic note, not blind idealism, but the kind of hard-won recognition that cleantech has finally become a smart business move.

Buff’s Take

The case for cleantech is becoming stronger and pushing itself into the mainstream, not because of idealism, but because sustainability has converged with capitalism. It’s becoming the smart business move. At least we’re not in 1980. There are viable alternatives we can actually talk about and deploy. If this were 20 or 30 years ago, we’d be out of luck.

Diana’s Take

It’s good business that also happens to be sustainable and clean. It’s no longer a compromise. The sheer dollars being spent on this crisis—that money could have gone to investing and hardening our infrastructure, the alternatives that could have prevented this bottleneck. We’ll have to make it back somehow. That’s the part that’s disappointing and sad to sit with.

Zainab’s Take

Anytime you can make something a good business case, it’s easier to get off the ground. The more long-term infrastructure investment that happens now, the better you set yourself up for the future. Hopefully, AI and data centers get focused on renewables earlier rather than waiting until the problem is too expensive to solve.

Anthony’s Take

Long-term, technologies that support decentralization of critical systems will become more integral to strategic planning. We expect e-fuels to further enter conversations around fuel security and decentralization—INERATEC’s partnership with Rheinmetall and AIRCO’s manufacturing of mobile fuel units for the Pentagon are an early indicator. Beyond supply resilience, infrastructure recovery will become part of mainstream resilience conversations—technologies like Infravision’s autonomous construction of power transmission will soon be perceived as a practical “tomorrow” solution versus a “someday” solution. A new chapter in the chaos of the 2020s has begun, and with it will come new urgency to embrace creative solutions.

Qualified, explorable data on investments, partnerships, and projects gives you unmatched visibility to delve deeper into market trends and competitor activity.